A monthly review of what's happening in the crypto markets. Enriched with institutional research on the most important topics in the industry. Written in cooperation with the Swiss digital asset specialist, 21Shares AG.

Crypto regulations brew in May as elections inch closer. The first presidential debate are scheduled for June 27th. Regulating crypto is becoming an increasingly inevitable hot topic in the lead-up to the elections. The competition heats up again, reminiscent of the 2020 race. However, this time, it’s Joe Biden who is defending his presidency. Both candidates are even represented on Solana’s blockchain with meme tokens in their names. Republicans have been fiercely embracing crypto in Congress, achieving bipartisan agreement for the first time. Once a skeptic himself, Donald Trump has recently vouched for the industry. He left the Biden administration in limbo with regard to pending crypto regulations.

Easing crypto custody restrictions, encourage US financial institutions to hold crypto on behalf of their clients. The House passed a bill on May 8th, nullifying the Securities and Exchange Commission’s (SEC) 121st Staff Accounting Bulletin. SAB 121 requires banks holding customers' cryptoassets to present a liability on their balance sheet to reflect their obligation to safeguard them, potentially leading to substantial capital expenses. On May 16, the Senate approved the bill before it landed in the White House, which vocalized its intention to veto it as it would allegedly undermine the SEC’s work to protect investors. However, if SAB 121 is overturned, it would diversify crypto custodians, only four of which are currently servicing the 11 Bitcoin Spot ETFs, a major concern for Congress. Moreover, the bill would be advantageous for investors who are discouraged from holding crypto outside traditional frameworks.

Decentralization gains priority with regulators

For years, the distinction between the SEC's jurisdiction over crypto and that of the Commodities and Futures Trading Commission (CFTC) has been blurry. The Financial Innovation and Technology for the 21st Century Act (FIT21) would provide the CFTC with new jurisdiction over digital commodities and clarify the SEC’s jurisdiction over digital assets offered as part of an investment contract based on the degree of decentralization of a crypto network. The bill has also laid out five conditions for a “decentralized system”:

- No one person can control the network or prevent others from using it. This means that no one can solely decide how it works or who can use it.

- No entity should own more than 20% of its native cryptoasset.

- The decentralized system's code should be open-source and can’t be majorly modified by a single person. Unless it’s to fix vulnerabilities and improve security, consensus on code updates should be reached through a decentralized governance system.

- No one from the founding team or anyone affiliated with the network should promote its cryptoasset to the public as an investment.

- The cryptoassets minted over time, through the programmatic functioning of the blockchain, should be distributed to the end-user, not a select few.

This sets a new precedent. It’s the first time decentralization enters the legal conversation in that context as a priority. This is a gauge for how close an asset is to a commodity. Although still pending the green light from the Democrat-controlled Senate, FIT21 has already forged the path for networks to work actively toward achieving sufficient decentralization.

US regulators look to MiCA for guidance

21 Shares believe that regulatory clarity is bound to be reached, especially with these two bills brewing in Congress. Many drew parallels between FIT21 and Europe’s iconic crypto framework ratified earlier this year, Markets in Crypto Assets (MiCA). Both legislations suggest conducting a study to better understand and, in turn, better regulate the burgeoning realm of decentralized finance. That said, crypto is still an inevitable topic of discussion in Europe. The European Securities and Markets Authority (ESMA) invited investors, and trade associations, among others, for consultation to assess possible benefits and risks of its Undertakings for Collective Investment in Transferable Securities (UCITS). UCITS would gain exposure to cryptoassets and 18 other asset classes.

ESMA has until August 7 to gather input. UCITS funds are generally considered safe, well-regulated investments sustaining €12T in market valuation. Thus, the funds are vital for crypto as UCITS accounts for 75% of all collective retail investments in the EU. Thus, if the conclusions of this consultation are in favor of adopting crypto, it would attract an influx of investors and bring more regulated accessibility to this asset class. Moreover, although still under consultation, ESMA’s deliberation adds more credibility to crypto, considering its renowned strict regulatory standards.

Finally, June’s calendar is almost blocked for many anticipated events that would forecast the continued trend of shifting policy. Due to increasing political pressure, we may see inactive bills resurface in the Senate. For example, the bipartisan support for FIT21 could bring back pending bills such as Clarity for Payment Stablecoins and Keep Your Coins. However, this renewed legislative activity alone could not exclusively impact the financial landscape, as macroeconomic headwinds still deeply affect crypto. The next monetary policy meeting will be held on June 12. This will pave a clearer path for rate cuts, with inflation data coming out right before. Following the same sentiment, the U.S. Treasury's buyback program, which started on May 29, will buy back $2B in weekly bond repurchases. This reduces outstanding debt while increasing overall liquidity, potentially allowing capital to flow into riskier assets.

Bitcoin's institutional demand increases

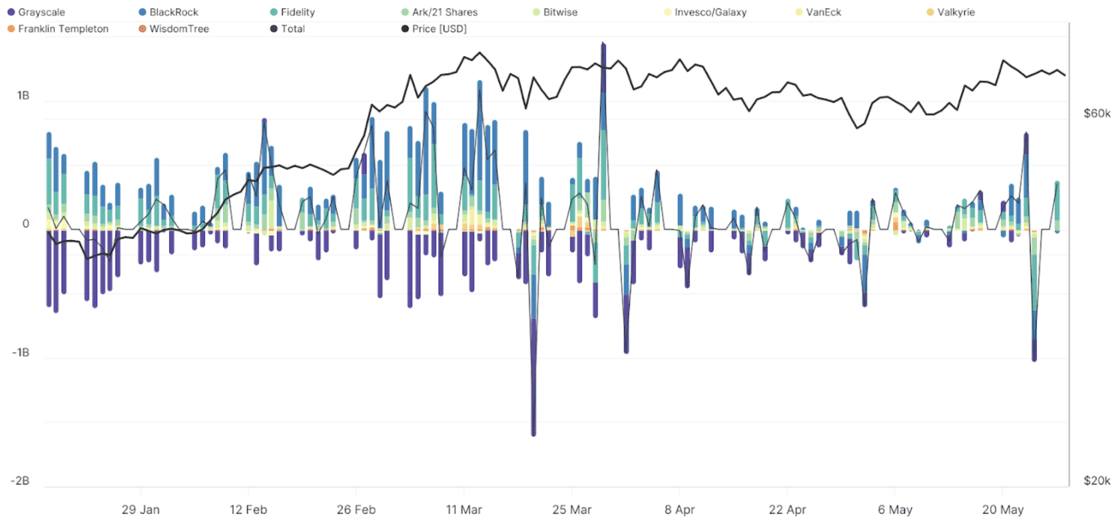

May was an exciting month for crypto. Institutional interest in Bitcoin kept growing and inflows increasing after a quiet April. The 13F filing deadline on May 15 revealed significant institutional exposure to Bitcoin. By the end of Q1, 937 professional investors owned $11B in U.S. Bitcoin Spot ETFs, about 20% of the ETFs' total assets. In contrast, Gold ETFs had only 95 professional investors in their first quarter post-launch, representing less than 10% of Bitcoin ETFs' reach.t

U.S. Bitcoin Spot ETF Flows (USD) / Source: Glassnode

The adoption of Bitcoin is unsurprising given the accessibility that Bitcoin ETFs offer traditional institutions through a regulated investment vehicle. The full breakdown of Bitcoin ETF adoption can be found here. Bitcoin’s role as a safe haven was reinforced in Japan, where economic pressures led Metaplanet to adopt Bitcoin as a strategic reserve asset, acquiring over $7M since April. International interest in Bitcoin continued, with the approval and launch of BTC and ETH exchange-traded notes (ETNs) in the U.K. for professional investors, showcasing the growing appetite for the asset class.

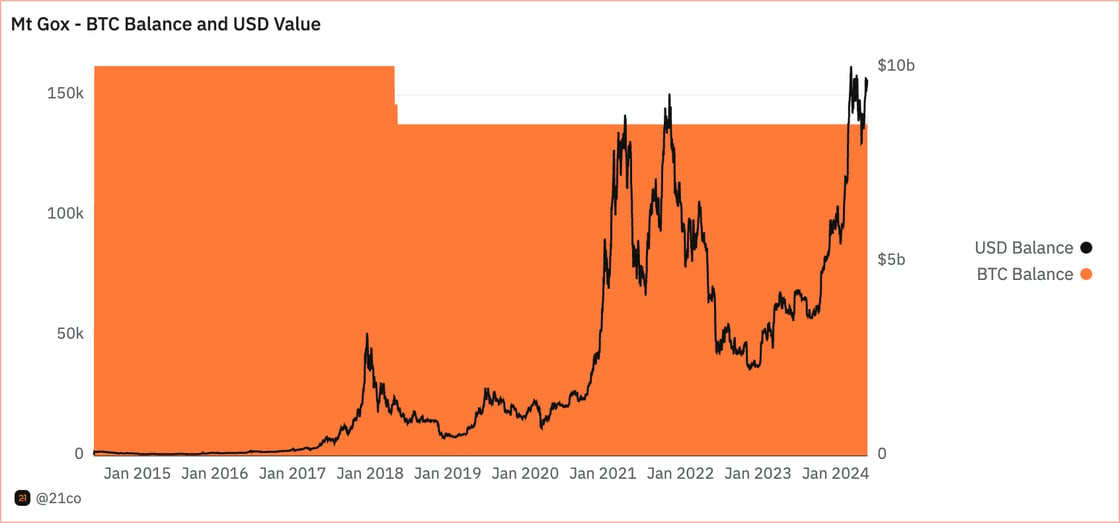

Climbing Mt. Gox

Despite the optimism surrounding Bitcoin's institutional adoption, the market is expected to face a headwind due to a decade-old exploit. Mt. Gox, once handling nearly 70% of all Bitcoin transactions, was hacked in 2011 and closed down after bankruptcy in 2014, losing 750K BTC, with 200K later recovered. Reparation initiatives were instituted to reimburse creditors with 142K BTC, 143K BCH, and 69B Japanese yen by October 31.

Mt. Gox BTC Balance in BTC and USD/ Source: 21co on Dune

Recent observations reveal that wallets associated with the exchange transferred approximately $9B of assets to a single address, likely part of the reimbursement plan. This rendered Bitcoin unable to break the resistance level at $70K due to the fears of potential sell-offs. However, since investors affected by Mt. Gox are early adopters who likely still believe in the asset class, selling pressure may be milder than expected. Once repayments are completed, another looming market uncertainty should be lifted, allowing Bitcoin to finally move on.

Ethereum’s Watershed Moment

The most significant takeaway from May was the SEC’s approval of Ethereum Spot ETFs’ 19b-4 filings on May 23rd. The filing marked a crucial milestone for the crypto industry. While the approval does not explicitly designate Ethereum as a commodity, it is implied by classifying these ETFs as “commodity-based trust shares.” These products are not tradable until the agency approves the S1 filings. Since this could take weeks or months, investors must be patient to see the impact of these ETFs. Nevertheless, this moment signals a growing acceptance of Ethereum within regulated investment frameworks. Potentially opening the market to significant inflows from Registered Investment Advisors and the local ETF market, with the latter valued at $8T.

ETH and BTC Performance Since December 2023 / Source: TradingView

Nevertheless, investors should exercise caution in the lead-up to the U.S. ETH ETF launch, given the “buy the rumor, sell the news” phenomenon observed after the BTC ETF launch, where Bitcoin’s price retraced 18% before rallying 90%. This phenomenon is already occurring, with Ethereum catching up to Bitcoin's performance when news of the approvals broke. However, the impact of ETH ETFs might differ due to the asset’s distinct attributes.

ETH ETFs missing out on critical staking rewards

U.S. ETH ETFs might follow the trend in Hong Kong. Their ETH ETFs only attracted about 20% of the assets under management, around $250M. Further, the absence of staking in the products removes a crucial component of Ethereum’s investment appeal. Investors purchasing these ETFs will miss out on staking rewards, which they could otherwise access by holding and staking ETH directly. On the positive side, the lack of staking features in the ETFs means the yield isn’t diluted for the wider community!

Additionally, ETH’s utility, as collateral in lending agreements or for minting NFTs, to name a few, is sacrificed when investing via ETFs. That said, many institutions accessing Ethereum through these ETFs have no option but to use regulated vehicles. Despite this, they are expected to generate excitement, opening a regulated investment avenue to the next-generation decentralized app store. This is especially significant with the network’s upcoming upgrade in Q1 of 2025. For additional details, refer to our breakdown, discussing some of the anticipated features.

Nonetheless, the SEC approval adds credibility to a broader range of cryptoassets. This indicates that Bitcoin is not the only 'legitimate' one in the eyes of regulators. With FIT21 developing, we could be heading to a future where a wider array of decentralized protocols could be integrated into the stock market. A step to fostering and embracing technological innovation and adoption. Further, Ethereum’s approval represents a significant step forward, highlighting the value of its on-chain ecosystem of decentralized applications. Indeed, May was a landmark month, further solidifying mainstream acceptance, with the approval underscoring broader integration of cryptoassets within traditional financial markets, which could set the stage for tokenization, one of the most disruptive financial innovations in recent years.

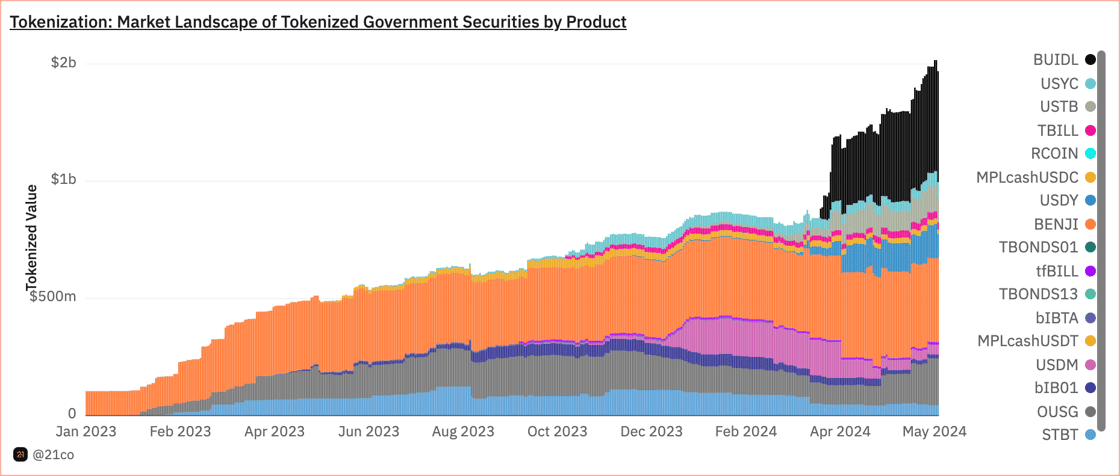

Chainlink continues powering tokenization

On May 17, the Depository Trust and Clearing Corporation (DTCC), the world’s largest securities settlement system, which processed $3 quadrillion in securities in 2023, announced it completed a pilot project in collaboration with Chainlink and major financial institutions such as BNY Mellon and JP Morgan. The project builds upon the existing DTCC Mutual Funds Profile Service I (MFPS I). It is the industry standard for transmitting NAV data, such as fund price and rate. The pilot does not affect initial portions of the workflow, such as calculating fund data. Focus was to create a standardized way to disseminate fund information across different blockchains. That said, the project will likely expedite real-world asset tokenization. It has become an increasingly important industry segment, showcased by tokenized government securities growing 20x in assets under management since the start of 2023, from nearly $100M to almost $2B.

Market Landscape of Tokenized Government Securities by Product / Source: 21co on Dune Analytics

The DTCC service handles the daily transmission of price and rate data for numerous mutual fund securities. Currently the NAV model connects funds and service providers to distributors. It collects and disseminates relevant data via message queues and file-based methods at regular intervals. On the other hand, Smart NAV extends the dissemination capabilities of MPFS I. Instead of data just being sent through existing channels, it is transformed into a modern data structure. The data is wrapped into a blockchain transaction, signed by DTCC’s private keys, and finally routed to Chainlink’s Cross-Chain Interoperability Protocol (CCIP). This allows relevant fund data to be sent across almost any blockchain, private or public. Once the fund data is transmitted to these networks, a CCIP-based smart contract forwards the data to the Smart-NAV-specific smart contracts. These are responsible for validating permissions and storing data for parties to consume.

Next Month’s Calendar