2022 was marked by a series of high-profile bankruptcies of various multi-billion crypto companies. FTX is yet another collateral damage of an industry that, blinded by an unprecedented bull market, completely ignored the possibility of a credit crisis and thus took itself down.

How was it possible that within a very short period of time, thriving crypto companies with former quarterly profits in excess of hundreds of millions of dollars suddenly filed for bankruptcy? To answer these questions, we need to turn back time a bit, because the foundations of the current wave of insolvencies were already laid at the beginning of the year - just a few weeks after the end of the prolific 2021 bull market.

There is a clear pattern that has already run through many historical financial crises: a perfect market environment tempts profit-seeking players and speculators to an increasing appetite for risk in search of even higher returns. When the spiral of credit-fueled investment excesses ends, the most reckless fall first. Over time, the subsequent "contagion effect" brings out all those who have bet too high.

Financial crisis 2008 revisited

Parallels between the 2008 financial crisis and today's situation in the crypto markets are obvious. A group of semi-regulated financial players are chasing appealing returns that are even higher given easily available debt financing. The game is made simple because loans can be secured with illiquid, second-rate collateral. What used to come across as a bunch of junk mortgages in AAA clothing was replaced with self-created "utility" or "governance" tokens in the digital age - leaving you in the exact same situation.

However, there is one difference to consider between old-world and new-world financial crises. In the digital asset sector, there is no central bank artificially keeping selected "too big to fail" coma patients alive with freshly printed money. And a second point should be communicated up front: The origin of the mess the industry has gotten itself into has little to do with Bitcoin or the blockchain, whose integrity has been untouched since its inception. After all, a blockchain system is built on mathematical proof, not trust. If too much of the latter meets highly speculative and partly dishonest players, the age-old ingredients of a financial crisis are given.

Grayscale Bitcoin Trust - first shadows on the horizon

But first, let's go back to the presumed beginning of the end. It is 2020 and the prices of Bitcoin & Co. are recovering from the Covid shock in analogy to other asset classes. A new post-2017 crypto bull cycle is being ushered in. This time, the investor base is already broader, but there is a vacuum of exchange-traded instruments, especially in the States, to participate in rising prices. There is only one place to go: an exchange-traded product in the form of a trust, the Grayscale Bitcoin Trust (GBTC). But the instrument has a catch: the closed-end fund is only one-way redeemable = Bitcoin can be converted into GBTC, but not vice versa. After a lock-up period of 6 months, the shares received can be sold on an exchange. So while more and more people invested, the exchange-traded product established a considerable premium in the double-digit percentage range.

An easy target for crypto investment firms that held bitcoin anyway. Through a quasi-arbitrage trade, funds could redeem their spot Bitcoin (BTC) for Grayscale Bitcoin (GBTC) 1:1, wait six months, and then collect the premium. Market participants with more risk tolerance leveraged the entire trade and deposited the GBTC shares as collateral during the waiting period to re-enter the lucrative loop with even more leverage. It also becomes clear that there were enough lenders for this kind of business; in the crypto world they are called "centralized lenders". This is because the "lending business", i.e. lending against digital collateral, was also a very lucrative business in the bull market.

However, as crypto markets became more efficient and new investment products were introduced, the initial GBTC premium steadily eroded, turning GBTC into a ticking time bomb. As crypto prices fell, the premium soon turned into a discount that weighed deeper and deeper on trading books over the months. Crypto hedge funds like 3AC were particularly affected by the reversing credit spiral and lenders were accordingly caught up in the melting collateral. Genesis Global Trading, the lender acting under Grayscale's parent company, later filed a $1.2 billion claim on the hedge fund 3AC, which was already insolvent at the time, and is now also struggling to survive.

Terra/Luna crash digs further holes in balance sheets

Misfortune rarely comes alone. A massive demand for digital assets met with an equally active and creative new creation of diverse tokens that ensured an increasing supply. One novel construct that presented itself in this environment was the algorithmic stablecoin UST - whose security was based on the seigniorage token LUNA, created out of thin air. The nature of such mechanisms only work when demand is constantly increasing. And so it came to pass as it had to. The then $60 billion construct was crushed by its own ponzinomic mechanism within days. The market value of the entire ecosystem collapsed to less than one billion - and with it the investments of the funds involved.

The fact that so many investors were involved in the Terra/Luna crypto project was due in no small part to a guaranteed return of over 20% p.a. that investors received when depositing their UST Stablecoins with the affiliated credit portal Anchor Protocol. A warning signal that was often ignored at the time. Thus, not only risk-averse venture capitalists (3AC) fell victim to the Terra construct. Centralized crypto lenders such as Celsius and BlockFi, which promised their customers double-digit returns on their deposits, were also caught with excessive Terra/Luna exposure. The first chain reaction ("Contagion") starts.

Centralized lending platforms depreciate billions

Crypto hedge fund Three Arrows Capital finally files for bankruptcy. Once the first domino falls, the crisis is unstoppable. Celsius, BlockFi, Voyager and many other well-known companies soon followed. After the implosion of the first web, the stone began to roll, and within a year nearly $100 billion of market value was wiped out. As the tide turned, it became clear who was swimming naked - as Warren Buffet would say.

FTX/Alameda - amateurish risk management turns into fraud

One of the last lifelines for the ailing credit platforms came from FTX, the second largest crypto exchange at the time. The subsidiary Alameda Research, which originally focused on quantitative trading strategies, increasingly acted as a venture capitalist over time. Countless investments were built up, loans were granted and drawn, while the CEO of both companies, Sam Bankman-Fried (SBF), signed advertising deals worth hundreds of millions.

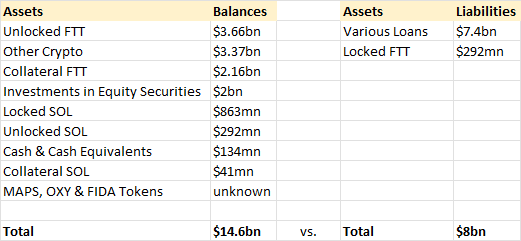

What nobody knew at the time was that there was no real separation of powers between the FTX crypto exchange and the Alameda trading house. Even worse: FTX (against its own guidelines) transferred its customers' money to Alameda's balance sheet and received illiquid, second-class FTX exchange tokens as collateral. The construct, which initially appeared financially healthy thanks to the accounting fraud, was in fact an extremely unstable entity that collapsed within 10 days of the fraud being discovered.

The repercussions of the revelations regarding the FTX scandal are penetrating deep into the industry. The actions of CEO SBF and other FTX/Alameda executives must be classified as criminal based on the latest revelations. The aftermath of the Enron case will be felt in the crypto world for a long time. In addition to the losses in the billions that customers and counterparties have to lament, the reputation of the entire sector has been massively damaged.

Free competition regulates the situation painfully but sustainably

Ironically, the Bitcoin price and thus the overall market, is suffering from exactly the situation for which it was actually created as a countermeasure. And it is precisely at this point that the industry will have to force its hand. The unconditional transparency that the blockchain guarantees must come to the fore again so that users can regain the trust they have gambled away. Mathematical proofs are more durable than trust, which has to be given to a counterparty. For this, the industry has the perfect technological tools and only these will be able to heal the damage over time. Last but not least, the fact that a blockchain-based financial system works is demonstrated by the DeFi sector, which remains unscathed regardless of all the failures.

Central crypto service providers, which operate with a fractional reserve system analogous to the banking system, must be encouraged to be transparent. Their users already inevitably demand this: never before have deposits been withdrawn so quickly when doubts about the solvency of a company arise. But the regulator is also challenged by the issues of disclosure obligations and customer protection.

Even if the loss of image cannot be explained away, the entire crypto ecosystem gains in sustainability over time in crisis situations like these. In free competition, including the absence of a central bank, only the strongest survive, while highly speculative and unfair competitors fall away. Undoubtedly, this process is playing out in a painful way for all involved.