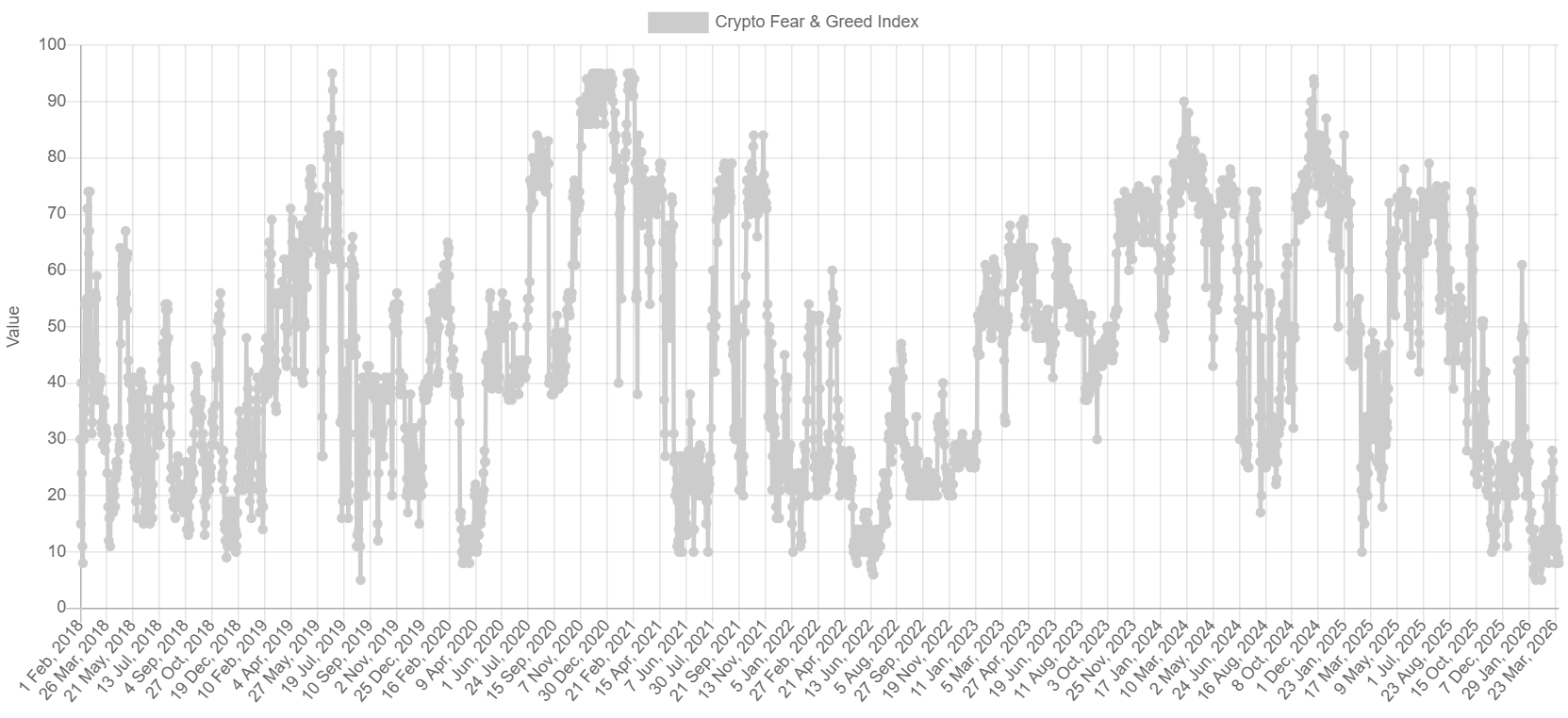

The Crypto Fear & Greed Index stands at 8 today, deep in Extreme Fear. It marks the 59th consecutive day below 25, the longest stretch of pessimism since the FTX collapse in late 2022. The low was recorded on February 6 at 5, the lowest level since tracking began in 2018.

The contrast is striking: as recently as October 5, 2025, the index was in Extreme Greed. In less than five months, market sentiment fully reversed. Since then, any recovery has been short-lived, with the current level of 10 marking the lowest reading outside the three historical capitulation phases on record.

Bitcoin Fear & Greed Index: What it measures and what it doesn’t

The Fear & Greed Index aggregates multiple inputs, including price volatility, market momentum, social media activity, Bitcoin dominance and Google Trends data. The result is a sentiment gauge, not a pricing model. A reading of 10 indicates that nearly all market participants are positioned defensively.

Ongoing liquidations reflect the pressure. On March 29, around USD 312 million in leveraged positions were liquidated within 24 hours, including USD 218 million on the long side. During the initial sell-off in early February, 24-hour liquidations exceeded USD 2.6 billion. The decline in open interest to significantly lower levels suggests that a large share of leverage has already been flushed out, historically a prerequisite for durable bottom formation.

Bitcoin spot ETFs recorded combined outflows of USD 396.8 million on March 26 and 27, marking the largest two-day outflow since early March. Unlike previous Extreme Fear episodes, selling pressure is not limited to retail but also reflects activity from institutional participants.

Historical context: three precedents, three different paths

Readings below 10 are rare. Since 2018, they have occurred in three distinct phases: March 2020 during the COVID crash, June 2022 following the Terra/Luna collapse, and the current episode. All three ultimately preceded major upside moves, with gains ranging from 150% to over 1,400% from the respective lows. The time required for recovery, however, varied significantly.

Following the COVID low in March 2020, Bitcoin rose by around 133% within six months. After the FTX collapse in November 2022, when the index stood at 12, Bitcoin traded sideways for months and only returned to USD 40,000 by the end of 2023, a 150% increase that took nearly a year to materialise. The Terra/Luna collapse in June 2022, which pushed the index down to 6, marked the beginning of a prolonged bear market. The 2018 bottom, when the index remained in extreme pessimism for weeks, was only identifiable in hindsight.

Structural differences vs previous episodes

What often gets overlooked is a key distinction from 2022. Back then, the downturn was driven by clearly identifiable catalysts, including Terra/Luna, Three Arrows Capital and FTX. The 2026 drawdown has no single trigger. Instead, it reflects a combination of macro pressure from persistently restrictive Fed policy, escalating trade tensions and a strong US dollar. According to Bloomberg, the 30-day correlation between Bitcoin and the S&P 500 rose to 0.74 in early March, the highest level of the year, indicating that Bitcoin is once again behaving like a risk asset rather than a hedge.

Bitcoin funding rates on Binance recently stood at -0.0002%, pointing to a clearly bearish derivatives positioning. At the same time, token unlocks of nearly USD 473 million are scheduled for today alone, led by HYPE, SUI, ENA, EIGEN and OP. US labour market data on April 4 could act as a near-term catalyst in either direction. With negative funding rates, any positive macro surprise could trigger significant short squeeze dynamics.

Historical data shows that since 2018, buying below an index level of 25 has resulted in positive 30-day returns in 68% of cases, with an average gain of 18.4%. In the remaining 32%, prices declined by a further 12% to 25% before a durable bottom was established.

market")