")

In light of the increasing digitalization worldwide, the European Central Bank (ECB) has been exploring the possibility of introducing a digital Euro since 2021. The digital Central Bank Currency (CBDC) is intended to serve as an alternative to cash and other digital payment means. An updated timeline.

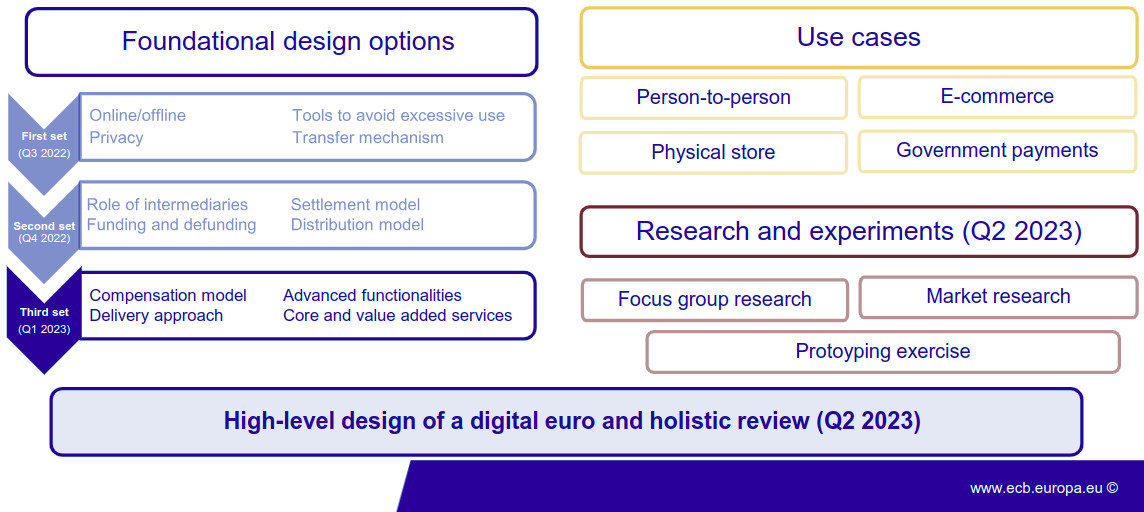

At the start of 2023, the European Central Bank (ECB) has announced a market study on the technical design of the possible components and services of the digital Euro in the form of a CBDC. The aim of the investigation is to gain insights into the possible features, functions, and user needs of a digital Euro. The report on the results of this market research is expected to be released in the 2nd quarter of 2023.

Accessibility and interoperability

One of the main goals of the digital Euro is that it can be used anywhere within the Eurozone, just like current cash. Whoever receives a digital Euro payment instrument from an intermediary in one country should be able to use it freely at any merchant in the Eurozone, regardless of the intermediary and the country of the merchant. This is intended to ensure that the digital Euro is widely accessible and easy to use for individuals and businesses, and aligns with the principle of the Euro.

The ECB is also focusing on interoperability and working to make the digital Euro compatible with other digital currencies. This would facilitate cross-border use and enable individuals and businesses to make cross-border transactions. To this end, the ECB is working at the international level to establish common standards and protocols for CBDCs. These efforts aim to enhance the strategic autonomy of the Eurozone by reducing its dependence on foreign payment systems, and increase economic efficiency by curbing market-distorting behavior.

Broad market participation

In order to achieve these goals, the ECB aims for broad market participation in the development of the digital euro system. Through close collaboration with market participants, the ECB hopes to establish a set of common rules, standards and procedures that will:

- Ensure coverage throughout the eurozone and a harmonized payment experience for end users

- Retain flexibility to respond to user preferences and habits

- Grant the market a high degree of freedom in the dissemination of the digital euro and the development of innovative front-end solutions

- Support market participants in offering payment services at the European level

By involving a wide range of market participants, the ECB aims to create a digital euro that is widely accessible, easy to use and efficient for both individuals and businesses. The central bank views the introduction of a CBDC-euro as a necessary step in keeping pace with the evolving digital landscape and ensuring that the euro remains a strong and resilient currency in the digital age.

Supervised intermediaries as central players

The European Central Bank views intermediaries as key players in the provision of a CBDC as a public good. The ECB hopes that intermediaries such as banks will act as direct points of contact for individuals, merchants, and businesses, providing all end-user services and developing innovative payment and financial services based on the digital euro.

However, it is important to consider potential conflicts of interest and the need for appropriate oversight of intermediaries to ensure that personal data of individuals cannot be misused. Strong public-private collaboration is essential for the success of the digital euro, but it must also come with regulations and controls to protect the privacy of EU citizens. The decision on appropriate data protection controls is however delegated to the European Parliament by the ECB.