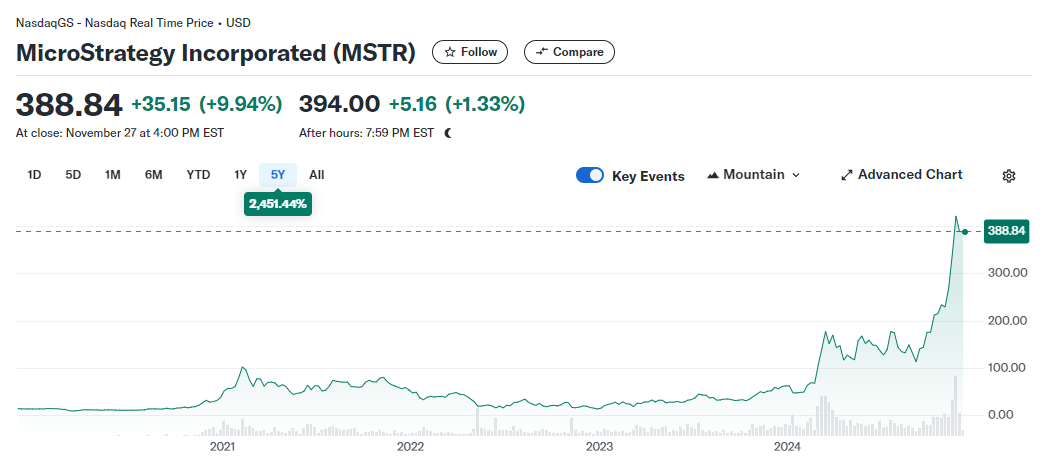

Since 2020, software developer MicroStrategy has taken on billions in debt to acquire bitcoin. So far, the strategy has paid off. The company's stock is at an all-time high. But how does Michael Saylor's bitcoin strategy work, and does it pose a risk to the industry?

Before entering the bitcoin market, MicroStrategy was primarily a business intelligence and analytics software company, providing tools for data-driven decision making and corporate reporting. However, this business had been stagnant for more than a decade. The company could not reinvest its remaining cash in a scalable way. So in August 2020, MicroStrategy CEO Michael Saylor decided to make an initial investment in bitcoin. After evaluating various asset classes, the company concluded that investing in "digital gold" was the best use of its reserves. The strategy paid off when bitcoin hit an all-time high in December 2020 and MicroStrategy's stock soared. Saylor discovered a seemingly endless cycle of capital generation.

MicroStrategy Becomes a Bitcoin Hedge Fund

Instead of simply investing excess profits in bitcoin, MicroStrategy began taking on debt to fund its purchases. This was done primarily through convertible bonds. Convertible bonds are a type of corporate debt that allows investors to convert their bonds into a predetermined number of shares of the issuing company. These bonds combine the characteristics of debt (regular interest payments) and equity (potential for stock appreciation).

Due to significant price increases, MicroStrategy has seen strong demand for long-dated (2027+) convertible bonds with low interest rates (below 2%). Buyers of these bonds are less interested in the interest payments and more focused on the upside potential of the stock.

The company channels all the capital it raises directly into bitcoin. The billions of dollars of buying pressure helps drive the price of bitcoin even higher. These investments increase in value, which supports MicroStrategy's stock price. Saylor then gains access to more debt. The CEO plans to continue this cycle indefinitely-as long as there is demand for the company's bonds. By 2027, MicroStrategy aims to raise more than $42 billion to invest in bitcoin. In November alone, the company secured $5 billion at zero interest, according to press releases.

A sustainable strategy?

In essence, Saylor is selling call options on MicroStrategy stock to accumulate as much bitcoin as possible. Bond holders include insurance giants like Allianz, who find the potential price gains more enticing than the typical 5% annual returns of conventional bonds. If the price of bitcoin doesn't rise enough, investors simply get their money back. They only bear the opportunity cost and the risk of MicroStrategy's insolvency. This leveraged bitcoin strategy is now priced at a premium to the company's assets. To date, MicroStrategy has purchased 386,700 bitcoins worth $37 billion for $21.9 billion, at an average price of $56,761 per bitcoin. With a current market valuation of nearly $90 billion, this results in an approximate 2.4x multiple on the company's assets.

Some investors view this valuation as a sign that MicroStrategy's stock is relatively overvalued. Last week, prominent short seller Citron Research announced a short position, arguing that the company's valuation is completely disconnected from bitcoin fundamentals. After all, there is no direct mechanism to exchange bitcoin for stocks. What's more, MicroStrategy is not obligated to pay back its loans until 2027 at the earliest. As long as the price of bitcoin continues to rise, the cycle works. Only a significant price crash in the distant future might force Saylor to sell some of his holdings.