A general overview of the Aave DeFi protocol, as well as an interview with founder and CEO Stani Kulechov.

Aave v1

In 2018, the ETHLend project was rebranded “Aave”. In the peer-to-peer lending model that ETHLend introduced, users were required to interact via smart contracts, but finding user matches for lending and borrowing proved not to be very efficient. As a consequence, the model was substituted for a decentralised non-custodial liquidity market protocol with Aave. The new model introduced liquidity pools, where users could interact with pooled funds instead of with single users. In October 2019, the Aave v1 public testnet, with the liquidity pool model, was initiated (keeping the native token LEND): its official launch was in January 2020. The protocol grew to a market size of USD 1B in less than six months and brought additional innovations, e.g. “Flash Loans” and “aTokens” as a way to unlock capital previously locked in DeFi.

Aavenomics: the AAVE token

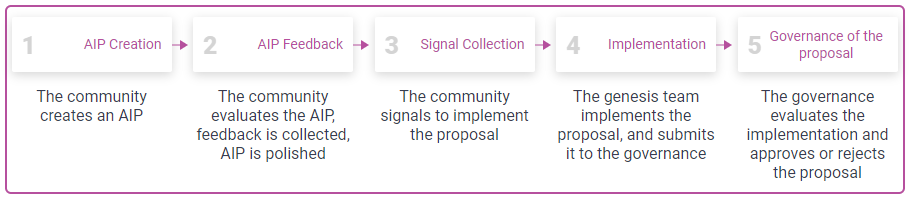

The AAVE token was introduced on the Ethereum blockchain in October 2021, with the aim of handing over the protocol governance to its community and making Aave a more decentralised protocol. AAVE allows its holders to vote and decide on protocol upgrades via Aave Improvement Proposals (AIPs). AIPs can, for example, involve adding new collateral assets to the protocol or changing the risk parameters of existing tokens.

To guarantee a smooth transition, existing users had the opportunity to swap their LEND tokens for AAVE at a 100:1 ratio (i.e. 100 LEND tokens can be swapped for 1 AAVE token). The staking of AAVE tokens was also introduced and allows users to earn staking rewards generated from protocol fees. AAVE owners can also potentially benefit from fee discounts on borrowing and lending.

Aave v2

Aave Version 2, or Aave v2 for short, was implemented in December 2020. Aave v2 is a protocol upgrade and introduced additional features, e.g. “Collateral Swaps” and “Batch Flash Loans”. Apart from new features, contracts were optimised, resulting in lower transaction fees compared to that of v1. The Aave v2 upgrade does not impact the AAVE token, and Aave v1 continues working as a parallel protocol.

Lending mechanism

Aave supports lending and borrowing for over 25 tokens, e.g., ETH, DAI, LINK, and UNI. Users can lend a specific token and earn interest by supplying their tokens to an Aave liquidity pool from which other users can then borrow. When the user supplies their tokens to the liquidity pool, they receive so-called “aTokens” in return, which represent the underlying token (1:1 ratio) plus the accrued interest.

- User wants to lend Uniswap (UNI) tokens

- User sends UNI to the Aave smart contract

- Smart contract issues aTokens “aUNI” to the user, which represent the UNI tokens supplied plus the interest earned while the supplied UNI is locked in a pool

In other words, while the underlying asset (in our case UNI) is loaned out to borrowers, the aTokens (in our case aUNI) accrue the interest.

Interest rate

In Aave, users can choose between variable and stable interest rates. The variable interest rate is determined algorithmically by the relation between a token’s liquidity pool (supply) and the demand to borrow it. If the borrowing demand for a specific token goes up, the liquidity goes down and the interest rate goes up. However, stable interest rates use an average calculation and can reduce volatility. Through a mechanism called “interest rate switching”, users can also switch between variable and stable interest rates at any time.

Over-collateralisation

As of now, all loans in DeFi require over-collateralization; this also applies to Aave. In other words, users who want to borrow need to supply more collateral than the amount they want to borrow (this applies to all the tokens supported by the Aave protocol). Collateralisation rates depend on the crypto asset and can vary between 15% – 75% (e.g. ETH has a rate of 75%, which means that with 1 ETH as collateral, users are able to borrow 0.75 ETH worth of the crypto asset to be borrowed). If the value of the deposited collateral falls below this threshold, the user is liquidated.

Flash Loans

Flash Loans are entirely unique to DeFi; they are non-existent in traditional finance. Flash Loans are what distinguishes Aave from its competition and make uncollateralised loans possible. They work by establishing time requirements: users must pay back the coins loaned within the same Ethereum transaction (within the same Ethereum block) otherwise the transaction will fail (i.e. every transaction that occurred with the borrowed funds will be cancelled).

The only costs occurring in Flash Loans are a fixed rate of 0.09% on the borrowed amount (which is paid to depositors and facilitators) as well as the network fees. Flash Loans allow borrowers to take advantage of short-term financial opportunities, e.g. arbitrage trading. They can also be used for other types of financial transactions, such as swapping loan collaterals, but since the mechanism is still relatively new, additional use cases are still being discovered.

What’s next?

Due to the Ethereum network’s high fees affecting Aave interactions, Aave has been looking into multichain strategies and is working on building a framework for cross-chain governance. The Aave protocol expanded into the Ethereum Layer 2 solution Polygon by March 2021, where fees are significantly lower. In October 2021, Aave successfully ported into the Avalanche blockchain, where it reached USD 5B in Total Value Locked (TVL) by the end of the month. Additionally, Aave founder Stani Kulechov has stated that Aave is looking specifically to expand into the Solana blockchain too.

Aave has also released a new proposal for an upgrade to Aave v3. The upgrade includes new features that improve efficiency, cross-chain capabilities, risk management and Layer 2 functionalities. The voting will occur during the beginning of November 2021, and is very likely to be approved.

In summary, Aave is currently the biggest lender, and one of the largest players in the DeFi space: it is a so-called DeFi blue chip. It is also very likely to continue holding this position with its historically proven fast-paced development, commitment to decentralisation, and growing community.