Stablecoins are systemically important to crypto markets, but they are coming under increasing scrutiny both inside and outside the industry. In this article, we explore the "three stablecoin problem" and examine the interactions between BUSD, USDC, and USDT.

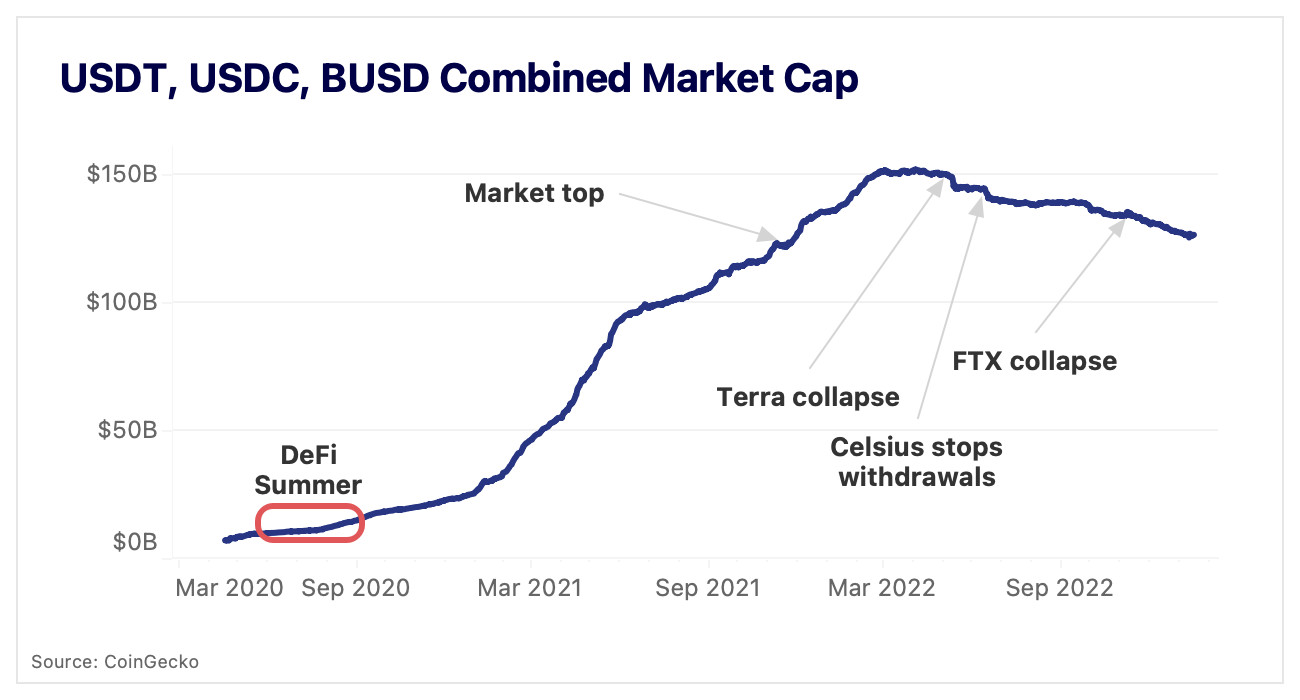

In six years, stablecoins have grown from making up just 1.5% of BTC trade volume relative to fiat currencies such as the Dollar or Euro, to more than 87%. This has been matched with an explosion in market capitalization for the three largest centralized stablecoins: Tether (USDT), USD Coin (USDC), and Binance USD (BUSD). The three had a combined market cap of $10bn in May 2020, the start of DeFi Summer. By January 2021 this figure had grown to $30bn, eventually reaching a peak of $150bn in the spring of 2022.

Since then, however, their combined market cap has been on a steady decline, with some sharper dips coming during major market events. Interestingly, they each peaked on different dates in 2022: USDT at $83bn on April 30 (a week prior to Terra collapsing), USDC at $56bn on July 1 (as 3AC and Celsius went under), and BUSD at $23bn on November 15 (as FTX collapsed).

Herein lies crypto’s version of the three-body problem: these three stablecoins necessarily interact with each other, but this interaction is chaotic and lacks reliable patterns. Today, we explore how these three stablecoins interact with one another, and what this means for their role in markets.

Various redemption mechanisms

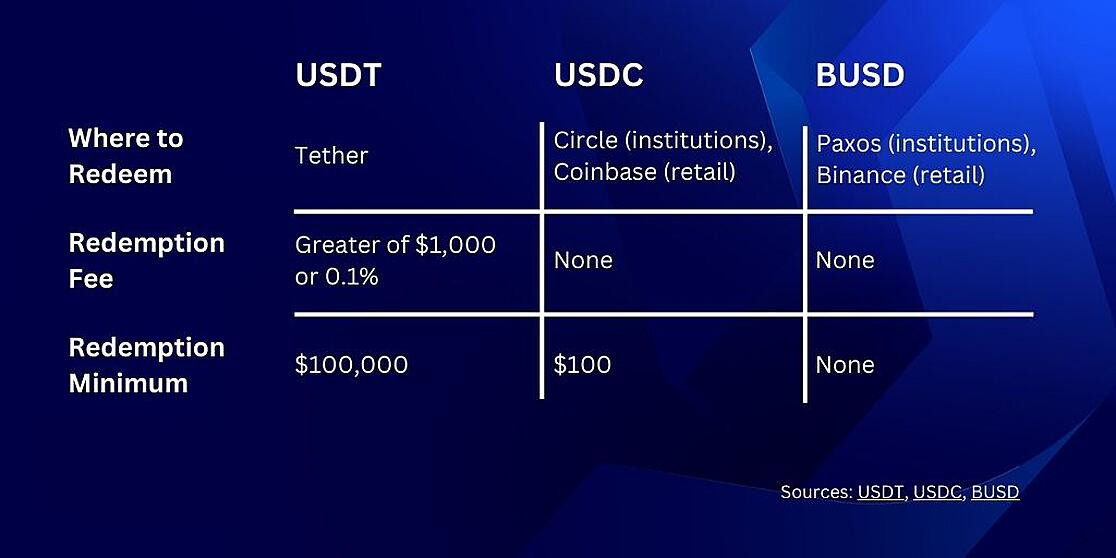

Before looking at the flows between these three stablecoins, it’s important to understand their redemption mechanisms, which are outlined below. Redemptions essentially function as a pressure release valve; when there is too much supply of a stablecoin, the supply can be reduced through redemptions. The alternative would be unwanted supply being sold, which could lead to depegging.

While the three function in essentially the same way, there is a larger barrier to entry to redeem USDT compared to USDC and BUSD. This has the effect of making USDT supply stickier relative to its peers. This also means that traders who don't have the minimum $100k required to redeem often resort to spot markets to off-load their USDT. Thus stablecoin-stablecoin pairs, particularly involving USDT, are vitally important, as they allow users – especially retail users who may not have a Tether, Circle/Coinbase, or Paxos/Binance account – a means to divest from stablecoins they perceive to be riskier.

Volumes develop dynamically

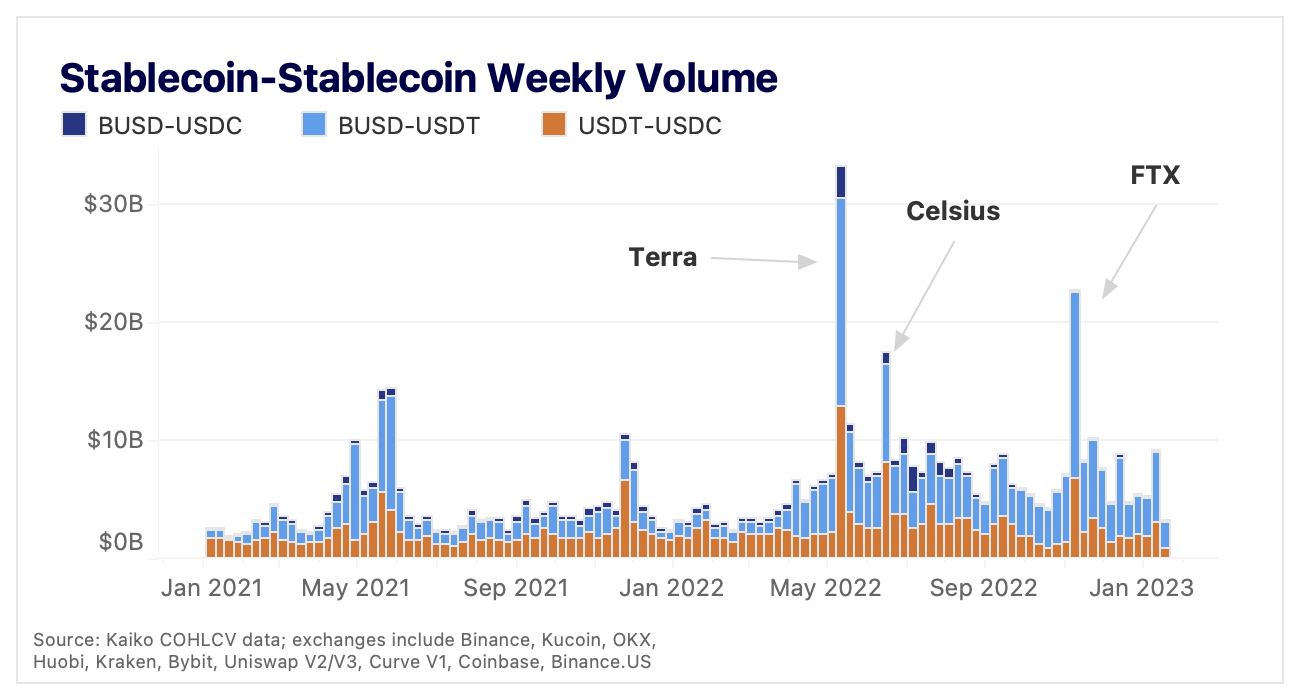

Given the relative difficulty of redeeming USDT, we might expect to see that users, especially retail, opt to swap into another stablecoin (instead of redeeming) during times of stress. This has largely been borne out in the data, with the three highest weeks for stablecoin-stablecoin volume being Terra’s collapse, Celsius halting withdrawals, and the FTX collapse.

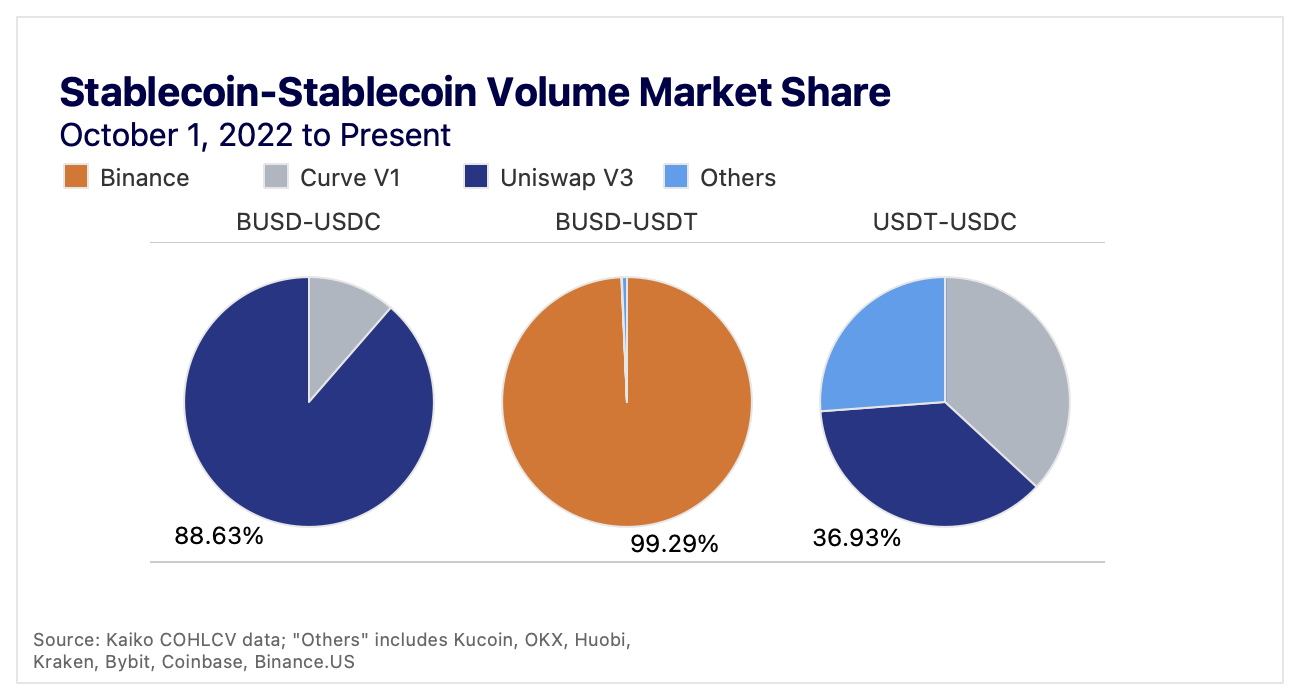

Notably, nearly all of the volume involves USDT, while BUSD-USDC swaps are extremely low, with just 0.27% market share among the three combinations of stablecoin swaps since the beginning of 2023 compared to 8.5% in 2021. This becomes more interesting when examining the exchange breakdown for each pair of stablecoins. [All data include bi-directional swaps. For example, USDT-USDC encompasses volume for all USDT-USDC and USDC-USDT trading pairs.]

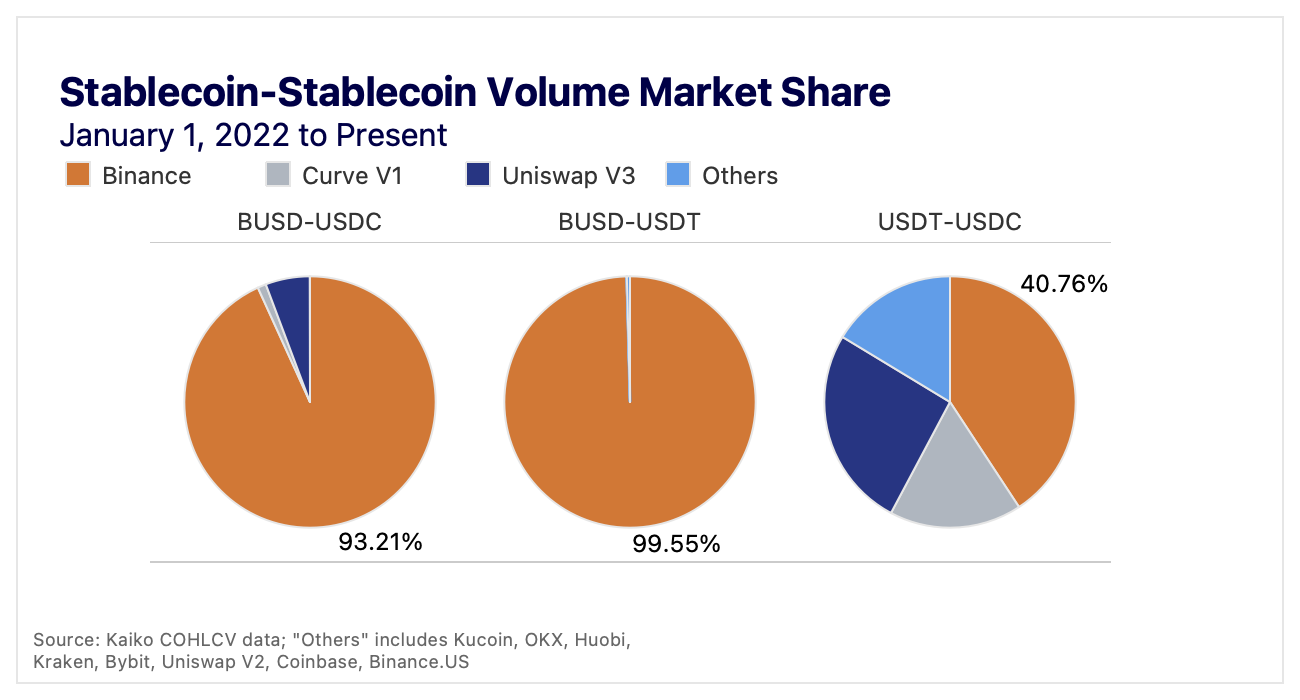

Binance dominates the relatively low volume BUSD-USDC pair, with Uniswap v3 coming in a distant second at 5.7% market share. Binance facilitates nearly all volume of the much higher volume BUSD-USDT pair. Finally, Binance holds just a 40.76% market share of USDT-USDC volume, followed by Uniswap V3 at 25.9% and Curve at 17%. However, there’s a catch here, as Binance delisted USDC (as well as USDP and TUSD) in September 2022. Since October, the market share has looked very different:

Uniswap V3 has dominated BUSD-USDC volume, Binance has nearly all BUSD-USDT volume, and Curve and Uniswap V3 have almost identical USDT-USDC volume. Binance delisting USDC has decentralized activity for the USDT-USDC pair. Here we’ll briefly pause to appreciate decentralized exchanges, which have only existed for about 5 years. USDT-USDC can be considered a systemically important token pair, and two DEXs have jumped in to pick up Binance’s market share.These two DEXs, Curve and Uniswap, are each facilitating more volume than 7 of the largest CEXs combined. A lack of CEX liquidity on the USDT-USDC pair has paved the way for DEXs to claim Binance’s market share of volume for the pair.

Curve liquidity still leading the way

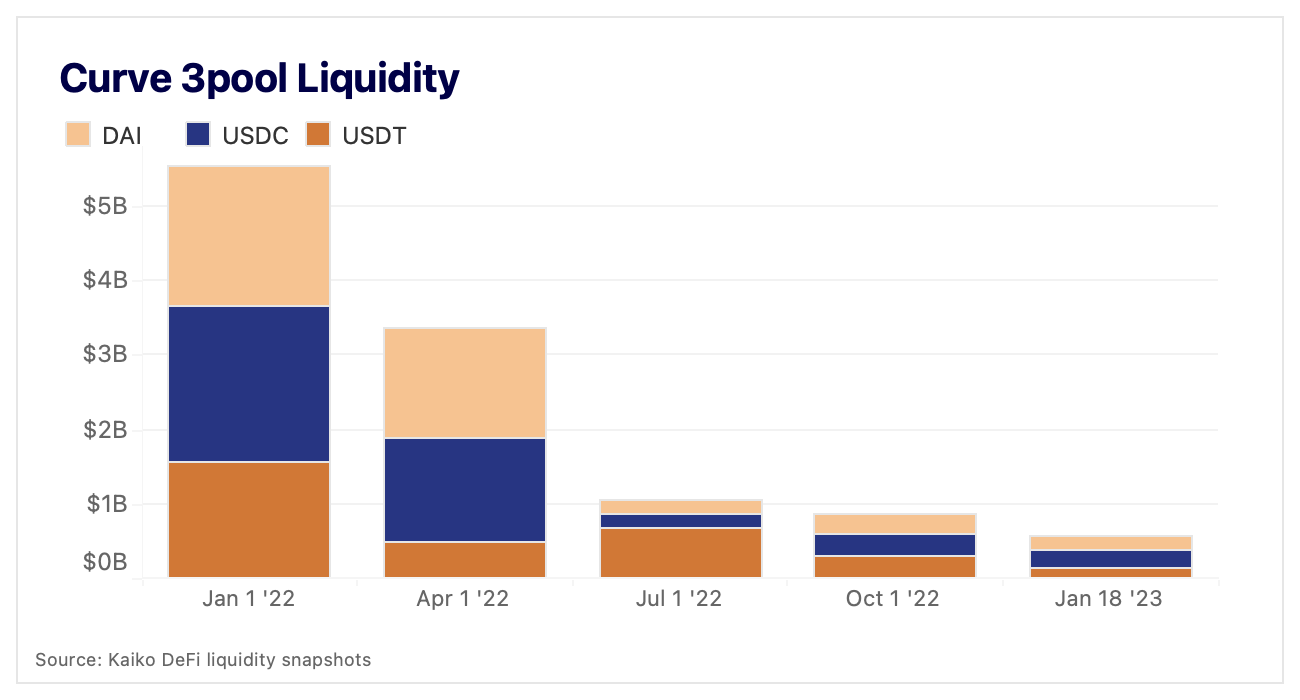

While Uniswap has higher volume, Curve holds far more USDT-USDC liquidity (despite TVL decreasing over 90% in the past year), with $200mn USDC and $169mn USDT in the 3pool compared to $50mn total in the largest Uniswap USDT-USDC pool.

As discussed in a previous Deep Dive, the makeup of a Curve pool can give an idea of sentiment around a stablecoin. For example, in July 2022, USDT made up around 70% of the 3pool as old fears about its peg and backing resurfaced in the post-Terra fog. This is due to a combination of users swapping out of USDT and into USDC and DAI – essentially taking USDC/DAI out of the pool and putting USDT in – and users disproportionately removing USDC and DAI liquidity.

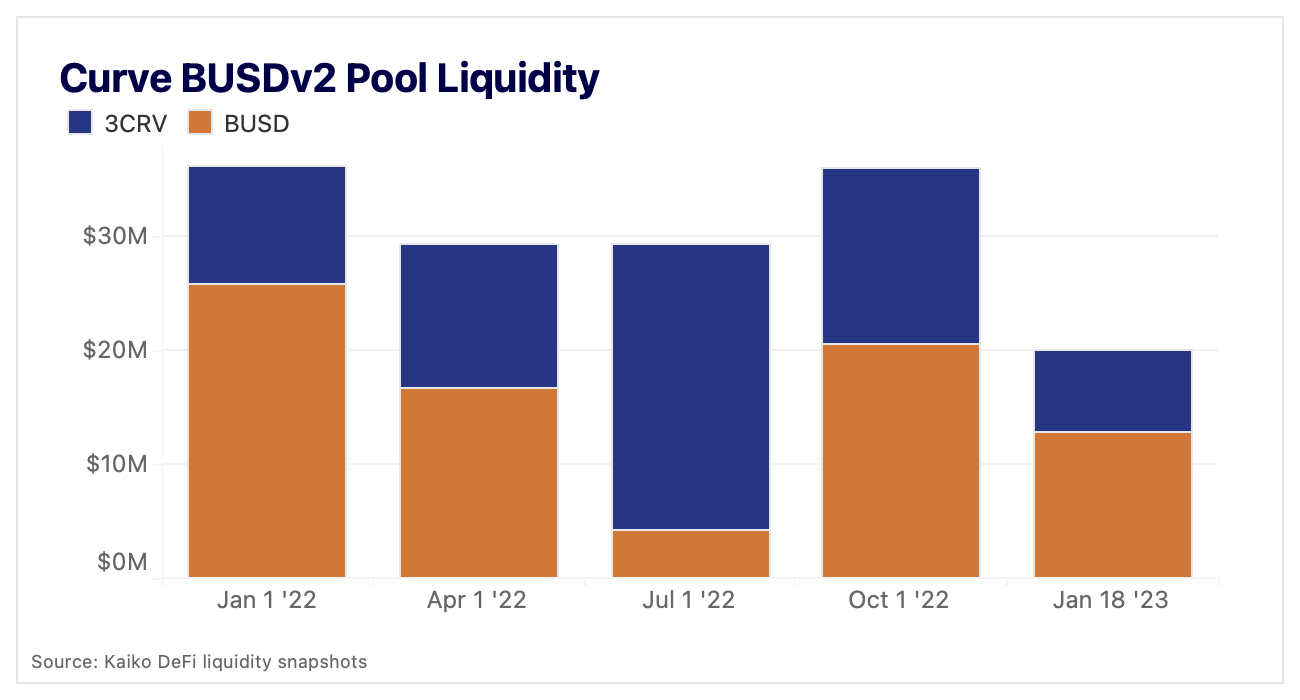

USDT’s proportion of the pool has been very volatile, in large part because it is far easier (and potentially cheaper, as it does not have Tether’s 0.1% redemption fee) for users to swap out of USDT in the Curve pool than to redeem directly with Tether. BUSD, meanwhile, has far less liquidity on Curve; its makeup of the BUSDv2 pool has also been volatile, though its TVL has not experienced as severe a drawdown as the 3pool.

DeFi-wise, BUSD is more popular on BNB Smart Chain (BSC). BSC’s largest DEX – PancakeSwap – holds $70mn in BUSD-USDT liquidity and $50mn in BUSD-USDC liquidity. Ultimately, BUSD’s DEX liquidity is far exceeded by its liquidity on Binance.

DEX trade flows

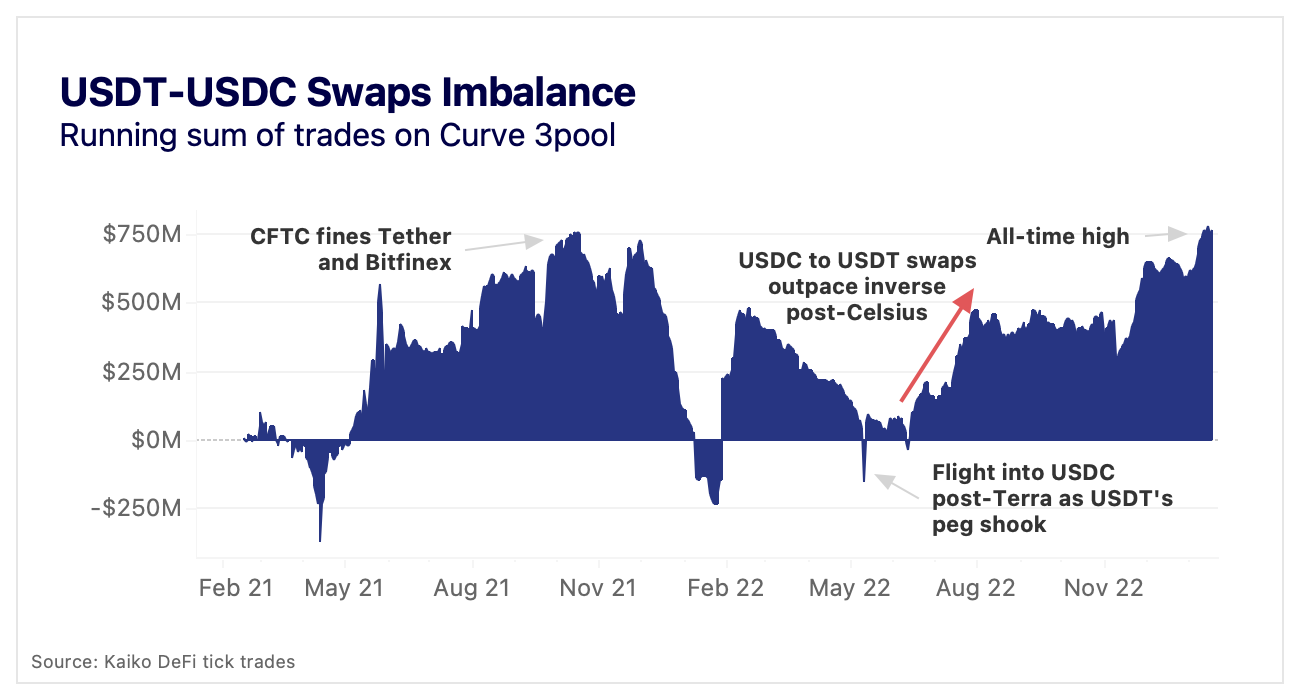

Additionally, Curve’s mechanics allow for large imbalances in token flows. The highest volume stablecoin-stablecoin swap on Curve is USDT-USDC. The chart below shows how the direction of flows has changed over the past two years; an upward slope indicates that swaps of USDC into USDT are outpacing swaps of USDT into USDC.

The most dramatic shift in flows came after the market peaked in November 2021, with a nearly $1bn shift towards USDC from November 30, 2021 to January 24, 2022. The trend flipped back again as the market rallied in February and March 2022. This reflects the general narrative that USDT is in greater demand when trading activity is higher, while USDC is seen as safer during bear markets.

However, this trend was largely bucked in the past few months (recall that Binance stopped USDT-USDC trading in September), as the imbalance surged to an all-time high a few days ago. We would expect USDC to be in greater demand during the last couple of turbulent months for crypto, but the trend towards greater USDT demand showcases the unpredictable and dynamic nature of the interactions between stablecoins.

Conclusion

That was a lot of charts, so what does it all mean? While all three stablecoins have slightly different niches – USDT is the original trading stable, USDC is used in Ethereum DeFi, and BUSD is used on Binance and BSC – the three are constantly interacting in new and unpredictable ways. These chaotic interactions are made even more unpredictable by the centralized entities that issue them.

While it went relatively under-the-radar, Binance’s move to phase out USDC created a massive shift in market structure that decentralized the USDT-USDC pair. Market participants should be aware of Binance’s immense market share of the BUSD-USDT pair and consider the nonzero possibility that the exchange phases out USDT, which would be the largest shock to the three stablecoins yet.