The CVJ.CH Summer Soirée at GenTwo's Zurich offices brought together leading voices in Swiss digital asset banking for a candid discussion on the state of crypto in traditional finance.

Despite the rainy weather that forced the planned barbecue indoors, spirits were high as a packed room of financial professionals - around 70 in total - gathered for an evening of insights and networking. The panel, moderated by Leon Curti, Editor of CVJ.CH, featured five experts at the forefront of Switzerland's digital asset revolution: Pascal Wyser from Incore Bank, Robin Lemann from Swissquote, Andri Gmünder from ZKB, Andy Flury from Wyden, and Mark Arasaratnam from GenTwo Digital. Below, we've summarized the key takeaways. A major thank you to all the panelists and attendees for an amazing evening!

Switzerland's unique position in digital assets

One striking revelation from the panel: Switzerland now boasts over 20 banks offering crypto asset services – a density unmatched anywhere in the world relative to population. As Pascal Wyser from Incore Bank noted, this positions Switzerland not just as a traditional safe haven, but increasingly as a digital asset safe haven as well. "Switzerland has always been a safe haven and Switzerland will always be a safe haven," Wyser emphasized, citing the country's educational system, strong Swiss franc, and robust economy as enduring advantages that extend naturally into the digital asset space.

The panelists agreed that Switzerland's early regulatory clarity through the 2021 DLT Act has been crucial. This legislation removed ambiguity around asset classification and custody solutions, giving Swiss institutions a clear framework to build upon. Combined with the country's financial heritage and innovation ecosystem – including institutions like EPFL – Switzerland has created a compelling environment for digital asset development.

Why banks matter in the crypto ecosystem

When asked why customers should choose banks over crypto exchanges or ETFs, the panel's response revealed multiple compelling reasons. Andy Flury put the counterparty risk issue bluntly: "With all been involved in FTX in one way or another... what banks have been good at and have done for decades is safekeep client assets." Unlike crypto exchanges where everything is commingled – the exchange, brokerage, lending, and funding operations – banks maintain strict separation with "Chinese walls" between departments. This structural difference provides the security that many investors, particularly institutional ones, require.

But security is just the beginning. Andri Gmünder from ZKB highlighted the simplicity factor: "Clients want simplicity, especially if you want to put two or 5% allocation of your portfolio into crypto assets. You do not want to switch to a separate app." The vision is clear – integrated wealth management where crypto sits alongside traditional assets in a single interface. Robin Lemann added another crucial dimension: institutional requirements. "Think about having funds issued. We also do safe custody for funds or for actively managed certificates where you rather want to have a bank in order to safekeep, maybe also in order to get the liquidity."

The young customer revolution

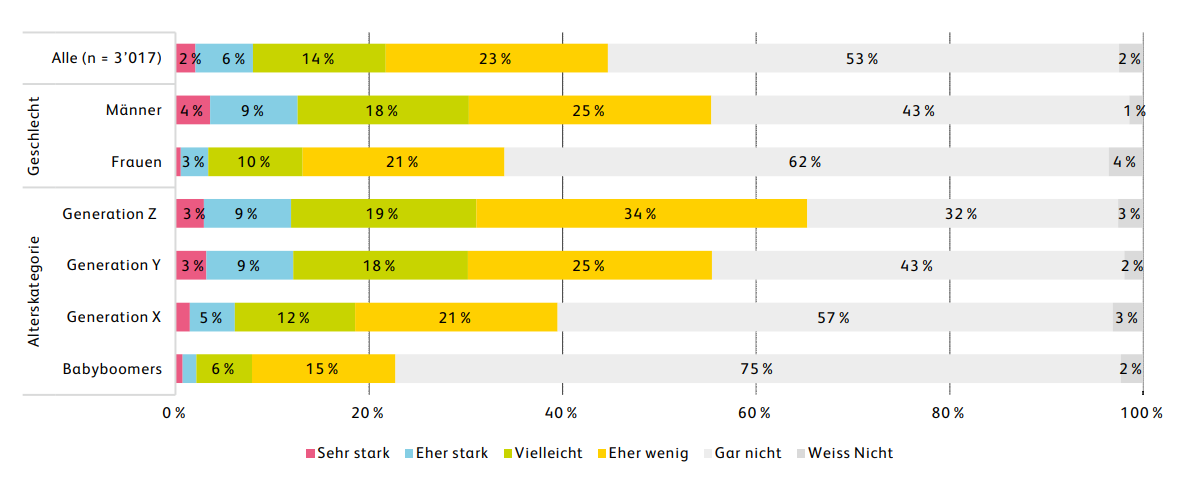

Perhaps the most intriguing insight came from ZKB's experience with customer demographics. Gmünder shared that 40% of their crypto clients have never invested before, and the average age is significantly below that of traditional investment products. This suggests crypto could solve two critical challenges for traditional banks: attracting younger customers and onboarding first-time investors into the broader investment ecosystem.

As Lemann noted, more than 25% of generation Y are interested in trading cryptos according to a Lucerne University study. "Sometimes they don't even own stocks or shares yet. So it's also a tool where you can actually onboard clients and then make them diversify into other asset classes as well."

Implementation realities and challenges

For banks considering digital asset offerings, the panel offered sobering but practical insights on timelines and challenges. While Andy Flury mentioned Wyden's fastest implementation was just two months, Gmünder suggested ZKB's offering took more like 18-24 months, including regulatory applications to FINMA. The challenges are multifaceted. Mark Arasaratnam outlined the "three Cs": compliance, complexity, and custody. "How do you shoehorn new and evolving regulation into an existing regulatory framework that's existed for the last 60, 70 years?"

The complexity extends to integration – traditional banks have cash, fixed income, FX, and commodities on different ledgers, while digital assets operate on a unified blockchain ledger. Flury emphasized that banks need vendor solutions for custody, KYC, and trading, often struggling with integration. "We need to better work together. We need to provide an end-to-end service to the bank so that it's as little effort as possible."

The path forward: from execution to advisory

A critical theme emerged around the current limitations of crypto offerings in Swiss banks. Pascal Wyser pointed out that "pretty much all the offerings within banks are execution only," requiring clients to convince their relationship managers to buy Bitcoin for them. This leaves "95% plus" of potential volume untapped, sitting with big asset managers and pension funds who are "very, very far away" from investing in digital assets.

The solution, according to the panelists, lies in moving toward advisory-based models. As Gmünder noted, this could be the key USP for banks: "Once banks start to offer advisory or also multi-asset portfolios with crypto allocations, that's something that we don't really see crypto exchanges doing right now."

Looking ahead: tokenization and consolidation

When asked about the next wave beyond basic crypto trading, the panelists converged on tokenization as one major trend. Lemann emphasized that while there were many tokenization projects years ago, "they were probably not as fundamental and too early. Today we see more fundamentally sensible projects." The panel envisions banks providing comprehensive services for tokenized assets – from custody of underlying assets to providing liquidity through exchanges and safekeeping via custodian solutions.

This represents a natural evolution from currency tokens to tokenized money market solutions, equity tokens, and beyond. Mark Arasaratnam predicted significant market consolidation ahead: "You'll see banks acquiring crypto firms, crypto firms acquiring banks." He cited Robinhood's recent acquisition of Bitstamp, which overnight gave Bitstamp 24 million new customers, as a harbinger of things to come. The driving force? "What do they want? They want more yield," Arasaratnam explained. As the market moves up the risk curve from stablecoins to money market funds to private credit (now $14 billion on-chain), yield products will increasingly blur the lines between traditional finance and DeFi.

The innovation imperative

One perspective came from the discussion of why banks shouldn't simply outsource to existing providers. As Flury argued, "This new technology blockchain is here to stay... at some point, every type of asset will be tokenized. Bankable assets, unbankable assets. So banks need to get familiar with this technology."

By building internal capabilities rather than purely outsourcing, banks ensure they develop the knowledge base necessary for a tokenized future. This isn't just about offering Bitcoin trading – it's about preparing for a fundamental shift in how all assets are created, traded, and managed.

Key takeaways

As the panel concluded with a rapid-fire round (revealing, among other things, unanimous support for Bitcoin over gold and a firm rejection of pineapple pizza), several key messages emerged:

- Switzerland's regulatory clarity and financial infrastructure create unique advantages in digital assets

- Banks offer security, simplicity, and advisory capabilities that pure crypto platforms cannot match

- Crypto is bringing younger, first-time investors into the banking ecosystem

- Implementation takes time, but the technology learning curve is essential for future competitiveness

- The shift from execution-only to advisory services will unlock institutional adoption

- Tokenization represents the next major wave, requiring banks to build capabilities now

The evening wrapped up and attendees moved to networking, and one thing was clear: Swiss banks are no longer asking whether to offer digital assets, but how to evolve their offerings to capture the full potential of this transformation. The question isn't if traditional finance and crypto will converge, but how quickly and completely this convergence will reshape the entire financial landscape.