Bitcoin’s usage growth over the past decade has been strong and steady. On this journey, from its humble beginnings, Bitcoin has progressed through several phases of differing usage. To become a fast and accepted means of payment, it needs solutions such as the Lightning Network.

Starting as a worthless geeky collectible, Bitcoin soon moved to a niche instrument of speculation, before graduating to its more recent and increasing use as a store of value, or digital gold. Such progressions inches Bitcoin ever closer to the final and most valuable use case: A global and widely used new form of money.

However, widespread usage of bitcoin as money requires it to be useful as such. For bitcoin to reach its final monetary form, it is not sufficient to be a store of value alone (as is currently the case with gold), it also needs to be a viable medium of exchange. As we will see, this is a peculiar challenge for a decentralised payment system.

The design of the Bitcoin blockchain

Bitcoin was designed to reliably settle peer-to-peer transactions without reliance on any third party. To achieve this, it purposefully prioritises security and settlement finality at the expense of transaction scalability. All decentralised systems face this dilemma as there exists an inescapable tradeoff between decentralisation and scalability at the blockchain level. Take note of that last distinction as it is an important concept to grasp when investigating how scalability can still be achieved in decentralised systems using layering. We’ll return to that in a bit.

To maximise security and robustness, Bitcoin’s protocol encourages decentralisation in its network structure, meaning that no specific individual or group is distinctly relied upon to ensure network uptime. A widespread infrastructural base is incentivised by keeping the barriers to joining the network as low as possible. By minimising participation requirements (computation, storage and bandwidth) Bitcoin can be effectively operated by cheap and widely available computers, and as a result, the network is kept accessible for as many participants as possible.

Simultaneously, to optimise for reliable settlement finality, Bitcoin enforces strict and complex rules that ensure time and energy have been expended to confirm transactions. While Bitcoin’s recipe to integrate security and finality have proven fruitful in its aspirations as a peer-to-peer monetary system, it comes with tradeoffs.

Non-instant settlement transactions

Bitcoin requires its transaction record (the blockchain) to add new batches of transactions (blocks) in a process that proves the passage of time to its otherwise uncoordinated network members, and as a result, bitcoin payments are settled incrementally, not instantaneously. Per the rules, each new batch of transactions must be replicated across the entire network and each member must verify the validity of each transaction. These duties take time and energy for each participant to perform, and transactions and blocks also require time to reliably propagate across the network.

In order to minimise the incidence of stale blocks, Bitcoin is programmed to generate blocks every 10 minutes on average. This ensures that the chance of two miners finding simultaneous blocks is lowered, meaning a valid block is likely to fully propagate across the network before an alternative valid block is discovered elsewhere.

The trade-off is that it can take time for a transaction to make it into the blockchain, and once it’s in, the level of settlement finality it enjoys is determined by how many blocks deep the transaction sits in the blockchain (and the total cost of mining those blocks).

Capacity limitations

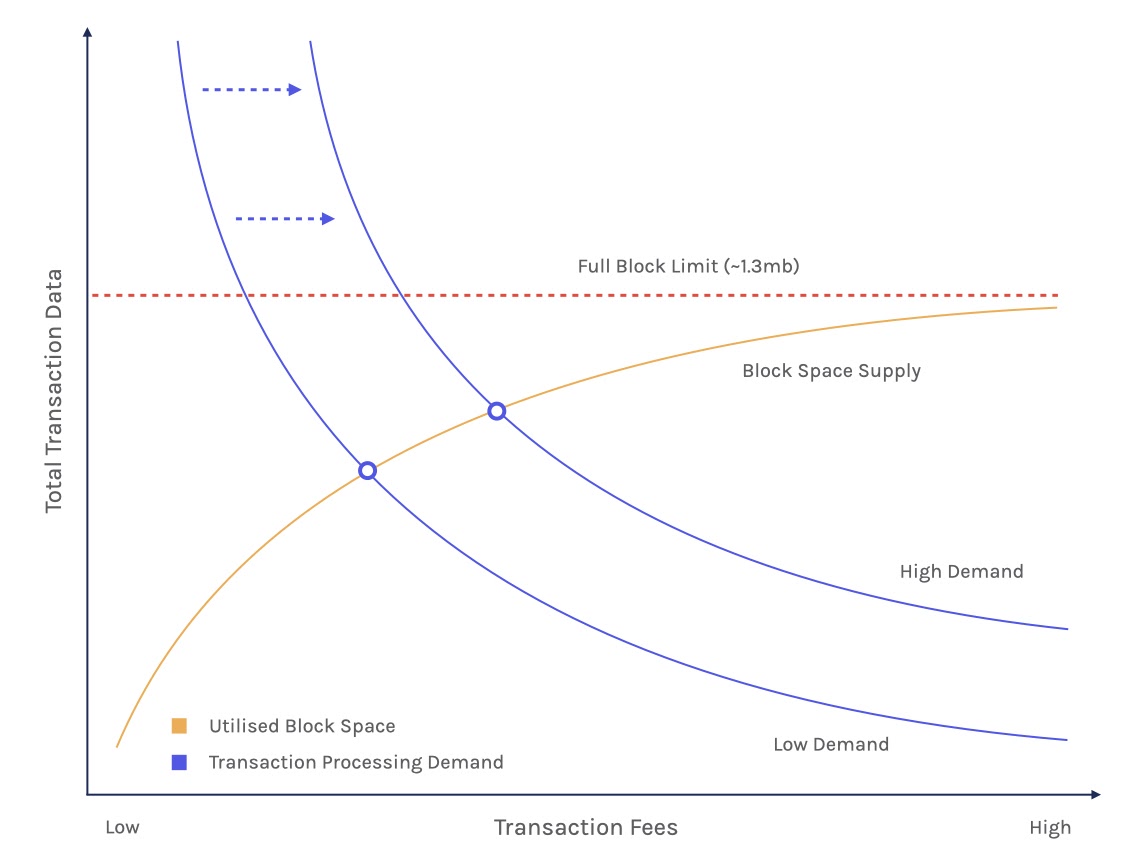

Apart from batches of transactions (blocks) being settled on a delayed schedule, they are also limited in total size (often referred to as the block size). Because these batches of transactions are replicated across the network, each participating member must sacrifice storage to maintain their own record of transactions and bandwidth to send and receive them. This is a cost node operators must bear to participate in the network, and one for which they are (unlike miners) not compensated by the protocol. Bitcoin limits these data requirements as a means to encourage participation and minimise barriers to entry.

Depending on the type of transactions the market requests for inclusion in any given block, Bitcoin’s rules require each batch (or block) of transactions to not exceed a certain data size. The actual average block size is not static, but tends to not exceed ~1.3Mb. The maximum theoretical limit is somewhat higher, but not much so. This size limit effectively increases the network’s decentralisation and security as it ensures it will remain inexpensive for users to support basic network activities.

Bitcoin’s capacity limitations together with its delayed batch processing yield a settlement speed of roughly three to seven transactions per second. This equates to around 600'000 transactions per day, which is roughly equivalent to the daily number of transactions on the FedWire settlement network. While it is probably enough for a settlement system, it is nowhere near the capacity needed for a retail payment system capable of handling small, casual transactions such as Visa or MasterCard.

High individual transaction costs

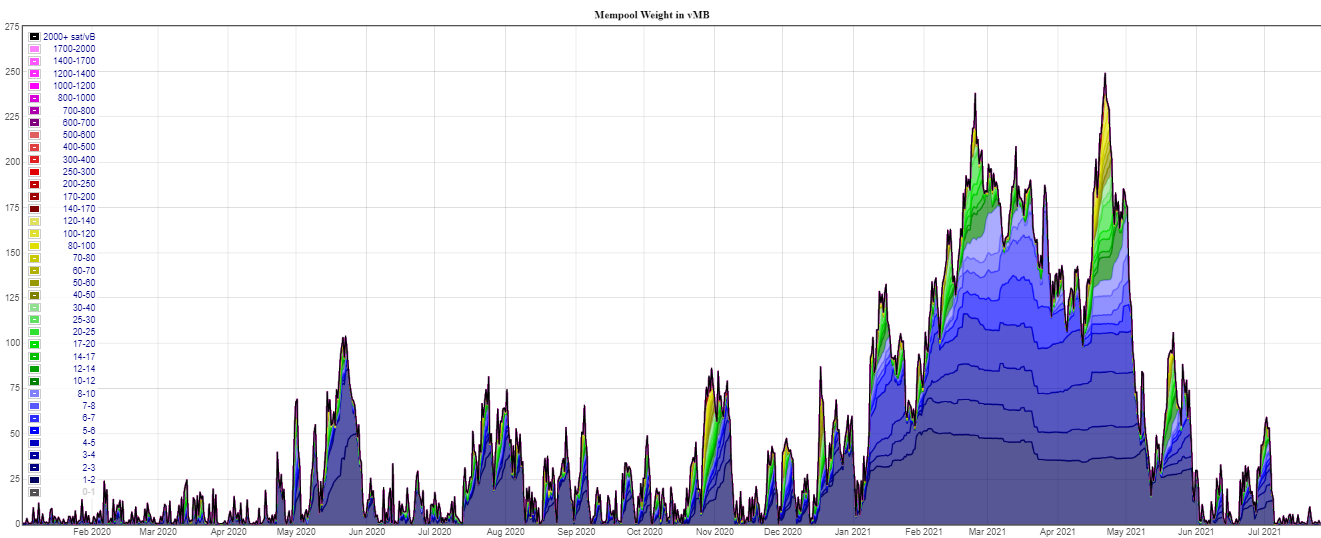

To keep track of new payments throughout the settlement process, Bitcoin offers a queue that serves as a waiting room for outstanding payments (the so-called mempool). These outstanding payments are ordered by the size of their offered fee and sit waiting until they’re added to a block by a miner. However, due to its limited speed and capacity, Bitcoin lends itself to congestion and waiting periods that unfavorably impact senders of low-value transactions (whose transactions are less able to justify competitive fees). If transaction demand gets high enough, low-paying fees may never make it into the blockchain.

Interestingly, Bitcoin transaction fees are offered on the basis of its data size, not its transaction size (value). A Bitcoin transaction sending 1'000 btc costs the same for a network participant to process as a 0.01 btc transaction. This favours transactions carrying large amounts of value. Being the same data size as a small value transaction, high value transactions can offer much higher fees per data size, while still paying a much lower percentage of the total transaction value. In a way then, the higher the value of a transaction, the cheaper it is to send.

The role of bitcoin miners

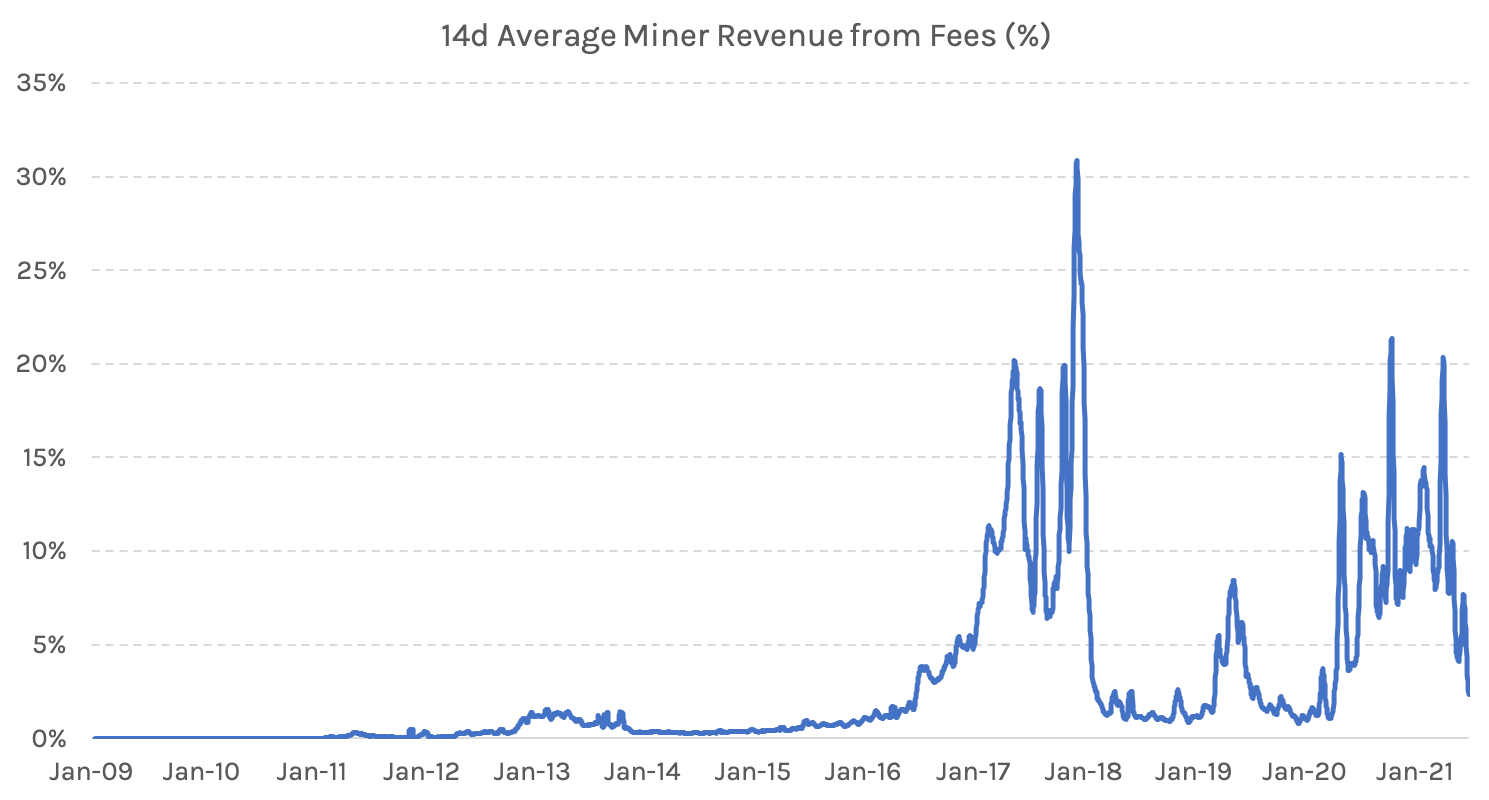

Block producing participants (miners) earn fees and subsidies (together, the block reward) for enduring the costs inherent in Bitcoin’s settlement process. The subsidies are released by the protocol as newly issued bitcoin supply, while the fees are "recycled coins" offered by users in each transaction. Importantly, each time bitcoin’s inflation rate is reduced (each halving), transaction fees become more significant as a means to incentivise Bitcoin’s settlement process.

In the early days of Bitcoin, fees were trivial as the project saw little adoption and its asset was more of an experiment than a monetary instrument. Back then, transaction demand on the Bitcoin settlement chain was low enough that blocks were rarely full and transaction fees were effectively zero.

Higher network usage

However, earlier this year, bitcoin’s market cap surpassed a trillion dollars, and its network and market infrastructure are supported by a vast industry of professionals. It has undergone three halvings and its inflation rate is approaching that of gold, meaning that the subsidy part of the block reward is getting smaller and smaller.

Increasing adoption has also induced more network activity, meaning more and more transactions are being requested by the market. This has highlighted the scarcity of transaction space available on Bitcoin, and as a result, several software upgrades and creative strategies have been adopted to combat high fees. Despite these advancements, transactions are still becoming increasingly expensive, making small casual payments on-chain, uneconomical.

The consequence of these dynamics is that Bitcoin requires layered solutions built on top of its settlement chain in order to accommodate the billions of daily transactions required for bitcoin, the asset, to take on a role as a widespread medium of exchange. Centralised payments aggregators like Visa, MasterCard, PayPal, Square etc. will likely fill a significant chunk of that role, but this is a "risk" in that these giants are competitors with clout and network effect, potentially eroding the benefits of Bitcoin’s decentralisation.

However, there are also independent alternatives out there that retain a user’s full autonomy over spending, without relying on a centralised service. One such system, that we will explore in an upcoming article, is the Lightning Network.