It has been speculated for a long time, now it is here. For a few hours, a Bitcoin fund (ETF) has been trading on the New York Stock Exchange (NYSE) for the first time. This gives institutional investors easier access to the largest digital asset.

The first request for a Bitcoin exchange-traded fund (ETF) in the United States dates back to 2013 and was submitted by the Winklevoss brothers. However, the application, like the countless others that followed in the eight years since, was rejected by the relevant Securities and Exchange Commission (SEC). The reason given was the insufficient maturity of the market and the comparatively low demand for an exchange-traded product. However, much has changed in recent years. The increasing merging of the crypto industry with the traditional financial world eventually led the regulator to approve the first Bitcoin ETF in the States.

Futures-based bitcoin ETF "BITO"

The first bitcoin ETF with the exchange ticker "BITO" is a futures-based fund from U.S. issuer ProShares. The company has been present with ETFs since 2006 and currently offers a wide range of ETF products, including leveraged and inverse ETFs.

The majority of Bitcoin ETF applications rejected by the SEC so far are spot ETFs. In this case, the Bitcoins are actually held in custody at the issuer and the ETF owner has a partial claim to the deposited values with his security.

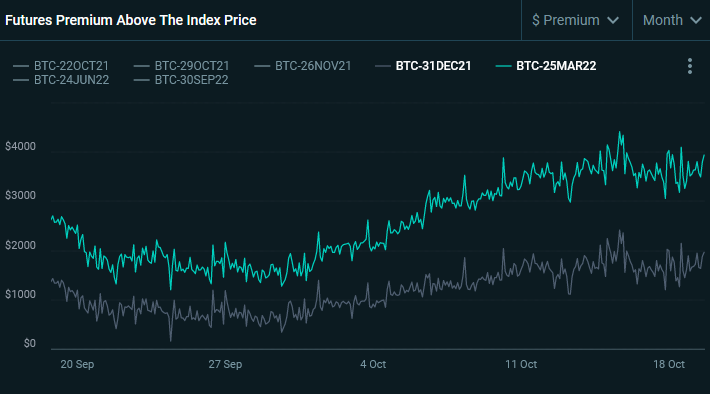

However, the Proshares Bitcoin ETF, which has been trading for a few hours, is a futures-based ETF. The price development is mapped here using forward contracts, the Bitcoin futures. Futures contracts trade at different prices than the spot market depending on their expiration date.

If the futures market trades at a higher price level than the spot market, the market is in a contango situation, in the opposite case the market trades in a so-called backwardation.

Bitcoin futures ETF not suitable for investors with a longer investment horizon

A futures-based ETF offers a number of advantages for the issuer compared to the spot ETF, as their handling is simpler in principle. For investors, however, there are certain factors to consider. If a futures contract trades predominantly in a contango situation, as is usually the case with Bitcoin, an investor fares worse over time than with a direct investment. This is because the issuer has to swap the deposited futures contracts into the next futures contract at the end of their term, paying the premium of the next futures contract, which is ultimately borne by the ETF investor.

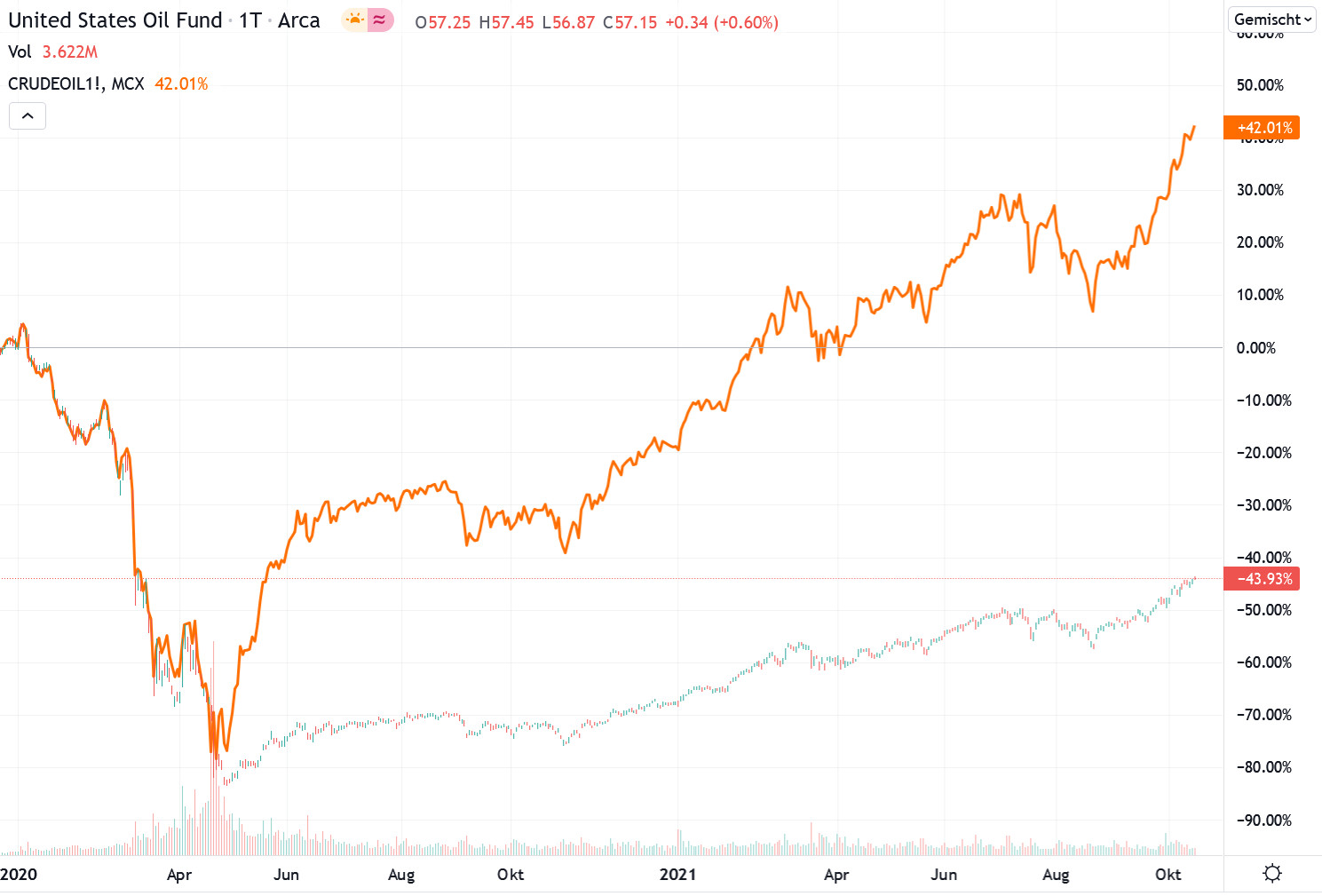

Over a longer investment horizon, this circumstance inevitably leads to a below-average performance compared to the underlying. A good example is the exchange-traded oil fund "USO" backed by oil futures contracts. Since the storage of oil turns out to be cost-intensive, the respective oil futures contracts trade at considerable premiums. Due to the expensive exchange activities involved, the investor loses money on each "rollover" due to the premium that has to be paid. In the illustrated example, this circumstance resulted in an investor losing a good 40% on the oil ETF since 2020, even though the oil price gained about 40% over the same period.

The long-awaited first US Bitcoin ETF should therefore be taken with a grain of salt. While the approval testifies to the maturity of Bitcoin as an asset class and opens up an investment opportunity for many institutional investors, for private investors, it is recommended to focus on products with direct Bitcoin investments.