Most stablecoins are pegged to the US dollar. They close the gap between the advantages of cryptocurrencies and the more stable fiat currencies. Various mechanisms exist to maintain the dollar peg. A complete overview from Tether (USDT) to TerraUSD (UST).

Stablecoins established themselves over the past years as essential pillars in the world of decentralized financial applications (DeFi). They are included in the highest-volume cryptocurrency pairs and are considered a safe haven against volatile cryptocurrencies thanks to their peg to a fiat currency. In addition to centralized, 1:1 fiat-backed dollar tokens such as Tether (USDT), the ecosystem also hosts over-collateralized and unsecured (algorithmic) stablecoins.

Parity to fiat backed stablecoins

Full collateralization with dollar deposits and money market investments is often considered the classic model. The first centralized stablecoin was launched in 2014 by Tether Ltd. and still takes up the bulk of the market. For every new dollar created in USDT, one fiat dollar must be deposited into Tether's reserves; when redeemed, the tokens are burned again. This is to ensure a 1:1 peg to the U.S. dollar at all times without having to fear the failure of an algorithm or a potential bank run.

The fiat-backed model is straightforward in theory, but requires regular auditing and a trusted financial manager. The latter must monitor that the token remains fully collateralized. In addition, reserves must be highly liquid to easily handle sudden withdrawals. The two biggest competitors to Tether's USDT are Circles USD Coin (USDC) and Binance USD (BUSD).

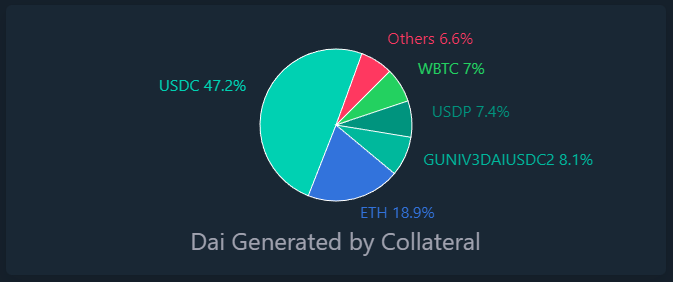

Crypto-backed stablecoins

Similar to fiat collateralized centralized stablecoins, crypto-backed stablecoins have a cryptocurrency deposited as collateral. These types of dollar tokens function much like a pawn shop. They allow users to use crypto assets as debt collateral and take out a dollar loan. The crypto collateral is provided in a decentralized manner via a smart contracts. These stablecoins counter volatility by overcollateralizing all loans and liquidating them in the event of a rapid drop in price.

On-chain issuance allows complete transparency and auditability of these reserves. The collateral is held in a smart contract and is only accessible through the clearing of the stablecoin debt. Alternatively, the smart contract can be closed and the collateral sold through the stablecoin system when the deposited collateral falls below a certain pre-determined level.

The biggest risk with this stablecoin model is the volatility of the underlying collateral. If the collateral loses too much value, the system becomes under-collateralized and fallback procedures could be activated, such as stablecoin liquidation. Ultimately, the volatility of the collateral portfolio determines the stability of the stablecoin, which is why the leading projects like MakerDAO (DAI) usually hold a large number of USDC.

Non-collateralized / algorithmic stablecoins

Algorithmic stablecoins make use of a different approach than collateralized dollar tokens. In this case, an algorithm/protocol acts as a central bank and is responsible for the stability of the binding. Unlike fully dollar-backed or over-collateralized stablecoins, the binding/collateralization takes place via the protocol's own token, the pricing of which depends freely on supply and demand. In theory, by minting and redeeming its own protocol tokens, the mechanism should be able to offset inflationary or deflationary trends of the relevant stablecoin.

In practice, the former largest stablecoin TerraUSD (UST) shows that such models only work with a steady increase in demand and, in the opposite case, react very vulnerably to disproportionate returns by investors. The concept of fractional or unsecured stablecoins may have met its early demise with Terra. UST thus very prominently followed countless failed attempts at under-collateralized stablecoins. As a hybrid model between algorithmic and crypto-collateralized, Frax Finance (FRAX) should be mentioned, whose price stability is guaranteed partly with collateral such as USDC and partly by an algorithm.

Corporate stablecoins

Leading banking institutions are also looking into creating their own digital stablecoins. One example is JP Morgan's JPM Coin and Facebook's Diem. Libra, as the initiative was called when it was launched in 2019, was originally intended to be pegged to a basket of fiat currencies and some other assets. However, the project faced strong headwinds from international regulators and was shelved.

In an effort to reclaim the rapidly growing stablecoin sector from the hands of private companies and back into the control of the state, many governments and central banks have begun their own experiments. Also known as central bank digital currencies (CBDCs), digital tokens would be issued directly by the resident central bank. Both the U.S. Fed and the European Central Bank (ECB) are exploring the potential of such a solution, with China's digital yuan already in circulation.