This week we analyze Worldcoin's (WLD) unique launch, featuring loans to market makers, possible wash trading, and unusual liquidity distribution.

Worldcoin’s launch was one of the most unique and controversial in recent years. Much of the controversy stems from the understandable skittishness with Worldcoin’s goal (creating a global identity network) and sci-fi-like methods of achieving this goal (eye scans). This article will focus on why this launch was unique by analyzing tokenomics, trading, and liquidity.

Worldcoin (WLD) Tokenomics

Worldcoin’s whitepaper is laid out on its website, though its tokenomics section is notably missing for those of us in the U.S. However, with the use of a VPN I was able to reveal some of its geofenced secrets, here are the most relevant details:

- The initial supply cap is 10bn WLD.

- The maximum circulating supply at launch is just 143mn WLD, 100mn of which was loaned to market makers operating outside the U.S.

- 75% of total supply is allocated to the “Worldcoin Community," 13.5% to investors, and 10% to the development team.

- Investor and development tokens are locked for 12 months after launch, then unlocked linearly over the next 24 months.

Worldcoin is unfortunately not unique in the fact that its tokenomics are fairly confusing, with distinctions between “circulating” and “unlocked” supply (unlocked is the upper bound on circulating; governance decides how quickly unlocked tokens move into circulating supply), various inflation and vesting rates, and unclear language. Put simply, the current circulating supply is 111mn WLD tokens, 100mn of which are tokens loaned to market makers. The extra 11mn have been claimed by those who took part in the pre-launch phase, verifying their identity to receive 25 WLD tokens. As more of these users claim their allocated tokens the circulating supply will increase. By this time next year, 1.6bn WLD tokens will be unlocked (unclear how many will be circulating), after which the inflation really kicks in, with unlocked supply set to hit 5bn by the end of 2025.

Just over 1% of the total supply is circulating right now, with nearly all of that loaned to market makers. Worldcoin provided more detail on these arrangements than projects have in the past, stating that five market makers collectively “received loans of 100M WLD for a time period of 3 months after token launch” after which they can return the tokens or purchase them for $2.00 + ($0.04 * X) where X is the number of tokens being purchased divided by 1mn. This dynamic, especially with five market makers involved, creates some interesting game theory. Crucially, it anchors WLD’s price around the $2 level. This, in turn, makes people more likely to scan their eyes and receive 25 tokens. So let’s now take a look at how this unique arrangement played out on- and off-chain.

Trading Worldcoin

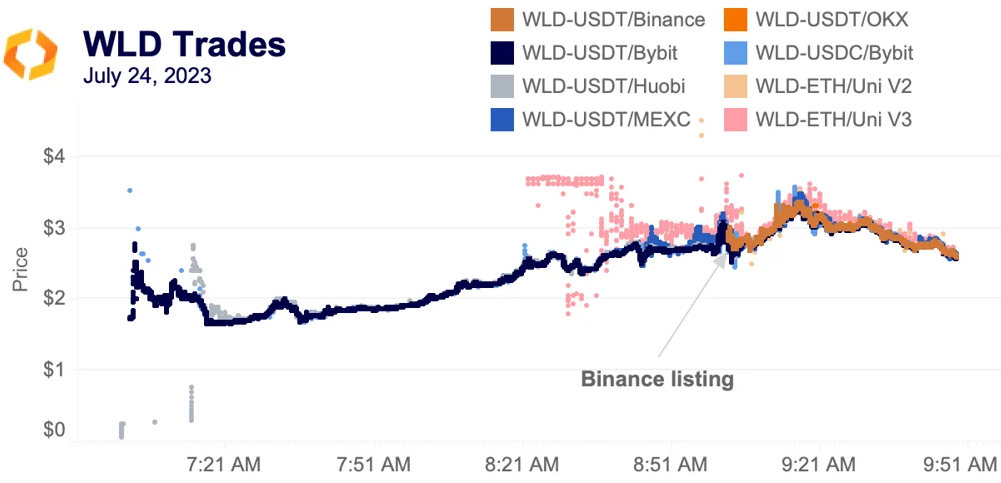

This was likely the most orderly launch ever for a token with this level of interest. Bybit and Huobi were two of the first exchanges to list the token, with Huobi seemingly false starting a few times, represented by the gray dots in the bottom left. However, once Huobi’s trading began in earnest, the two exchanges converged in about 8 minutes.

Uniswap was the next exchange to join the fray, with about 200 transactions in the $3.5 range while the price was nearly a dollar lower on centralized exchanges. Uniswap’s price began to converge over the 45 minutes as other exchanges, including MEXC, listed the token. Binance’s listing caused a spike in volatility before all prices quickly converged and began to trade in lockstep. Despite some price divergences, especially on DEXes, this was the cleanest launch in terms of price discovery in recent memory (take BLUR as an example).

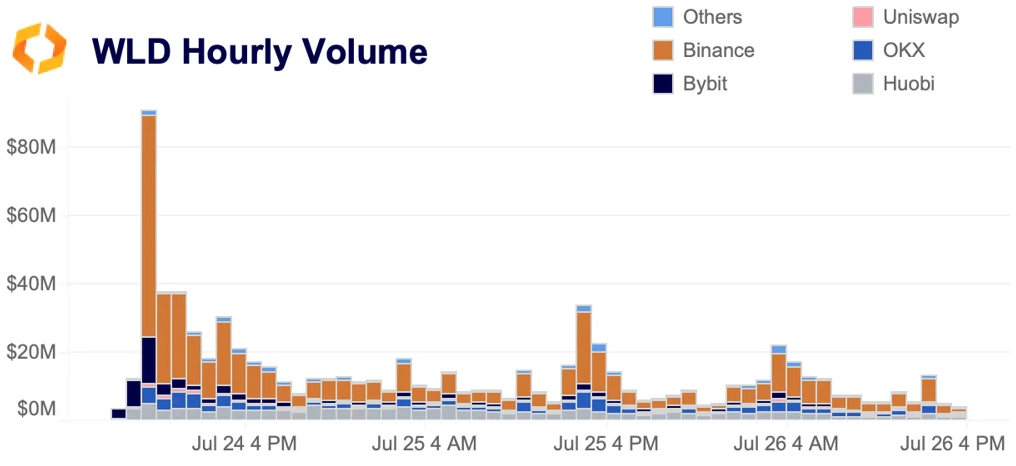

Aggregated together, it’s clear how quickly the Binance listing changed the market’s dynamics. In the first two hours, the combined volume for other exchanges was $16mn. In Binance’s first hour of listing, it did $65mn in volume, followed by Bybit at $14mn. It’s also interesting how steady Huobi’s hourly volume has been compared to other exchanges.

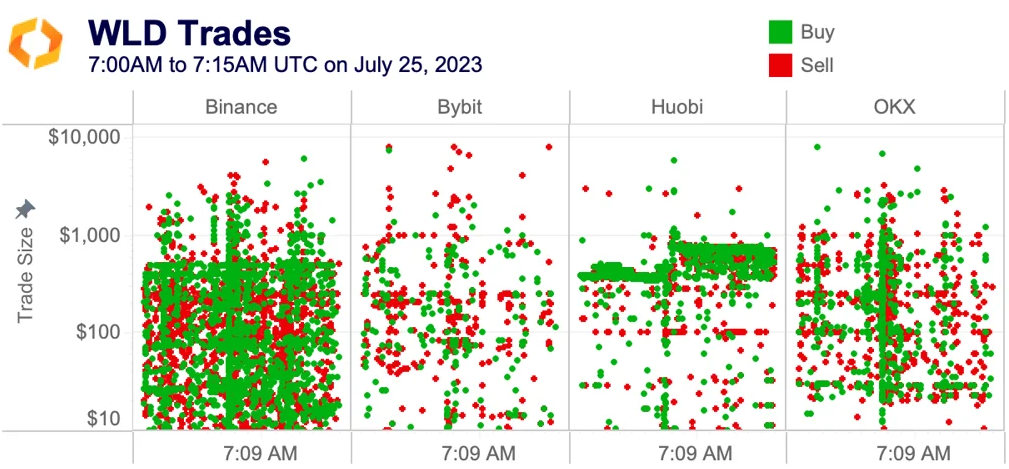

To investigate this further we can zoom in on a random 15-minute period of time on July 25. The chart below shows all trades larger than $10 on a selection of exchanges, with a logarithmic x-axis to better show smaller trades. Vertical clusters make intuitive sense: these are periods of time with higher trade volume. Horizontal clusters will generally represent TWAP trading, which is evident in Huobi’s chart.

However, when looking more closely at Huobi, these horizontal clusters are not TWAP orders; they are all perfectly balanced between buys and sells. In the past, we’ve identified that as a telltale sign of artificial volume.

The matching buys and sells add up quickly, too. The five clusters depicted above represent about $100k in trading volume in just 5 minutes, roughly equal to the sum of all the other non-cluster trades shown.

Low liquidity despite loans to market makers

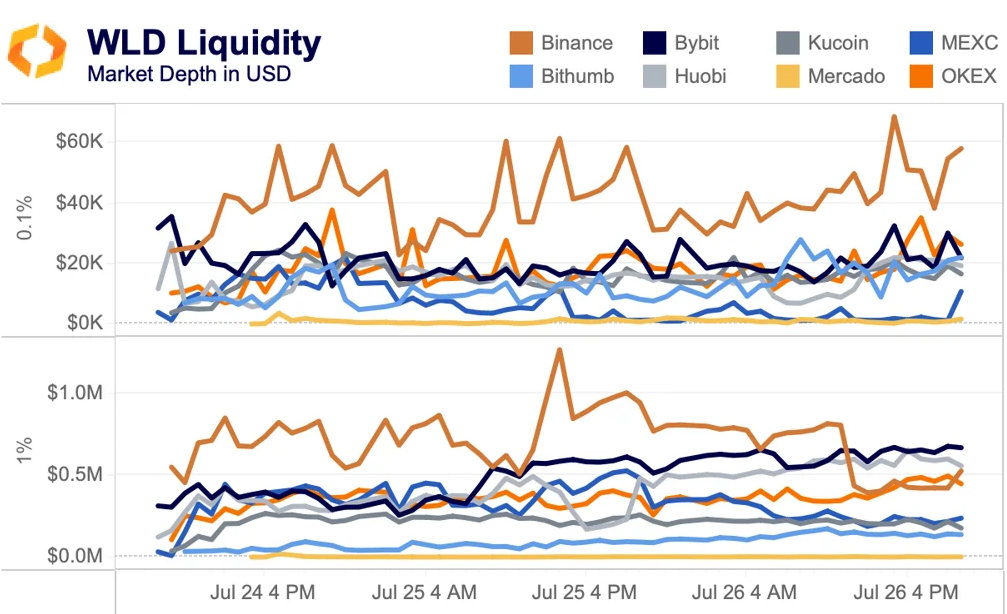

Given that five market makers were loaned nearly all of the token’s circulating supply, we’d expect the token to be quite liquid. The chart below shows both 0.1% and 1% market depth, indicating how many bids and asks are within a certain range of the mid price.

Liquidity is fairly well balanced across exchanges at both the 0.1% and 1% level. Surprisingly, Bybit is actually more liquid at the 1% level than Binance despite the latter’s significantly higher volumes. Liquidity has also been essentially flat since the token’s launch. We can compare this to two of the higher profile launches in the past year: APT and ARB.

APT’s launch was just before the FTX collapse, which caused a huge amount of liquidity to exit markets. As a result, in the first few days of trading its liquidity surged, with Binance hitting $2.75mn just a day after listing. Binance was followed by FTX, which hit $1.5mn around the same time. Just two days after listing, total APT liquidity at the 1% level broke $8mn. Unfortunately, Aptos did not provide details about any arrangements with market makers.

About five months later, ARB launched with an airdrop that caused technical issues, delaying some users from claiming their tokens. The Arbitrum Foundation also loaned 40mn ARB to market maker Wintermute. In the first week, ARB’s liquidity was concentrated on Binance, which held steady at the $2mn level. This was followed by OKX, which never broke $1mn and Coinbase which only briefly broke $500k.

Conclusion

Given that nearly all of WLD’s circulating supply was loaned to market makers, it’s somewhat surprising that liquidity is still relatively low, especially when compared to ARB, which loaned about $50mn worth of tokens at the time. WLD’s loan is worth about $220mn at current prices, yet total liquidity at the 1% level is under $3mn. Additionally, total volume has still not passed $1bn.

Taken together, the nature of the launch suggests that the team may have felt that they needed to assign an appealing dollar value to their token. Convincing people to scan their eyes for 25 units of a token that doesn’t yet exist can be challenging; if the token's price is, say, $0.10, it's even more challenging. The 25 WLD tokens are currently worth a little more than $50 and will likely stay in that range for the next three months. So far, this seems to be enticing people to sign up and scan.