The international financial network SWIFT is undergoing what may be the biggest transformation in its history: together with Consensys, the organization is developing a blockchain-based ledger that will soon be directly embedded into its infrastructure.

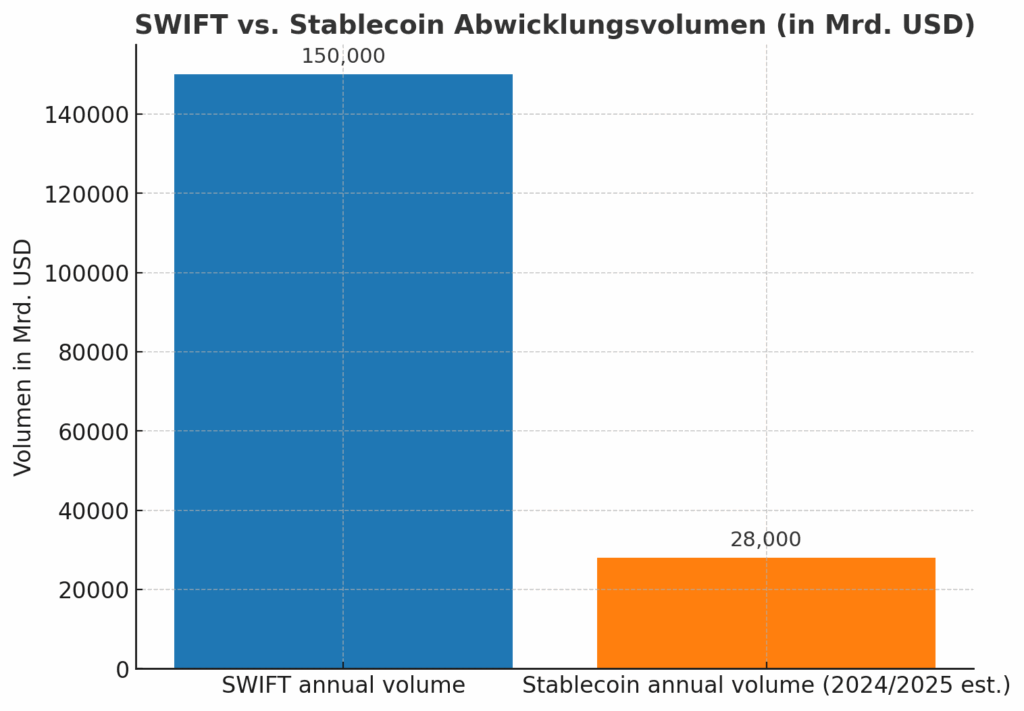

As the Financial Times reports, the new ledger will be able to process thousands of transactions per second 24/7, use smart contracts, and ensure interoperability with existing financial systems. This not only upgrades the 150 trillion USD network technologically – it also strategically shifts toward interoperability between banks, tokenized deposits, and digital assets. The initiative reflects the growing pressure from stablecoins and digital assets to modernize the traditional payments network.

From messaging layer to blockchain connector

For decades, SWIFT has primarily been a neutral communications system between more than 11,000 financial institutions in over 200 countries. Trillions were exchanged through secured messages without SWIFT itself acting as a payments processor.

With the new blockchain ledger, this role fundamentally changes: SWIFT aims to act as an interoperability layer connecting banks, stablecoins, tokenized deposits, and even CBDCs – thereby standardizing the fragmented digital asset landscape.

Implications for stablecoins

Until now, stablecoins such as USDC have taken on the role of dollar settlement in the crypto ecosystem. Billions are moved daily via exchanges and wallets. However, with a SWIFT-native solution, banks could issue their own tokenized deposits and settle payments directly through the SWIFT ledger.

The consequence: fee streams currently flowing to stablecoin issuers and crypto exchanges would be redirected more strongly into banking channels. For stablecoins, this could increase the pressure to integrate more closely with regulated payments.

Impact on Bitcoin and Ethereum & co.

While Bitcoin and Ethereum are not designed for settlement finality like bank money, they are deeply embedded in financial markets – whether through ETFs, derivatives, or as collateral in collateral management.

If banks build new on-chain functionalities through SWIFT, this could increase the willingness to accept BTC and ETH in collateral frameworks. Indirectly, this would channel additional institutional capital into crypto liquidity.

Efficiency gains and risks

SWIFT moves over 150 trillion USD annually. The average cost of cross-border payments is more than 6 percent, and settlement often takes days. Even a reduction of 50 basis points would save tens of billions.

On the other hand, risks remain: a permissioned ledger could lead to isolated “walled gardens” instead of fostering open liquidity. In addition, conflicts over standardization (ISO 20022 vs. smart contracts) as well as regulatory hurdles are still unresolved.

A turning point for the industry

The introduction of blockchain into SWIFT’s core infrastructure signals more than just a technical update – it is a strategic turning point. While the crypto industry long assumed that public blockchains would dominate cross-border payments, banks are now countering with their own model.

Whether this weakens the role of stablecoins or significantly boosts the overall volume of tokenized settlement will be decided in the coming years. What is clear: with SWIFT, the world’s largest payments network is now entering the blockchain era.

The new “shared ledger” is expected to handle thousands of transactions per second around the clock and map rules directly via smart contracts. More than 30 global institutions – including Bank of America, Citigroup, and Deutsche Bank – are supporting the development. This is not only about efficiency, but also about geopolitical positioning: with blockchain-based infrastructure, SWIFT seeks to strengthen its role against competing systems such as China’s CIPS or new stablecoin payment networks and to bridge the gap between traditional finance and the digital asset economy.