A summarizing review of what has been happening at the crypto markets. A look at trending sectors, liquidity, volatility, spreads and more. The weekly report in cooperation with market data provider Kaiko.

Bitcoin closed the week within touching distance of the highly symbolic level of $100k. Meanwhile, Cboe BZX Exchange filed four Solana spot ETF proposals, SEC Chair Gary Gensler announced plans to step down in January, and a Shanghai court ruled that individual cryptocurrency ownership is not illegal in China. This week, we will explore:

- Launch of Bitcoin ETF options

- Altcoins take off

- ETH ETFs see positive inflows

ETF options are the latest bullish signal for Bitcoin

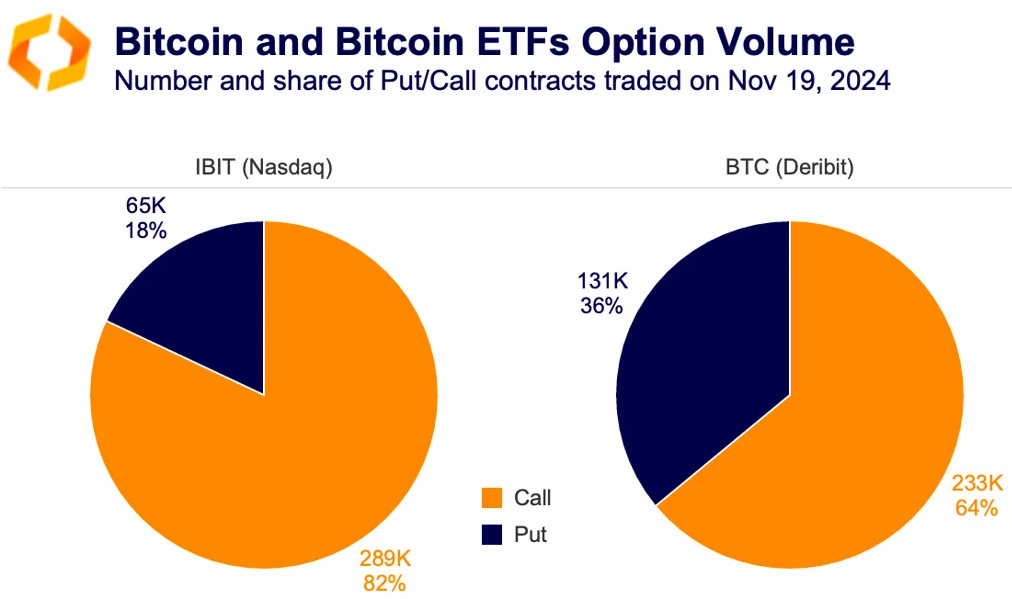

Ten months after the launch of spot Bitcoin ETFs, options on several BTC ETFs debuted last week, with BlackRock’s IBIT options reaching $1.9 billion in notional volume across 354,000 contracts on day one. For comparison, BITO options saw $360 million at launch in 2021. This strong uptake highlights robust demand for BTC-linked derivatives and bullish market sentiment.

Notably, over 80% of IBIT’s first-day options volume consisted of call options, reflecting a strong market conviction that Bitcoin prices will rise. Trading activity was heavily concentrated in near-term expiries, with December 2024 contracts dominating. The share of IBIT call options significantly exceeded that of Deribit, the largest crypto-native options market, where calls accounted for 64% of trades.

The launch of BTC spot ETF options could further accelerate institutional adoption. These instruments allow investors to hedge risks and craft sophisticated strategies to profit from Bitcoin’s volatility. While crypto-native options markets like Deribit and regulated offerings such as ProShares’ BITO futures and CME BTC futures options are already established, BTC ETF options are poised to significantly boost liquidity.

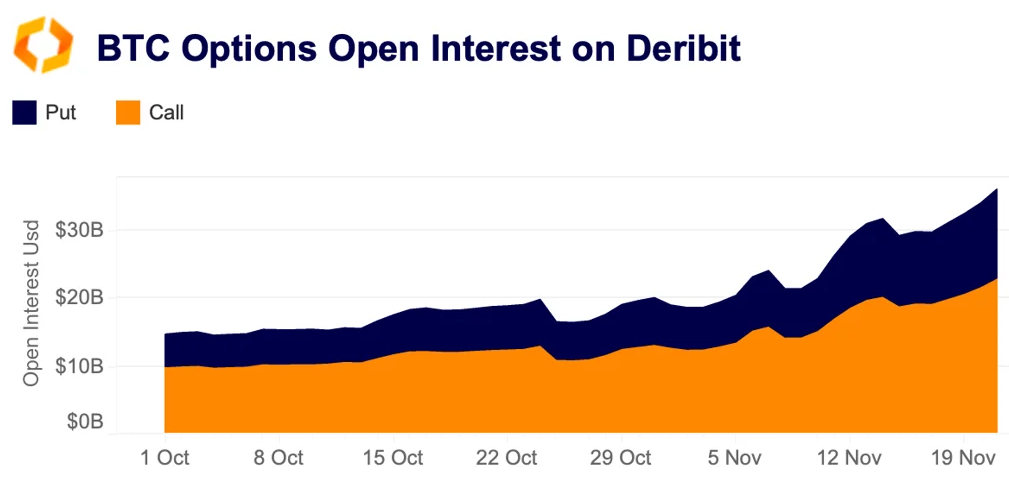

Additionally, they could drive the creation of structured products—customized investments offering specific risk-return profiles—typically developed by large financial institutions. This is likely to attract fresh capital and a new wave of sophisticated institutional traders. Finally, increased arbitrage activity by institutional players across markets could further enhance crypto-native options volumes. Deribit, already benefiting from rising institutional interest, saw Bitcoin options open interest hit a record $36 billion last week. While contract volumes remain below the 2023 peak of 320,000 (in number of contracts), they continue to climb.

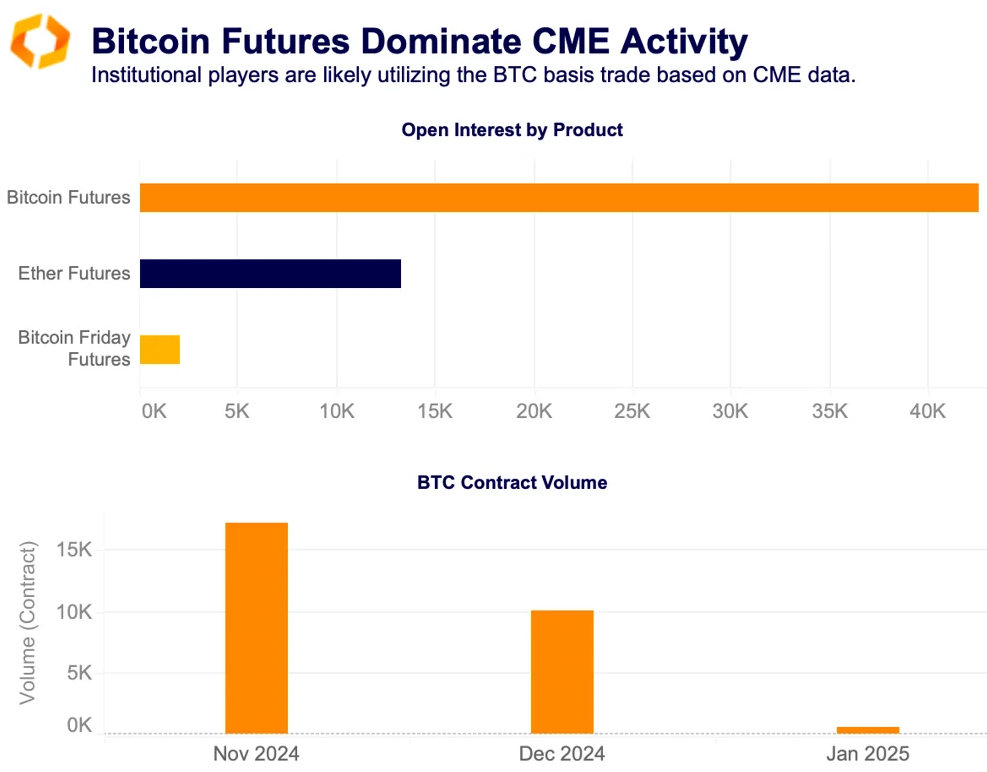

The growing institutional momentum is also evident in other regulated derivative instruments with Bitcoin futures open interest on the CME exchange hitting several back-to-back record highs over the past weeks. As we can see below the original Bitcoin Futures instrument has just over 42,000 open contracts, at 5 BTC a contract that is around $22bn in open interest at current prices on Monday.

Most of the volume over the past week has been on the November contract, known as the front month as it is nearest to expiry. The next most active is December. It's likely that trades are continuing to utilize the BTC basis trade based on this activity and we should see that December contract grow in popularity this week as traders roll their position into next month.

Breaking down the altcoin rally

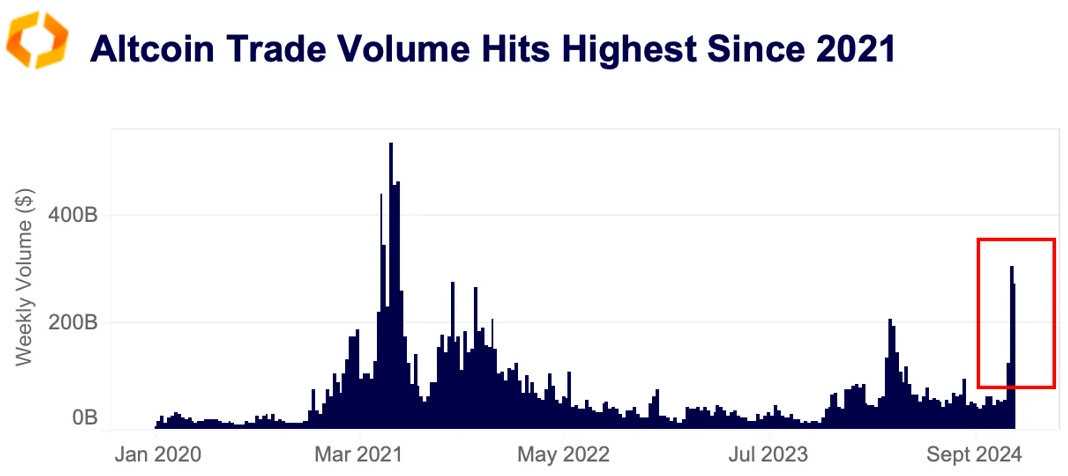

While the current market rally is still driven by Bitcoin, altcoin volumes have surged significantly since early November, signaling a growing risk-on appetite. The weekly trading volume for the top 50 altcoins by market cap reached $305 billion in early November, its highest level since October 2021. Additionally, altcoin volume dominance relative to Bitcoin (not shown in the chart) has risen to a three-year high of 74%.

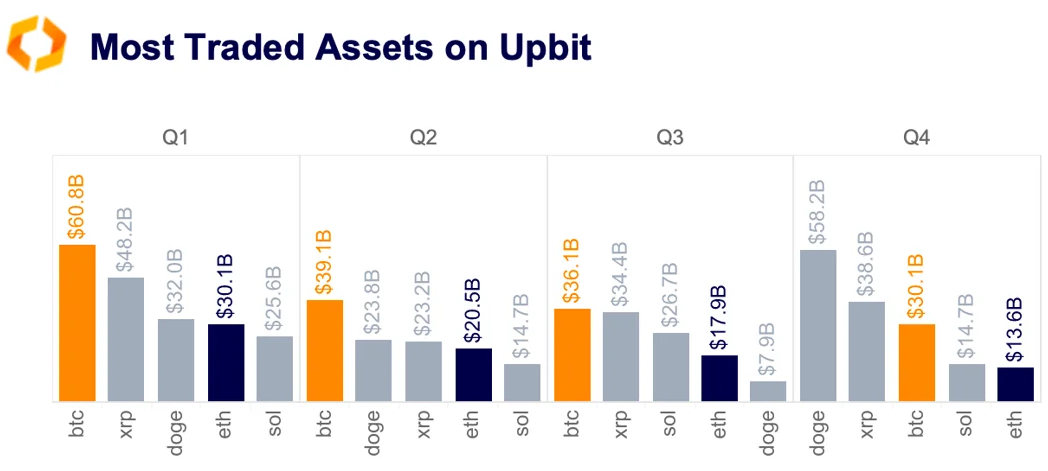

In yet another sign that altcoins are gaining momentum, DOGE and XRP surpassed Bitcoin in trading volume on Korea's largest exchange, Upbit, in November, for the first time this year. Korean exchanges, fueled by speculative retail traders, are often seen as a key indicator of risk-on sentiment in the market.

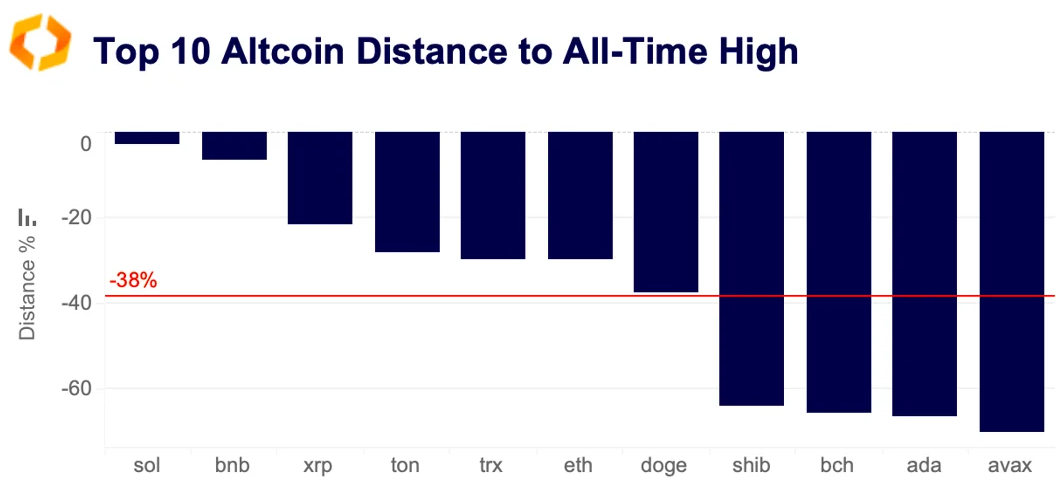

However, a closer look at the rally's drivers reveals that altcoin volumes remain heavily concentrated, with the top five tokens by volume accounting for 64% of November's total. In contrast, during the March rally, the top five contributed less than half of the monthly volume.

Most altcoins remain below their all-time highs. However, SOL stands out as an exception, hitting a new all-time high of $258 last week before slightly retreating. This surge was fueled by growing enthusiasm around ETFs, following Cboe’s re-filing of several SOL ETF applications amidst a shifting U.S. regulatory outlook.

Perhaps the largest signal of that impending regulatory shift was SEC Chair Gary Gensler's resignation. Gensler announced that he would be stepping down from the commission on January 20, the same day president Trump will be inaugurated. Under Gensler's leadership the commission has branded SOL and other altcoins as "crypto asset securities." While it is customary for the chair to step down following a regime change in the White House, he was entitled to remain on the commission until the end of his term in 2026. He will be followed out the door by Democrat Jaime Lizarraga—who is just two years into his five year term.

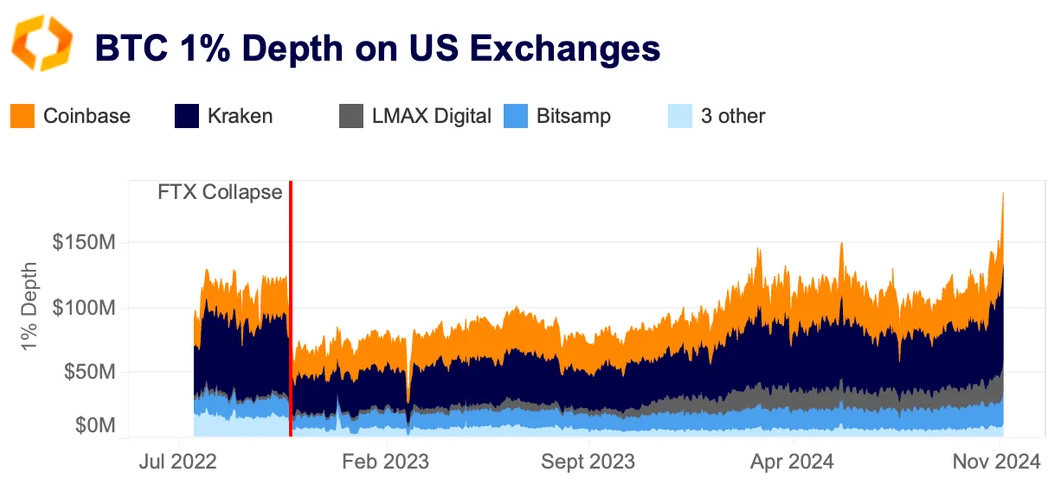

The 'Alameda Gap' is no more

The 'Alameda gap' - the gap in liquidty left after the collapse of FTX and its sister company Alameda has closed on US exchanges. Bitcoin 1% market depth is up above its pre-FTX levels of around $120mn this year driven by both risisng prices and growing market participation. Kraken, Coinbase and LMAX Digital have seen the strongest rise in liquidty. Notably Bitcoin market depth on institutional focused LMAX hit a record $24mn last week, briefly surpassing Bitstamp as the third most liquid Bitcoin market.

ETH ETFs flows turn positive

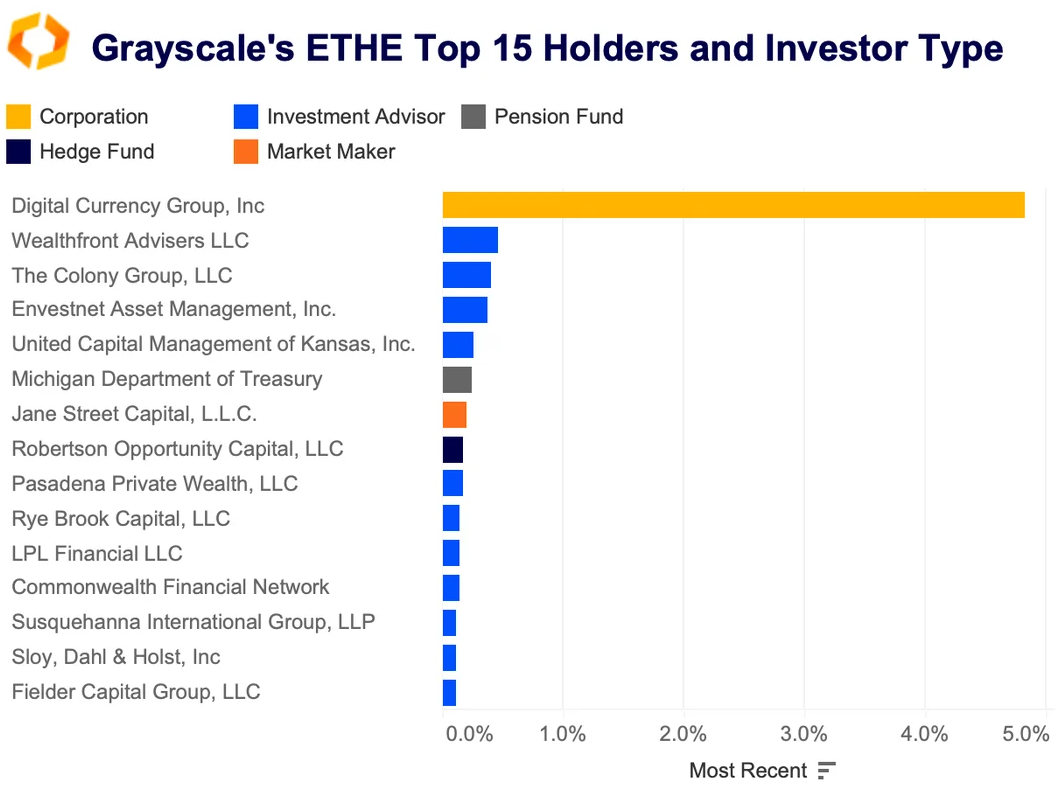

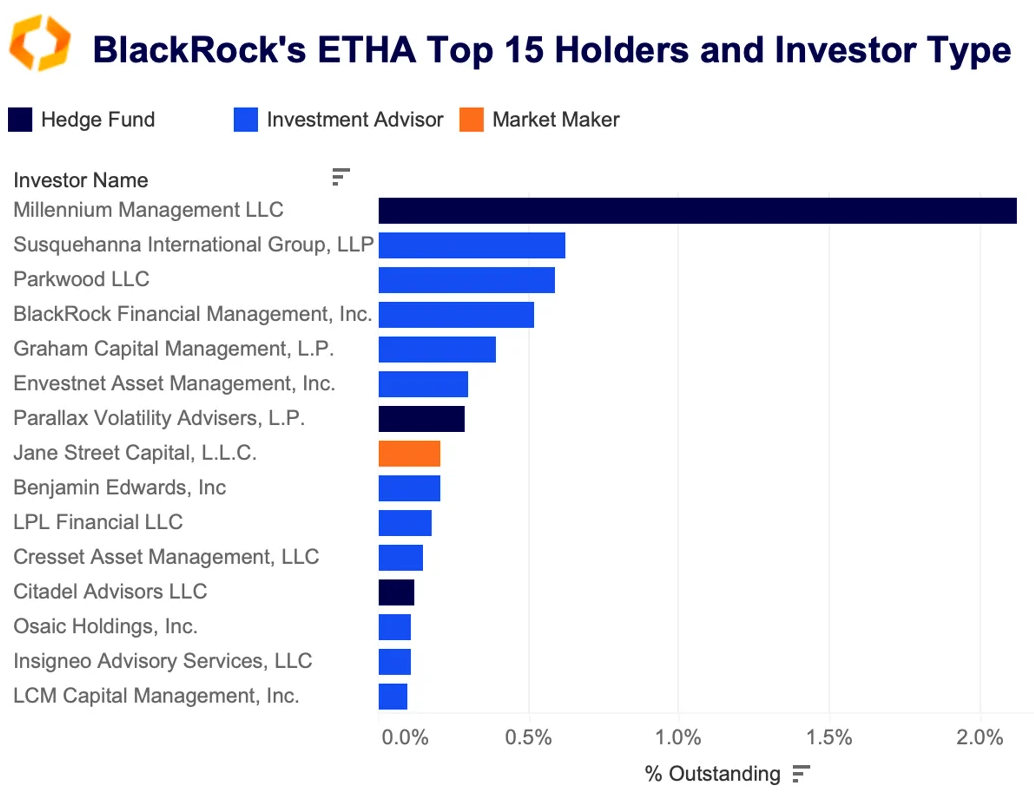

Net flows into spot ETH ETFs have turned positive this month, driven by soaring prices across the board. While ETH still lags behind BTC in terms of year-to-date gains, it briefly outperformed BTC earlier this month and is up nearly 40% since the end of October. November also marks the release of the latest 13F filings from large investment managers, which reveal holdings as of September 30, the end of the third quarter. These filings highlight some interesting trends, including the Michigan state pension fund’s holdings in Grayscale’s ETHE. The parent company of the asset manager, Digital Currency Group, remains the largest holder of ETHE.

There is an interesting contrast in the composition of the holders in Grayscale’s fund compared to those invested in BlackRock’s ETHA. BlackRock’s fund includes some of the largest names in finance, such as the $70 billion hedge fund Millennium.

This mirrors the trends we’ve seen in BTC markets, where traders are using products from established financial firms to gain exposure to BTC, such as BlackRock’s IBIT or the CME’s futures products. While ETH futures activity on the CME remains subdued for now, it could experience a similar uptick in activity as BTC markets if interest from these firms continues.

")