Currency Wars")

At the centre of every conversation about bitcoin is a much broader conversation - what is money? And to explore that question, we have to talk about central banks.

Money as a means to create empire has existed almost as long as history itself. This is not an article on the meaning of money. For that, we’d probably need Joe Rogan, a joint, and a bottle of whiskey. I digress. Julius Caesar is credited with the innovative idea to utilize coinage as more than just currency. By stamping his face on coins, Julius Caesar created one of government's most effective instruments of control. Since then, the issuance of money has been the privilege of countries.

Central banks evolved out of a world of physical cash - in the days of Caesar, we needed an entity to store and manage coins, and to manage payments and balances between parts of the empire. Today, central banks manage these payments and in turn, entire economies. Central banks still manage coin but now they move zeros and ones on a central bank database as opposed to moving coins around the royal treasury and the empire.

Banking on Blockchains

With the advent of cryptocurrencies, and later, the application of “blockchain” to well…. everything, central banks have now become intrigued by the potential to use “blockchain technology” to add a new set of tools to their policy toolkit.

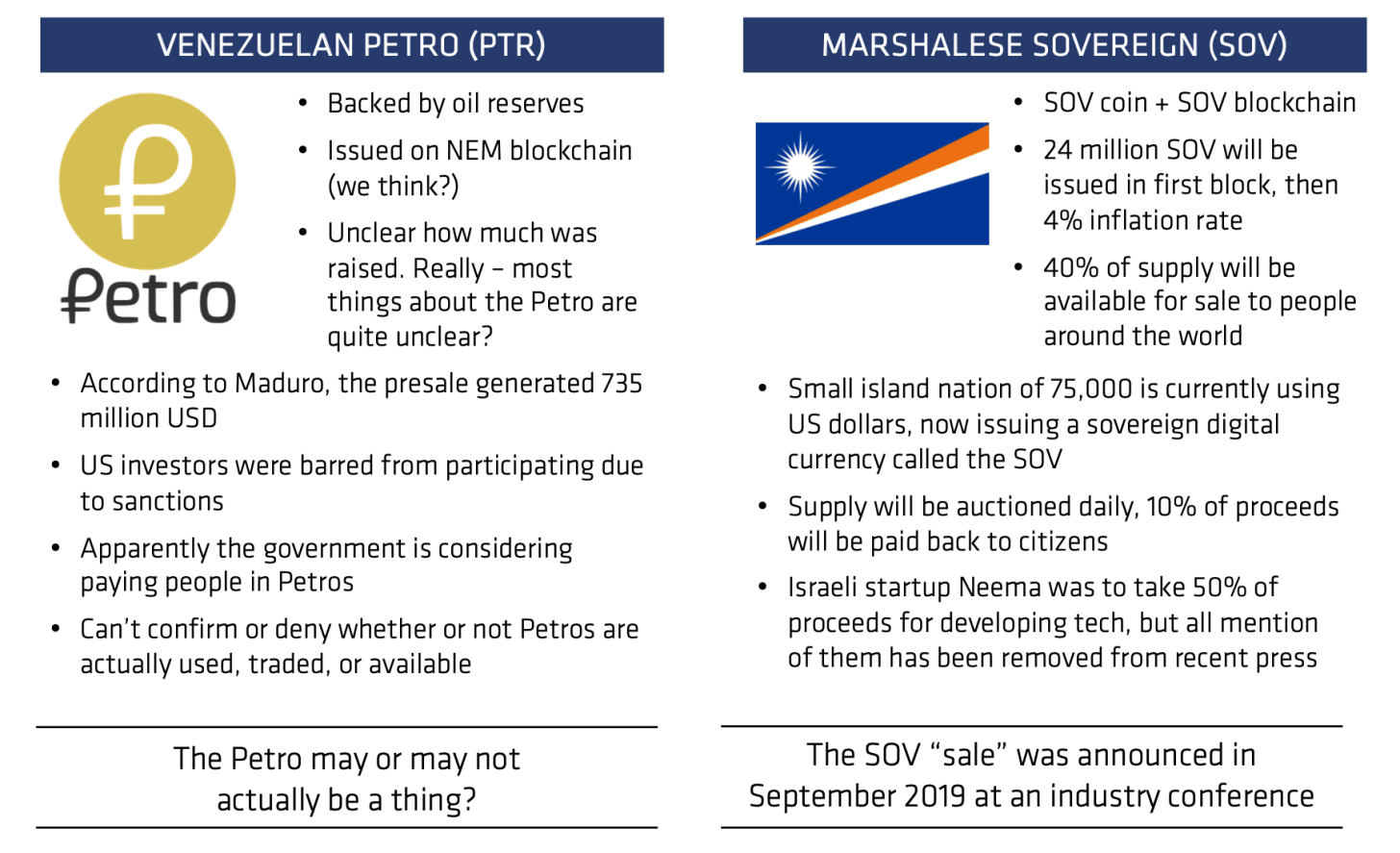

It started with Venezuela, who in 2017 attempted an “Initial Country Offering” by tokenizing their oil reserves and attempting to access global financial markets despite extensive sanctions limiting the country’s ability to do so.

It continued with the Marshall Islands having difficulty accessing capital markets for very, very different reasons. Because of its tiny scale and the remote nature of the island nation, it has trouble accessing capital markets to raise funds. They have explored raising funds via a token called the SOV.

Following Facebook’s announcement of Libra, every central bank is suddenly incredibly crypto-curious. In a recent report by the Bank of International Settlements (BIS), 80% of central banks are currently exploring issuing a central bank issued digital currency.

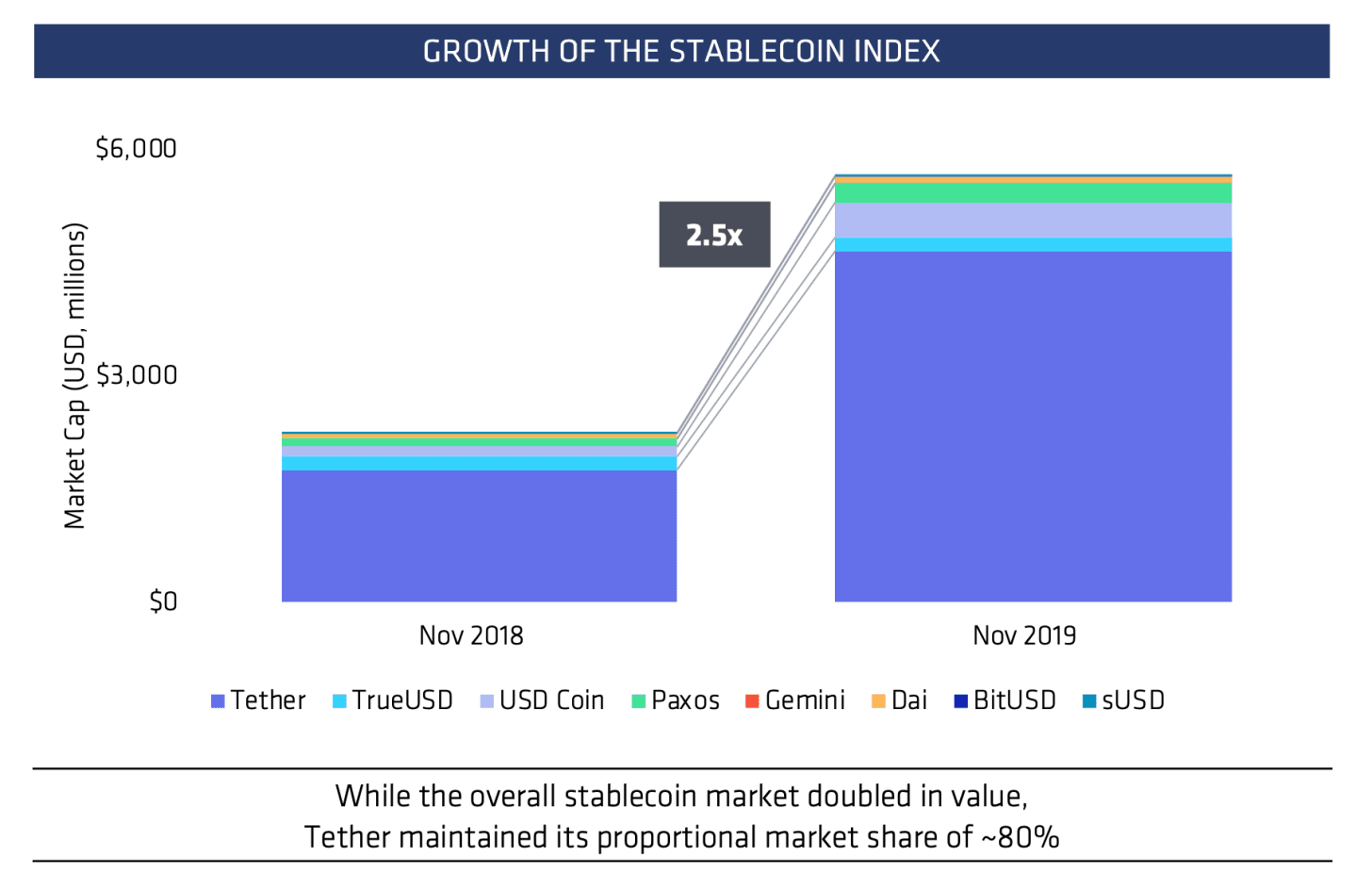

There’s also another handy statistic we should consider. While still small, the rapid growth and proliferation of stablecoins has been an eye-opening experience for central banks and the commercial banks who rely on them for liquidity. Consider the continued dominance of Tether, a stablecoin pegged to USD. Tether currently has a float in excess of $4B, and has spin-off at least $100M in fees per year. Tether is probably the most important asset in the function of the digital currency ecosystem, providing a payment mechanism native to each blockchain “ledger.”

All the Banks are Doing It

Currently many major banks are doing it. China, Bahrain, Vietnam, Thailand, India, the UK and the ECB. The World Economic Forum report on central bank digital currencies has in fact released an entire toolkit dedicated to exploring the various considerations for central banks embarking on this journey. This past week, Cambodia announced it will soon (real world soon, not crypto soon(TM) which is actually not soon at all but like, 2 to 3 years later) launch a “quasi” central bank digital currency. Cambodia is a great way to explore what issuing a central bank digital currency actually means.

A Blockchain Named Bakong

The National Bank of Cambodia (NBC) has set up a platform called Bakong, a private blockchain network built by the Japanese blockchain software development firm, Soramitsu, which has its own native token, a digital wallet, and features optimized for wallet to wallet payments. The token is a basket of USD and Riel, the Cambodian national currency, and can be obtained by users who deposit money in account at banks. There are currently 11 banks participating in this platform, and I assume each of these banks will effectively participate in this tokenization scheme as an “Authorized Participant” or AP. This term comes from the world of ETFs, where APs are one of the major parties at the centre of the creation and redemption process, and provide a large portion of liquidity in the ETF market by obtaining the underlying assets required to create a fund. Here, these member banks will hold assets, issue tokens to their customers for use in this payment network, and redeem tokens back into the underlying currencies. so, anyone with a bank account with these 11 banks in the network can send money to each other. It would seem that this could be a great way for things to work.

The question is why would Cambodia do this? The why is always where the magic is.

If you read the published literature, much of the logic behind Bakong is about improving the fragmented payments ecosystem in Cambodia, which is mostly cash based, and to drive more electronic payments via the wallet and its native currency. Of course, the primary objective is the unbanked. Clearly financial innovation is going to rescue them. And here, it actually might make sense for once. The average Cambodian lives on $3 a day, and having a very low cost, efficient payment system that allows for all sorts of fintech innovation could in fact help introduce cost-effective financial products and services. This is an exciting development, and indeed one to be celebrated, although I’m not sure if a blockchain is really needed.

Why Bank on a Blockchain?

After reading about Cambodia’s plans to bank on the Bakong network, I started to ask why. And if we look at the story behind the headline, a much more interesting narrative emerges.

Reducing Dollar Dependence: Cambodia’s economy has historically been based on the US dollar. The local currency, the Riel, is not widely used. Roughly 84% of transactions in Cambodia are denominated in dollars - not Riel. This means that Cambodia’s economy is highly susceptible to US monetary policy. Because the central bank can now exert control over the mix of assets that make up the Bakong system’s native token - which is currently set to include USD and Riel, but in the future, could include a broader mix of currencies, the NBC can start to actively monitor and manage the impact of monetary policy set by other central banks, most specifically, the US.

Influencing Current Account Balances: The current account balance is an important metric for economies to measure and track. The current account is the sum of the balance of trade (exports aka what you sell to other economies minus imports aka what you buy from other economics), income from abroad, and transfers abroad. A positive balance indicates the country is a net lender to the rest of the world, while a negative current account balance indicates that it is a net borrower from the rest of the world.

Cambodia, as you might have guessed, has a large net negative account balance. Much of the country’s economy is dependent textiles and tourism, and the average income is around $1,500 per person. Cambodia’s gross domestic product is roughly 23 billion USD. Its net account balance is negative 3 billion USD, meaning it’s a net borrower.

The current account balance is influenced by a wide range of factors – but most important are trade policies, which impact the balance of imports and exports, and controlling and managing the exchange rate, which is much easier to do when you control the means of payment and the national payment networks. The Bakong system is currently focused on payments within Cambodia, but the NCB has already expressed its intentions to open the network up outside the country as well.

So effectively the NCB will now have a way to manage financial flows into and out of the country. More importantly, it will be a way to manage the basket of currencies that makes up these payments, presumable working to minimize its economic dependence on dollars and optimize its own currency’s competitiveness.

Economic Data Gathering and Controls: Lastly, it's important to note that anyone participating in the Bakong system will be required to attach their digital wallet to the bank account in order to exchange payment tokens for currency, and back. It has historically been challenging for cash driven economies to gather economic data and for central banks to implement effective policies, especially when the cash economy is driven by dollars.

With the move to a digital payment system that is supported by the majority of commercial banks and the central bank, one side effect is minimizing the USD shadow economy and capturing data on payment flows and implementing more effective controls. This could be used for levying taxes on these flows that have historically happened outside the system, limiting daily transactions between wallets, or perhaps even blocking certain individuals from using the digital payment system.

You don’t necessarily need a digital currency or a blockchain to do this - notably, India removed high value bills from circulation in 2016, as an effort to “curtail the shadow economy and reduce the use of illicit and counterfeit cash.” The ban on higher value bills was coupled with a digital payments and digital identity scheme, and the demonetization effort was intended to boost adoption of these schemes.

China has already implemented a financial surveillance system without the use of a blockchain, but intends to digitize the Renminbi over the coming years. Surveillance capitalism isn’t just for corporates - everyone can play!

Currency Wars on a New Frontier

So the real conversation we now get to, and the one I’m excited about, is the future of currency wars. All one has to do is look at the headlines to see this is already happening. In October of 2019, Rosneft, Russia’s largest oil company, announced that it would no longer be using dollars for its contracts. The reasons for the switch were reducing dependence on the dollar, but more importantly, reducing the impact of US sanctions on Russian trade with Venezuela.

During the recent trade negotiations between China and the US, fears of digital renminbi have loomed large, and in a hearing about Facebook’s Libra, Mark Zuckerberg just came right out and said it -

“China is moving quickly with the launch of a similar idea in the coming months,” he said. “Libra is going to be backed mostly by dollars and I believe that it will extend America’s financial leadership around the world, as well as our democratic values and oversight.”

Central bank digital currencies are going to usher in a new era and new form factor for currency wars, and it’s going to be very interesting to see what protocols, networks, and product and service providers end up being the vendors of choice to the best customers in the world - governments. We like to think that startups are made out of magic and stardust, but we forget that Silicon Valley owes much of its legacy to the needs of the military industrial complex. And we see an increasing number of companies in the Valley focused on solving problems for not only enterprises and consumers, but also the largest and most complex institutions in the world - our governments. The trillion-dollar dot com poster child, Amazon, is well on its way to becoming one of the largest US defense contractors.

So in this era of digital currency wars, many of today’s infrastructure providers operating in the cryptocurrency space will likely have a significant role to play in the future of central bank digital currencies. As an early stage venture investor with six years and 150+ companies in the crypto ecosystem under my belt, I have a lot of thoughts on the who, what, where, and how. That’s a much longer conversation saved for another day.

Lastly - wrapping this up because it’s getting long and I tend to overdo these things - this tweet succinctly sums up my thinking. If every central bank, corporation, and power-hungry entity decides to issue its own digital currency, what will be the neutral choice for international trade? Does the medium actually change the message? And most importantly, where will market activity flow?

I’m about two sentences away from putting #BitcoinFixesThis in here, so let me spare us all the rocket emojis. The current state of central bank digital currencies has many people playing out this chess game in their heads and realizing why bitcoin is so powerful - it belongs to no state, government, or country. And that is something that we can all be excited about.