")

In the area of decentralized finance (DeFi), credit markets have played an important role. Some protocols now have billions of dollars in locked collateral and institutions are slowly stepping in. An introduction to the three biggest credit protocols: MakerDAO, Compound and Aave.

Decentralized credit protocol Aave recently revealed that it is in the advanced stages of developing a liquidity pool for institutions. It is a permissioned pool (i.e. it is access controlled) allowing Aave’s institutional partners to experiment with KYC / AML compliant DeFi lending.

In addition to bringing institutional money to the Aave Protocol, it also offers an opportunity to showcase how compliance analytics on public blockchains, travel rule protocols, and traditional KYC processes have combined to make cryptocurrency transactions more transparent and traceable than the fiat equivalent.

Credit markets as a strong DeFi pillar

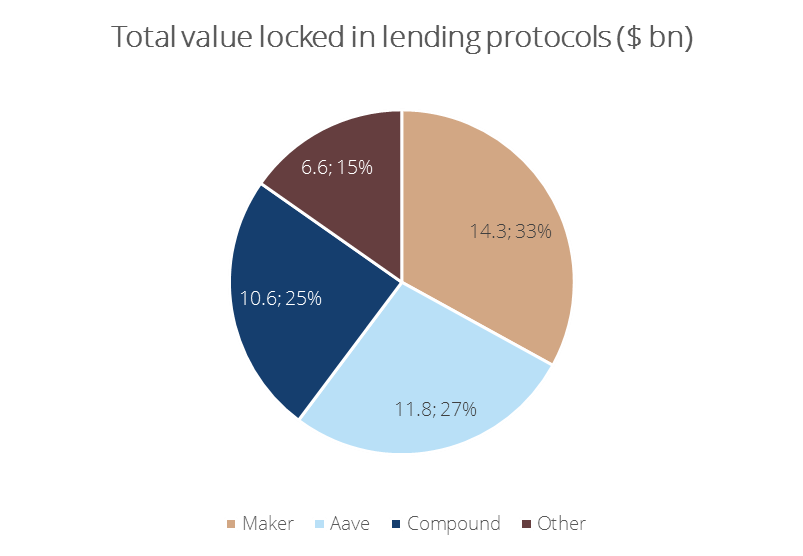

The seemingly accidental release of Aave’s news set twitter alight with the CeFi vs. DeFi lending debate. Last week, we considered crypto borrowing and lending on centralized platforms (CeFi), a market that Arcane Research conservatively estimated to be 400'000 BTC in size (around $30bn). On the other end of the spectrum, total value locked in decentralized finance (“DeFi”) lending protocols amounted to $43bn, outweighing CeFi at the time of writing. Lending accounts for over 50% of the value locked (TVL) in DeFi, illustrating that it is a key use case for the DeFi movement.

Borrowers use crypto as collateral to access liquidity without disposing of their coins, and lenders earn yield in environments where fiat rates are low and negative. Although DeFi borrowing is often used to facilitate leveraged investments in crypto or to take advantage of arbitrage opportunities, it also has the potential to support the acquisition of assets in the real economy.

The Ethereum blockchain forms the basis of popular DeFi borrowing and lending protocols such as Compound, Aave, and MakerDAO. Eighty five percent, or $37bn of $43bn, total value locked on lending protocols was staked on these three protocols.

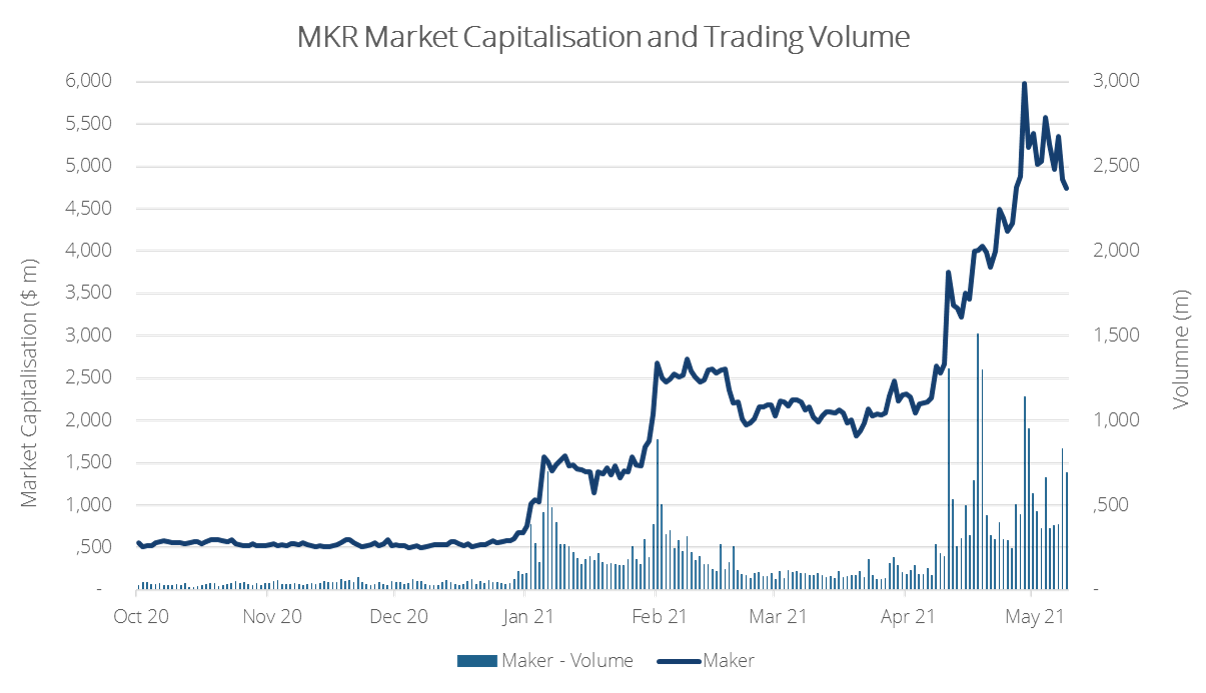

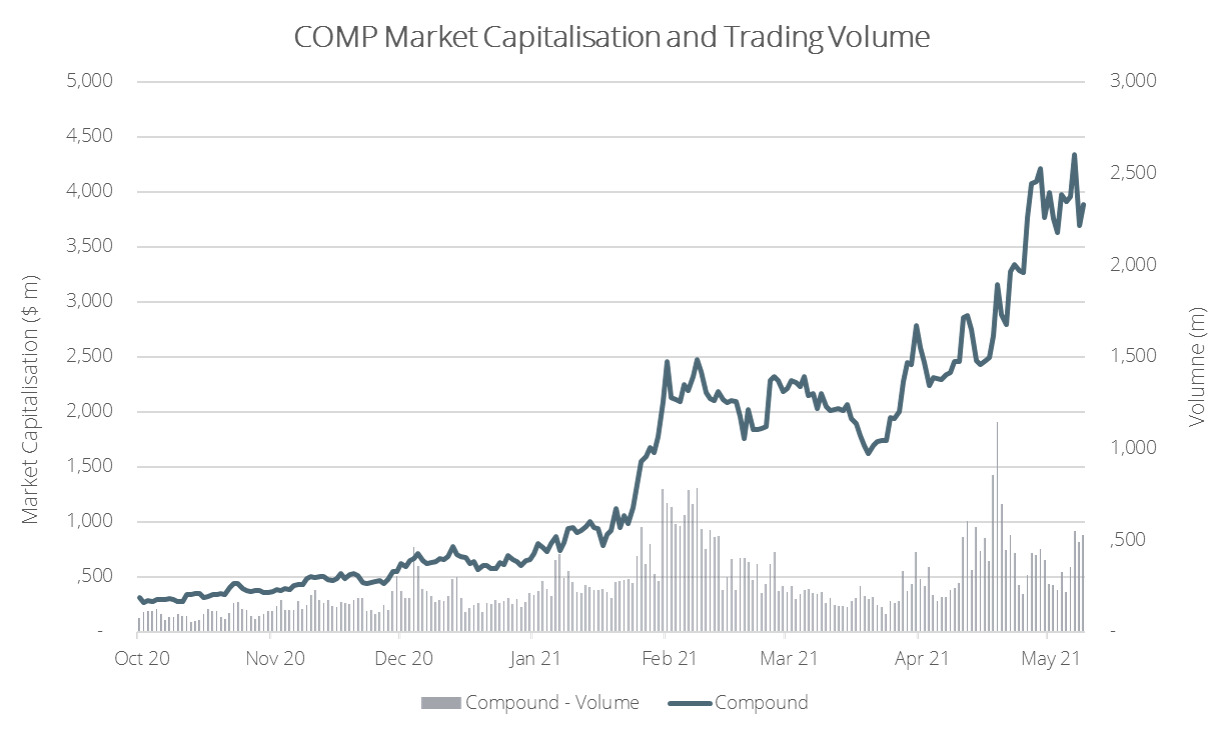

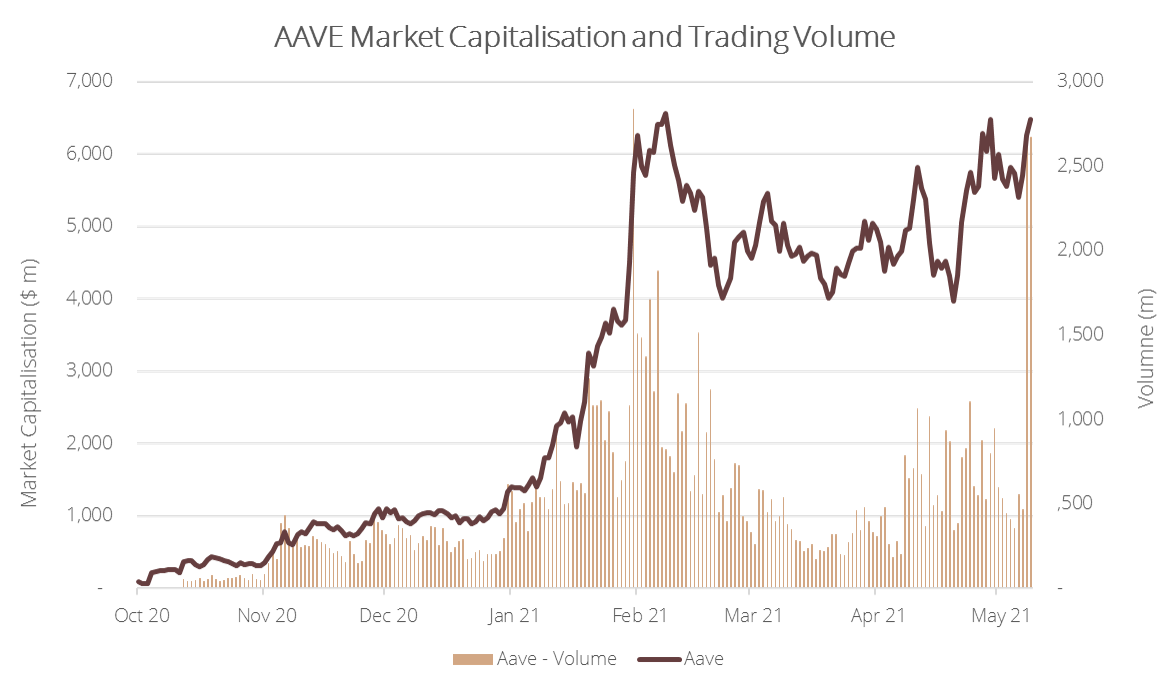

Since Aave began trading in October 2020, its coin market capitalisation has grown from $89m to almost $6.5bn, quickly catching and exceeding COMP and MKR in value and volumes traded, with near record volumes this last week (see graphs below).

The market appears to be pricing in continued utilisation of Aave, with Market Capitalization / Total Value Locked of 55% compared to 33% for MKR and 37% for Compound. But what are the differences between these protocols?

MakerDAO (MKR)

MakerDAO is a decentralized autonomous organisation (DAO) that was a pioneer in DeFi borrowing (there is no lending / investing piece). It started as a single collateral system – meaning that users borrow stablecoins (DAI) against only ETH as collateral.

The amount of DAI that you can borrow depends on the amount of ETH you deposit (or send into Maker’s smart contract). If you lock up ETH as collateral, DAI is minted for your loan. If the value of ETH drops, ETH is sold to repay borrowed DAI (and penalties). Loans must be paid in DAI and stability fees (similar to interest) are included in the balance owing. On repayment the DAI is burned, stability fees are used to buy MKR, and ETH is returned to the borrower.

MKR is the governance token that is also used to help ensure that the stablecoin DAI remains pegged 1:1 with the USD. DAI differs from USDC and USDT because it is collateralized by ETH and its peg to the USD is maintained through smart contracts. MKR acts as the lender of last resort, because if the value of ETH drops very fast, MKR tokens are created and sold to generate funds to collateralize loans.

Pool-based lending protocols

In contrast to MKR, Compound and Aave are pool-based borrowing and lending protocols that accept various coins as collateral. Smart contracts allow cryptocurrency deposits to be combined in a deposit pool. Borrowers access the pool of funds through the same contract, posting collateral. Required collateral is typically defined as a multiple of the loan amount (e.g. LTV of 150%). Liquidation automatically occurs, and liquidation fees are charged, if the LTV drops below predetermined limits. Cost of funds (interest earned on deposits) and interest paid on loans are algorithmically determined based on supply and demand, as are liquidity reserves.

Compound (COMP)

With Compound, when you lock in coins as collateral, you receive cTokens in return (ERC20 tokens that represent your balance in the relevant coin, e.g. cBTC or cETH). COMP is the governance token of Compound, which allows holders to vote on changes to the protocol.

Borrowers and lenders in the Compound ecosystem each receive a set amount of COMP every day.

Aave (AAVE)

Similarly, Aave allows users to access liquidity pools in different coins: using aToken, e.g. aBTC and aETH (pegged 1:1 to each coin) to represent the amount borrowed or lent. Aave is the governance token. Aave distinguishes itself by offering a feature to allow investors to take advantage of arbitrage opportunities. These flash loans allow users to borrow an unlimited amount of liquidity from the protocol for the duration of one Ethereum block. There is no credit risk because the loan repayment including interest is automatically settled within the duration of one block, or the transaction is reversed.

Look out for our article next week, where we will take a step back and evaluate the narratives behind leading digital asset tokens.

Copyright © 2021 | Crypto Broker AG | All rights reserved.

All intellectual property, proprietary and other rights and interests in this publication and the subject matter hereof are owned by Crypto Broker AG including, without limitation, all registered design, copyright, trademark and service mark rights.

Disclaimer

This publication provided by Crypto Broker AG, a corporate entity registered under Swiss law, is published for information purposes only. This publication shall not constitute any investment advice respectively does not constitute an offer, solicitation or recommendation to acquire or dispose of any investment or to engage in any other transaction. This publication is not intended for solicitation purposes but only for use as general information. All descriptions, examples and calculations contained in this publication are for illustrative purposes only. While reasonable care has been taken in the preparation of this publication to provide details that are accurate and not misleading at the time of publication, Crypto Broker AG (a) does not make any representations or warranties regarding the information contained herein, whether express or implied, including without limitation any implied warranty of merchantability or fitness for a particular purpose or any warranty with respect to the accuracy, correctness, quality, completeness or timeliness of such information, and (b) shall not be responsible or liable for any third party’s use of any information contained herein under any circumstances, including, without limitation, in connection with actual trading or otherwise or for any errors or omissions contained in this publication.

Risk disclosure

Investments in virtual currencies are high-risk investments with the risk of total loss of the investment and you should not invest in virtual currencies unless you understand and can bear the risks involved with such investments. No information provided in this publication shall constitute investment advice. Crypto Broker AG excludes its liability for any losses arising from the use of, or reliance on, information provided in this publication.