– a fundamental analysis")

Bitcoin must be valued as a form of money and theorise a new framework for measuring bitcoin’s progress towards a theoretical end state where it meets all global monetary use cases. A fundamental analysis of Bitcoin's total addressable market (TAM).

In this post, we review once again bitcoin’s potential as a contender competing with other global monies, why we find a Total Addressable Market (TAM) approach is the best way to evaluate bitcoin. While it may not be likely that Bitcoin (BTC) seizes the total market share of all other forms of monetary items, bitcoin is certainly competing against them and therefore has the potential to capture their usage.

Bitcoin has no appreciable alternative use case outside of money and it is therefore inappropriate to consider valuing bitcoin as one might for a commodity with industrial utility (Nickel, Copper, etc.), an equity with promise of future cash flows (Coca Cola, Apple, etc), or a debt security with yielding interest payments (US treasury, Commercial Paper, etc.).

Bitcoin will continue to absorb an increasing share of the global demand

For bitcoin to increase in value, it must both perform better as a store of value and become easier to sell at any time, place as well as scale properly. Many items have performed these monetary functions. However historically the items that have done this best have been characterised by certain monetary properties. In our view, it is these properties that set each item apart, increasing (or decreasing) their ability to perform meaningful monetary usage and ultimately determining the value they will capture relative to other competing monetary items.

The idea that bitcoin will become more valuable in the future, better perform monetary functions and in turn compete for greater use as a global money, is therefore dependent on its ability to provide preferential monetary properties. But more specifically, it is based on the following principles holding true:

- It's fixed properties continue to make bitcoin suitable to monetary use cases.

- It's relational properties, such as volatility and liquidity, continue to improve.

- The context of the current economic environment changes such that bitcoins’ properties are more desirable relative to other global money competitors.

Bitcoin fulfills a lot of important monetary properties

When an investor chooses to store their value in US treasury bonds as opposed to gold, it is because they believe that in their individual circumstance US treasury bonds have preferential properties, making them better suited to store value. For such an investor, it may be that US treasuries are more liquid and transferable than gold, given their digital nature and level of market depth across global trading venues, it may also be tactical in nature, believing that the US Dollar is likely to appreciate.

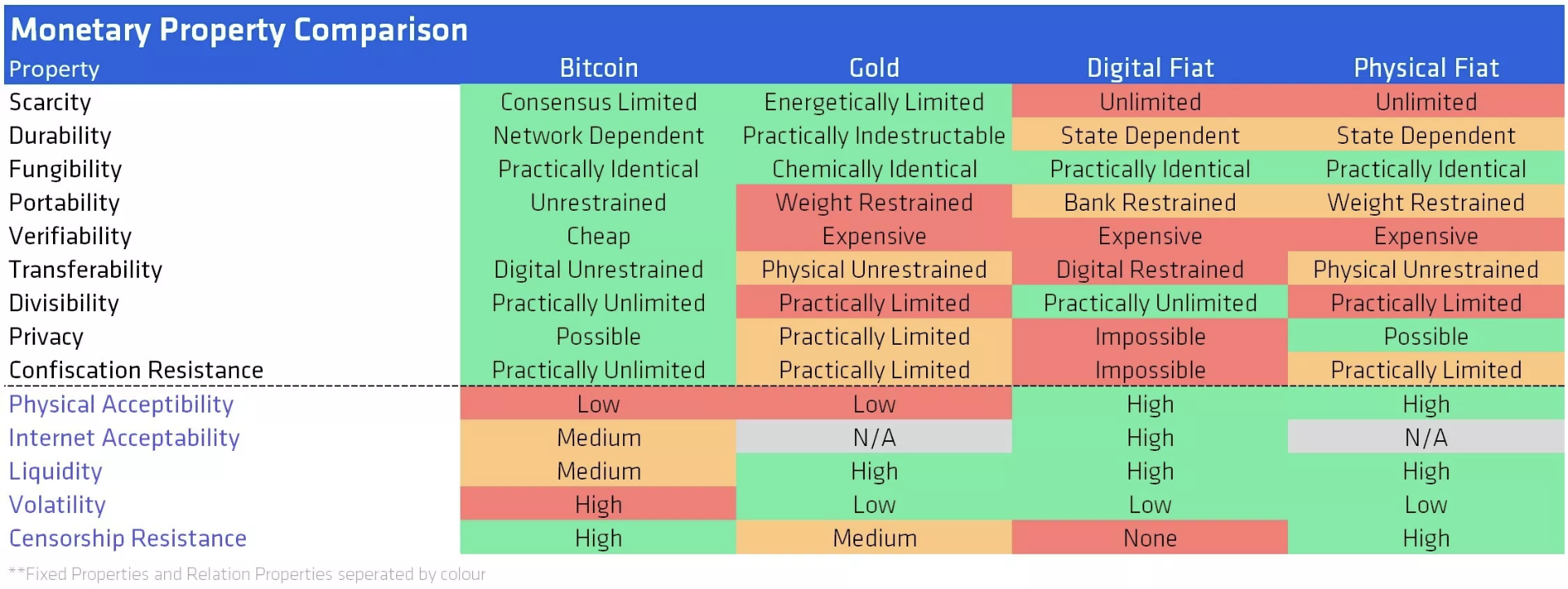

But maybe the desire for certain properties may fluctuate based on the context of an individual’s circumstance, the chart below lists the properties that we’ve found to be the most consistent among historically used monies, as well as how bitcoin fares in comparison to other prominent monies of today and the characteristics that underpin each fixed property.

It is not a coincidence that bitcoin scores well in many historically significant monetary property categories. It was designed specifically with monetary properties in mind, as evidenced by its original stated purpose of serving as a form of electronic cash with a predefined, unchanging and finite supply schedule.

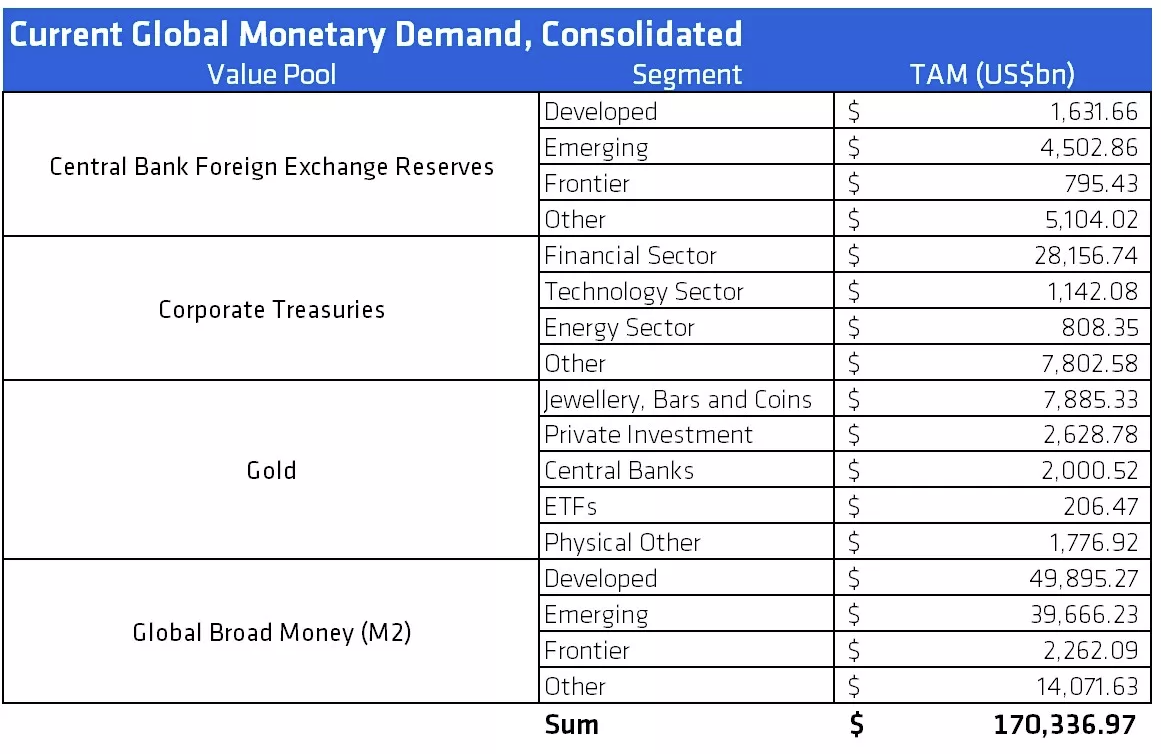

Current global monetary value

To approximate the size of the current global demand for money, we consider the value of pools of monetary assets that are currently and most clearly fulfilling monetary functions. We’ve chosen four pools: above-ground gold, central bank foreign exchange reserves, corporate treasury assets, and global currency (M2).

While these pools do not represent all forms of monetary value, or all of the possible demand that may flow into bitcoin, we find these pools likely represent the lion’s share of the future potential of bitcoin. Thus, we believe they represent a reasonable and simple upper bound to the future value that could accrue to bitcoin. The TAM model relies on bitcoin gaining market share from these separate value pools, with the following four assumptions:

- The first assumption is that bitcoin could completely or partially replace the use of gold as a monetary store of value. Bitcoin’s fixed monetary properties are superior to gold while having a few current shortcomings in its relational properties, such as volatility and liquidity, which we expect will each improve with greater monetary usage.

- The second assumption is that bitcoin will, to some extent, be used as a reserve asset by central banks, who will continue to issue their own local currencies on top of a set of monetary reserves including gold and foreign exchange assets. However, at the time of writing, very few central banks have direct exposure to bitcoin as part of their FX reserves.

- The third is that bitcoin is and will continue to be used by businesses as a long-term treasury asset or cash reserve and thus could replace some or all of the currently held monetary reserve assets, such as US Treasury Bonds.

- The final is that bitcoin is being used by individuals as a general savings tool and can therefore continue to take market share from commonly held global government monies (M2), which we separate into frontier, emerging, and developed market currencies based on MSCI’s Country Classification Index.

Bitcoin market capture of current monetary value

Our model offers several scenario-based estimates for the amount of monetary demand bitcoin could capture in the future. Each scenario assumes a different combination of percentages that may accrue from each value pool above, and is separated into optimistic, baseline, and pessimistic cases.

Note that bitcoin may eventually receive none or all of the demand from each value pool and such demand will almost certainly be changing to varying degrees at different times. This is why, for the sake of simplicity, we take a long-view forecasting several potential end-state market capture scenarios.

Our hypothesis is that bitcoin has the greatest opportunity to gain use in countries where bitcoin’s current adoption rate is already the highest and whose economic environment makes bitcoin’s unique combination of monetary properties highly competitive.

Summary

From a valuation perspective, bitcoin has a large potential upside even if the extent of the upside is unknowable in advance. The global market for money is the largest in the world and the potential benefits of owners of successful monetary assets is significant. In less than 15 years, bitcoin has already established itself as a nascent, yet serious contender in the global competition of monetary items.

Our thesis is that its fixed properties are highly beneficial and unchanging, such that there is no deterioration in bitcoin’s ability to perform the core functions of money over time. However, its relational properties will continue changing for the better as its usage grows. As an added bonus, contextual changes in the global economic environment may then also favour bitcoin. Taken together, these factors suggest that bitcoin will continue to absorb an increasing share of global demand for money.