The FED's hawkish monetary policy has been a concern for the economy for quite some time now. Since Bitcoin has a very high correlation to regular stocks and the US dollar, high interest rates are currently also having a strong impact on the price of Bitcoin. Could we perhaps see a turnaround in interest rates in the near future?

Bitcoin prices have been hovering around the USD 20k mark for quite some time now. In this article we explore what might be the potential price catalyst from a US Dollar valuation perspective. It is clear, for now at least, that the US Federal Reserve (FED) is not about to “pivot” to a softer monetary policy stance as many had expected at the recent Jackson Hole event. This had an immediate effect on the US Dollar and interest rate sensitive assets such as equities and bitcoin. The hawkish rhetoric from the FED is likely to have a continued dampening effect on the bitcoin price outlook until their perception of macroeconomic data justifies a pivot.

Bitcoin’s relationship with the Dollar

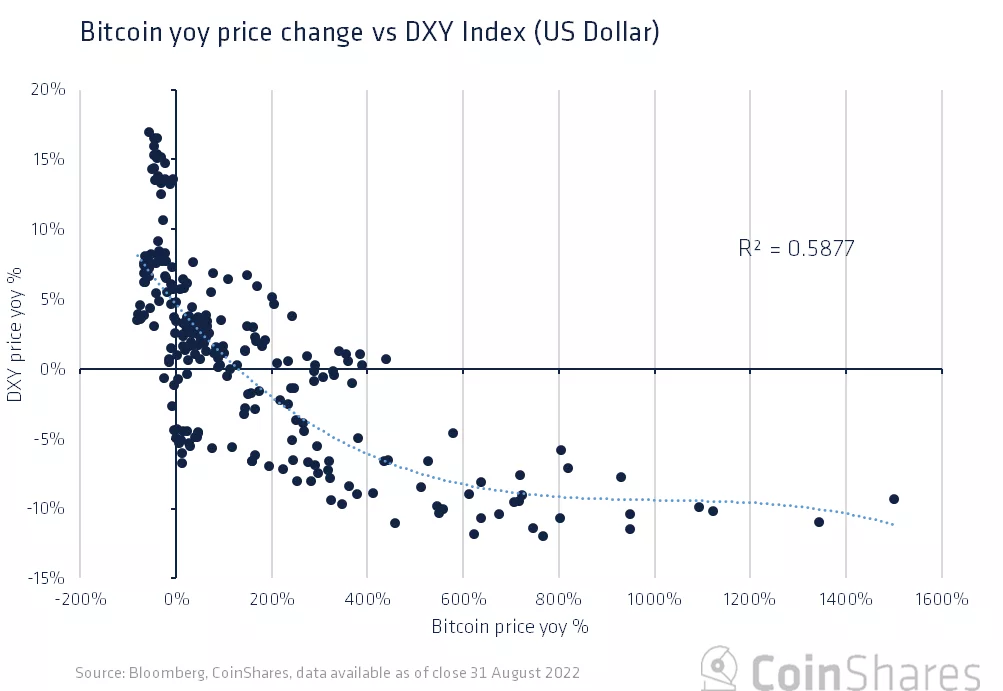

Bitcoin has a high inverse correlation to the US Dollar Index (DXY) which conceptually makes sense as it is of fixed supply and most commonly traded against the US Dollar more than any other currency. At present its correlation is approximately -70% (with an R2 of 0.5877) when looking at weekly data since the beginning of 2018. Consequently, the outlook for the DXY from a valuation and sentiment perspective, particularly after a period of hawkish comments from the FED, is crucial in determining the short-medium term outlook for bitcoin prices.

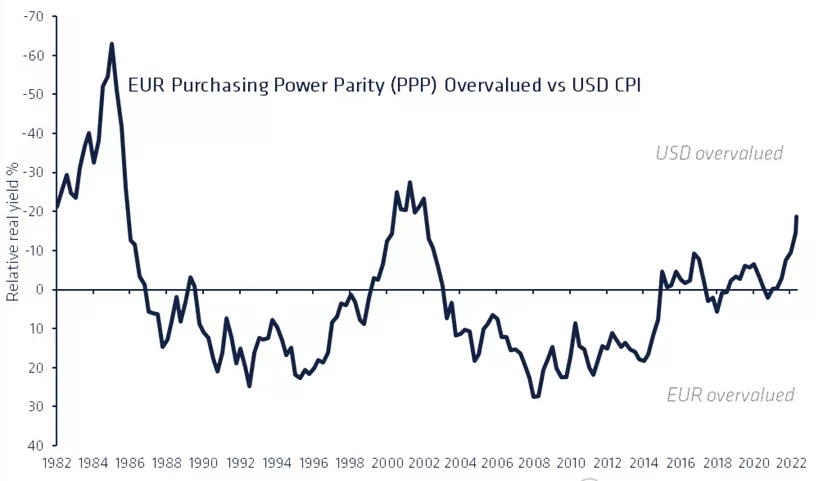

One approach to value the US Dollar is based on the notion of Purchasing Power Parity, the idea that currencies eventually equalise the cost of goods between countries. Based on this concept the US Dollar is the most expensive since 2003, although looking back further to the Volker days in the early 1980s, which is most comparable to today’s economic challenges, highlights the US Dollar could strengthen much further than it already has.

Volker managed to tame the extreme inflation of the late 1970’s and early ’80s with aggressive monetary policy, pushing the dollar to very overvalued levels. While today is similar, the US isn’t experiencing the same high levels of inflation, with indications it could have already peaked. Consequently, it is unlikely that the US Dollar will reach the highs it did in the early 1980’s.

Dollar Carry Trade

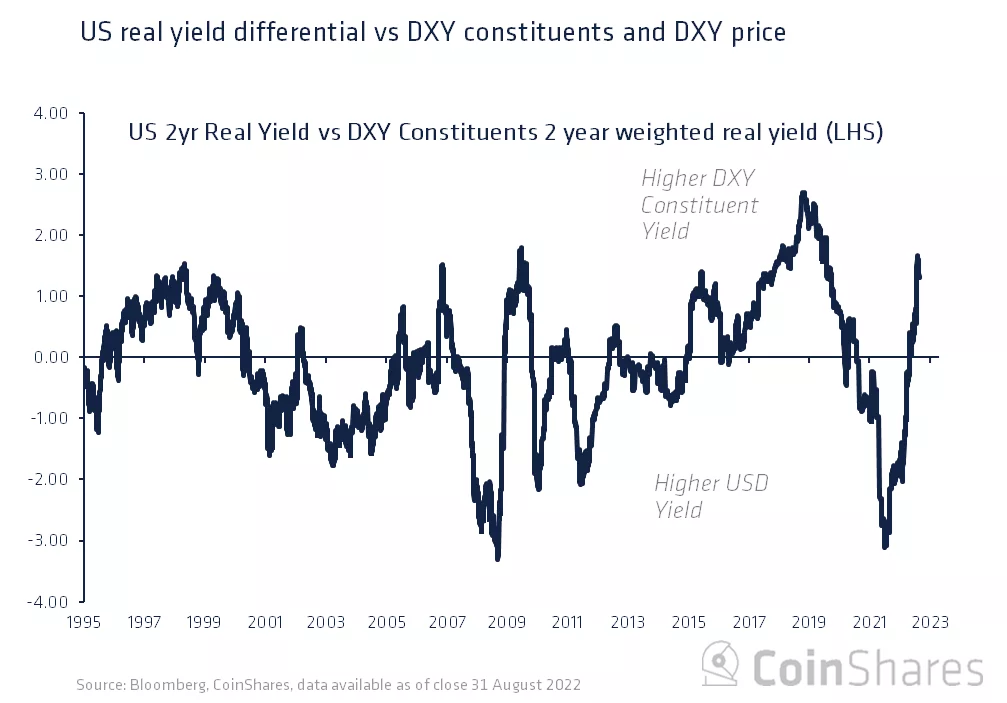

The carry trade is a trading approach that is predicated on investing in a country with higher interest rate than exists in the country where the investment is funded. In this way, demand for the designation or target currency (higher yields) rises while the demand falls for the funding currency (lower yields).

The carry trade here, between the DXY real yields and the DXY index weighted constituents real yield reveal the US Dollar is overvalued, but not at the levels seen in early 2019. In a carry trade context, the US Dollar is overvalued but could have further to run.

The CFTC futures market non-commercial positions can be used in order to determine whether investors are optimistic about the outlook for a particular currency. Since data began in 1999 investors are above the average, having been net long since August 2021.Although, as the carry trade data also highlights, investors aren’t at peak bullishness levels from a futures perspective.

When will interest rates turn?

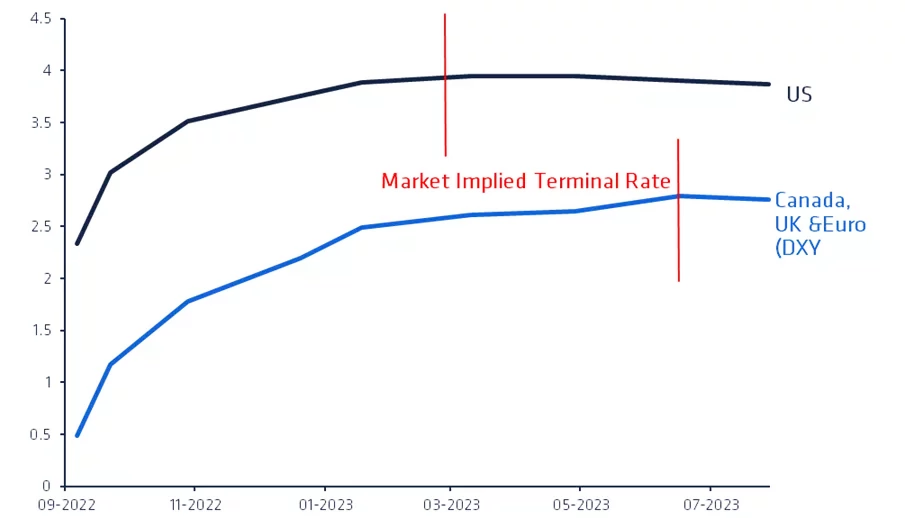

If the US Dollar isn’t at its peak levels, from an historical perspective at least, then what will prompt a near-term peak and eventual downturn? Looking at futures implied terminal interest rates curve, (the peak point of the US Federal Funds Rate) suggests interest rates are likely to peak in March 2023. This is earlier than the key trading partners of the US, which are expected to peak in July 2023.

As investors expect interest rates will peak earlier in the US, the “pivot” in monetary policy could push the DXY down before its key trading partner currencies and likely define the peak in the DXY. But the path to recession is never formulaic, with every recession having its own path to some extent. In a regular cyclical downturn and interest tightening cycle, the response to monetary policy on differing components of the economy can more or less be timed.

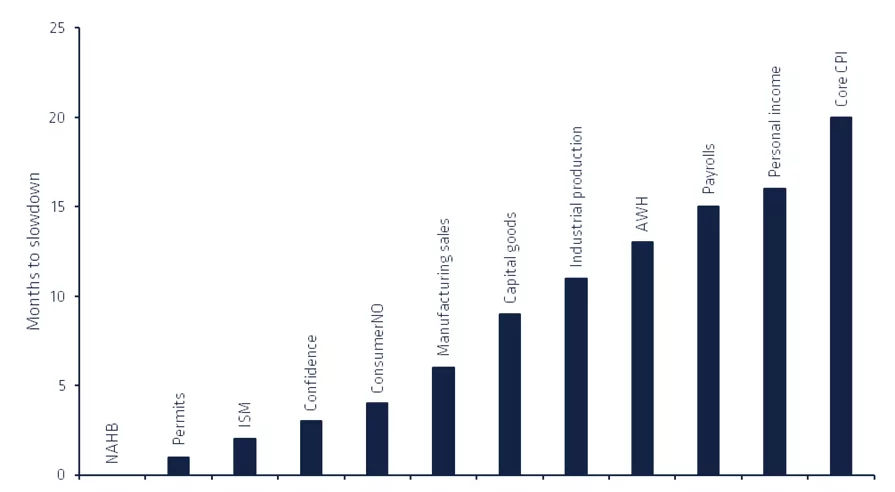

Historically, housing and corporate confidence related indicators tend to deteriorate first, while personal income and core CPI tend to be the last. History suggests that the market’s current focus on unemployment and CPI responding to monetary tightening could be leading investors into a false sense of security.

But this is anything but a regular cyclical downturn. If it were, consumption would have crashed by now, given the hit to real incomes from the surge in gas prices, and the accompanying record lows in consumer confidence. But spending rose in both Q1 and Q2 2022 and is on course to pick up in Q3. US Households still have more than $2T in excess savings, nearly 10% of GDP, so they can absorb the gas price shock without much trouble, except at the bottom end of the income scale. But the bottom 20% account for only 8% of consumption (according to Pantheon Macro), and an even smaller share of discretionary consumption.

As for housing, it will hit residential investment and all housing-related retail in due course, but that’s only 8% of GDP. Unlike the early 2000s, there has been no equity withdrawal boom, and there are no adjustable-rate mortgages to reset upwards, killing cashflow. It is therefore far from clear how this potential recession will play out.

Future outlook

We conclude that from most measures, be it valuation, carry trade or sentiment, that the DXY looks overpriced, but could appreciate further in the near-term while the prospect for a recession is far from conclusive. It looks as if the monetary policy terminal rate (according to consensus) will peak in the US before it does in its key trading partners, this coupled with the likeliness of weaker economic data in the US, suggest the DXY is likely to peak towards the end of the year. Due to bitcoin prices being highly inversely correlated to the DXY, bitcoin prices are unlikely to have a significant upside breakout this year unless we see an unexpected deterioration in macroeconomic data.