Ripple, a US-based blockchain-based digital payment company, is finally moving forward after a four-year legal battle with the Securities and Exchange Commission (SEC). The main dispute was: Is Ripple’s XRP token an unregistered security?

In 2023, the court ruled that selling XRP to institutions qualified as a securities sale, while sales to regular investors on exchanges did not. The SEC appealed the latter part of the ruling, alleging that XRP is an unregistered security. Now, two years later, Ripple’s founder says the SEC is dropping the case. The decision comes near the inflection point of Ripple, as it stands as the biggest beneficiary of Trump’s crypto-friendly approach, clearing the path for its ambitious plans in 2025.

What is XRP aiming to achieve in 2025?

The goal is to make the XRP ledger (XRPL) the go-to platform for banks and big businesses by adding better security, lending options, Ethereum compatibility, and new types of digital assets.

Key upgrades include identity verification, a compliant trading platform, lending tools, Ethereum-based app support, and improved ways to handle digital assets and liquidity. These changes aim to attract regulated financial institutions, making XRPL a more trusted and useful system for global transactions.

Here are some key agenda:

- Compliance: Institutions can launch permissioned domains to create compliant DeFi products, such as tokenized bond markets, making them only accessible to verified participants and eliminating legal concerns.

- Institutional Lending: Direct on-chain lending with undercollateralized loan options (expected by Q3 2025), integrating Ripple’s RLUSD stablecoin and real-world assets (RWAs) and supporting a more mature and stable DeFi ecosystem.

- Programmability: EVM Sidechain (Q2 2025) and custom contract extensions, attaching custom code to XRPL primitives (e.g., escrows, automated market makers - AMMs) without full smart contracts.

- Tokenization: Multi-Purpose Tokens (MPTs) for RWAs and financial products. These are semi-fungible tokens supporting bonds, RWAs, and structured products with metadata (e.g., expiry dates).

- Liquidity & Trading: Integrated liquidity pools and a clawback feature for asset recovery. Optional feature allowing issuers to reclaim misused assets (e.g., stolen funds).

Banks and Ripple

Ripple is positioning XRPL as a regulatory-friendly blockchain, making it a gateway for banks, fintech firms, and institutional investors. With a focus on compliance, EVM integration, and asset tokenization, XRPL aims to drive institutional adoption and expand XRP’s long-term demand.

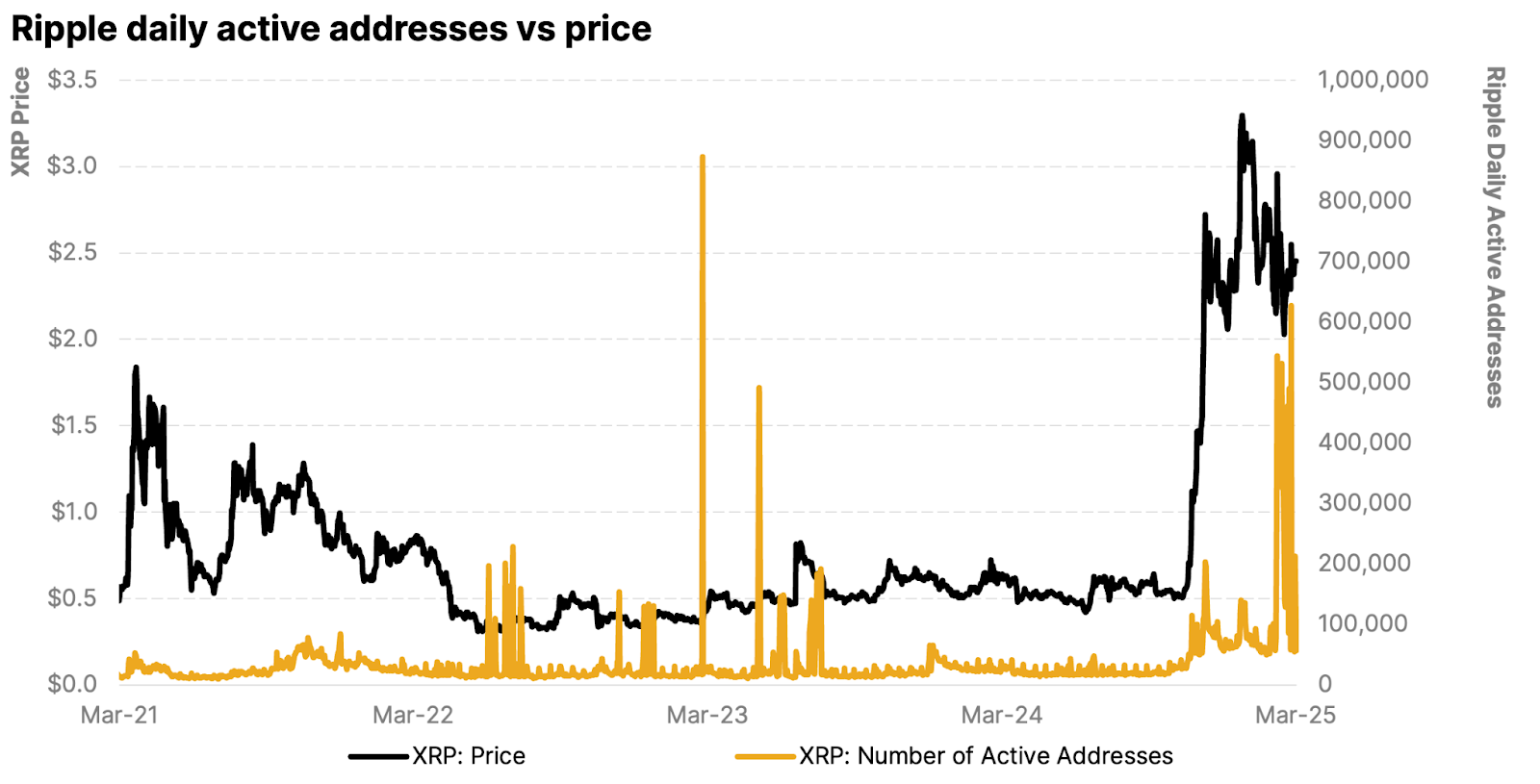

The chart above demonstrates that active addresses on the network have grown by almost 300-400% (disregarding the spikes). The elevated levels since September show there's growing user activity on the network, which could be driven by forward-looking speculation.

The surge in activity may be driven by the December 2024 account reserve reduction from 10 to 1 XRP, which lowered onboarding costs. Additionally, Ripple’s partnerships with Archax, Meld Gold, and Zoniqx to enable tokenized assets like gold and Treasury bills on XRPL could be fueling increased settlement activity.