The SEC has historically cited a lack of surveillance sharing and the potential for manipulation as reasons for rejecting previous spot bitcoin ETF applications. Are new surveillance sharing agreements with Coinbase enough?

BlackRock’s entrance into the spot bitcoin ETF fray brought a renewed sense of optimism that a spot ETF might be approved. This was bolstered by a D.C. court’s decision that the Securities and Exchange Commission (SEC) had not properly explained why it had accepted futures-based ETFs but rejected spot-based ETFs on market manipulation grounds, given that their prices are “99.9 percent correlated”.

The question now becomes whether the SEC will accept spot ETF applications, the most prominent of which have been updated to include surveillance sharing agreements. To help explore this question, we’ll take a granular look at BTC volumes to better understand which exchanges have the most influence on price.

Regulatory background of previous ETF decisions

In a 2022 rejection of a spot bitcoin ETF application, the SEC determined that the applicant had not properly demonstrated that it had “a comprehensive surveillance-sharing agreement with a regulated market of significant size related to the underlying or reference bitcoin assets.” It clarified these terms by stating that a significant market means that there is a “reasonable likelihood” that someone trying to manipulate the ETF would also have to trade on that significant market. In more recent ETF filings, Coinbase is listed as the significant market for surveillance sharing.

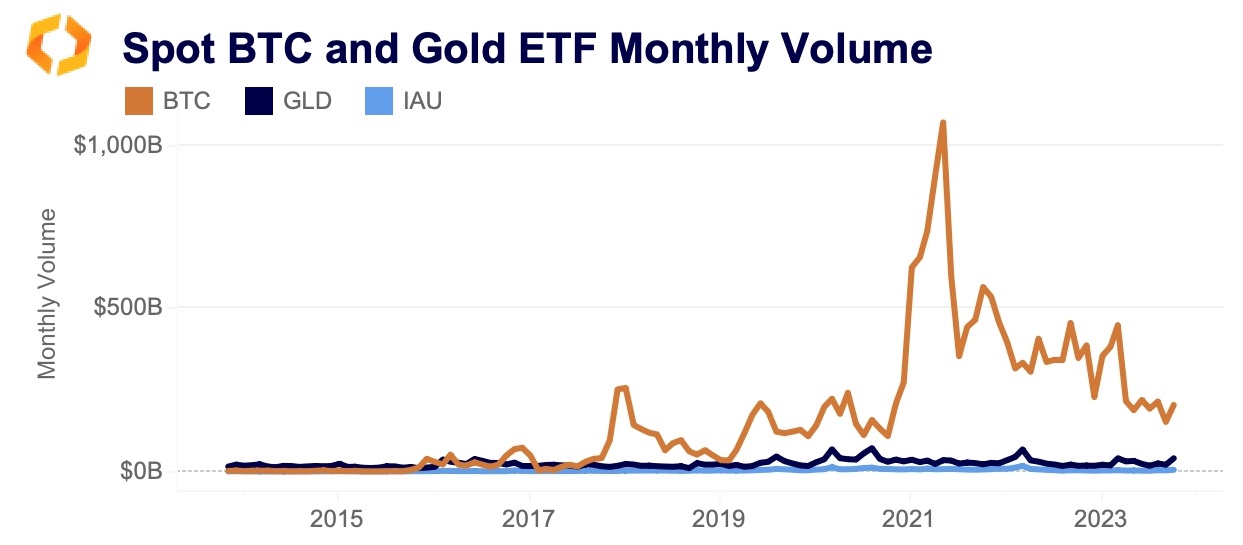

It’s worth pausing here to provide some context on volumes. Last month, there was over $200bn spot BTC volume. To use a popular comparison, GLD and IAU, the two largest gold ETFs, registered under $50bn total.

Even if hypothetical spot bitcoin ETFs generated, say, $50bn in monthly volumes, cannibalizing some from primarily U.S. exchanges, the spot market would still be significantly more active. To manipulate the ETF would require an entity to manipulate the much larger spot market on a variety of exchanges headquartered in different countries. When considering futures markets, this prospect is even more challenging.

While BlackRock’s initial application did not include direct reference to a spot surveillance sharing agreement, an update in June explicitly named Coinbase as a spot market surveillance partner and noted that Nasdaq is a member of the Intermarket Surveillance Group, along with CME, whose surveillance of its own bitcoin futures has been deemed acceptable by the SEC in the past. But are these agreements enough?

Bitcoin volumes: then and now

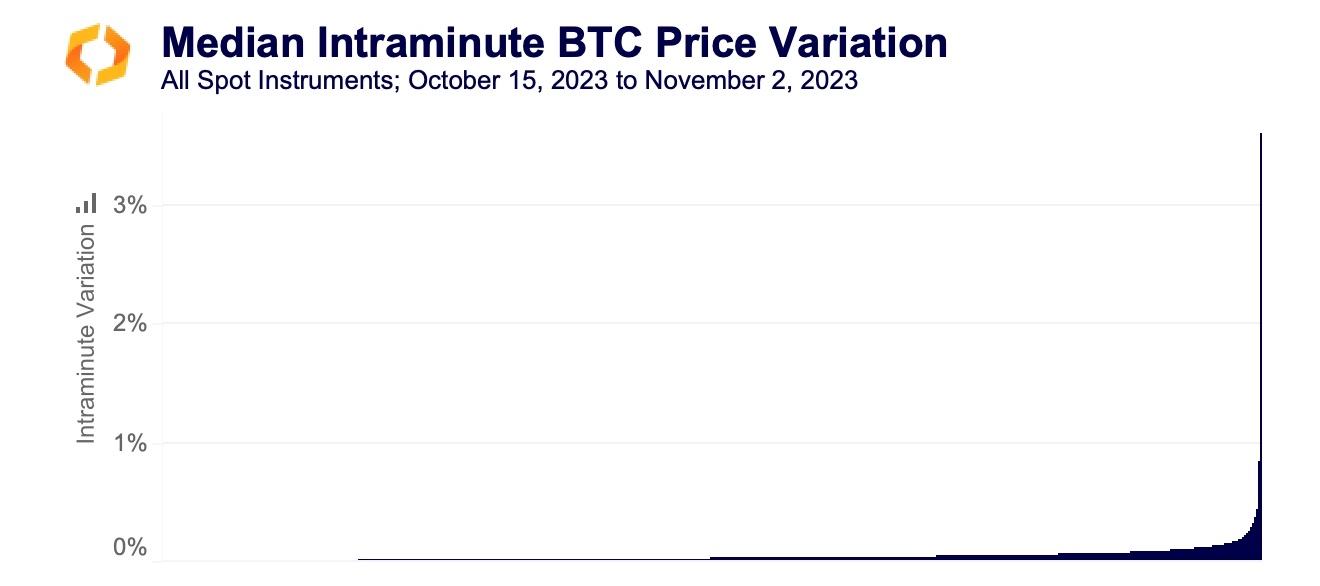

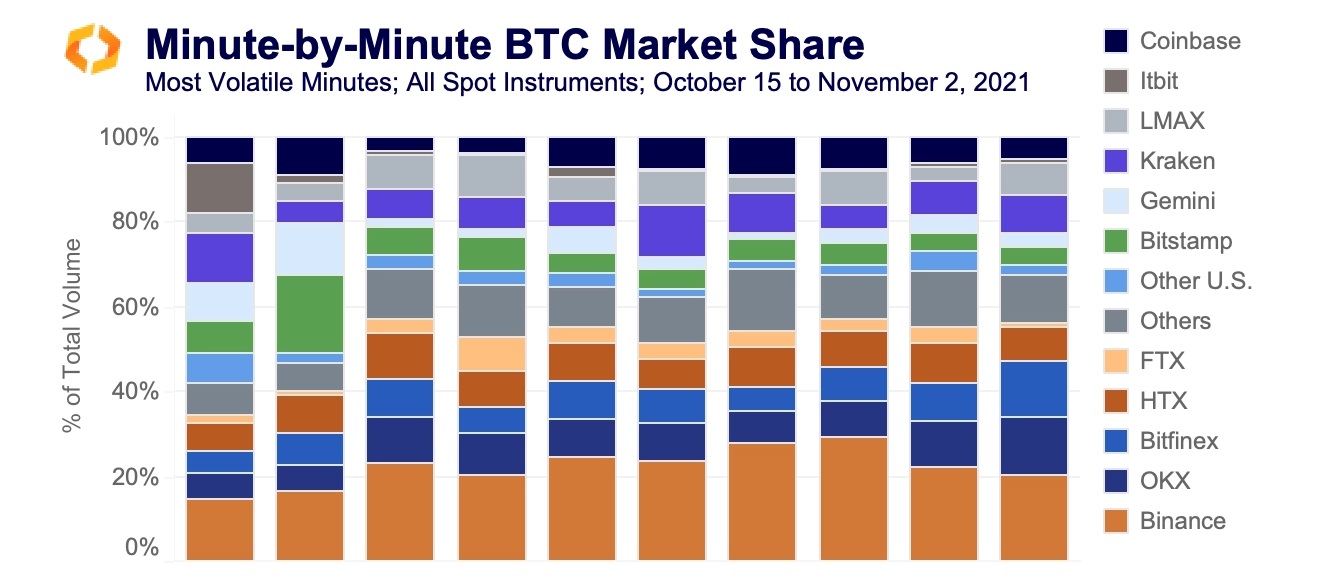

When it comes to BTC, not every minute, hour, or day is created the same. The chart below shows each minute between October 15, 2023 and November 2, 2023. The y-axis shows the median percentage price difference between High and Low at each minute. For example, if Coinbase BTC-USD swung 1%, Kraken BTC-GBP swung 2%, and Binance BTC-BUSD swung 3%, the chart shows 2%.

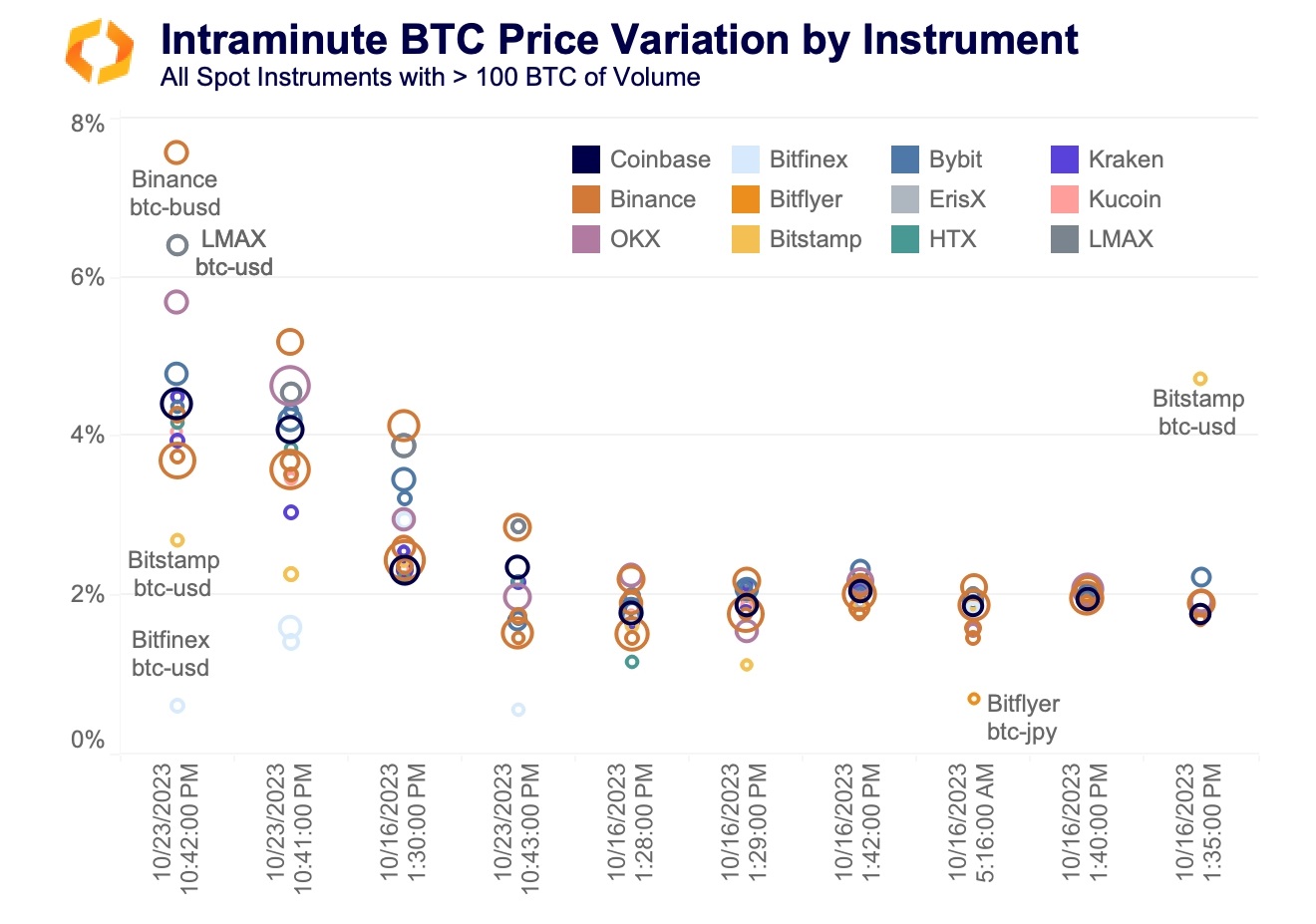

Of the nearly 30,000 minutes in this timeframe, only 15 registered a median price swing of more than 1%. The largest median price swing was 3.6% on October 23 at 10:42 pm UTC. The chart below zooms in on the higher volume instruments during the 10 most volatile minutes in this timeframe.

Intraminute price variations are largely clustered except for the four most volatile minutes. In the most volatile minute, Bitstamp and Bitfinex’s BTC-USD instruments swung the least, Binance’s BTC-BUSD the most, followed by LMAX’s BTC-USD. By far the highest volume instrument in this minute was Binance BTC-USDT at 1.5k BTC traded, followed by Coinbase at 1.1k BTC. In the next most volatile minute, OKX and Binance BTC-USDT are virtually tied at 1.9k BTC, followed again by Coinbase at 900 BTC.

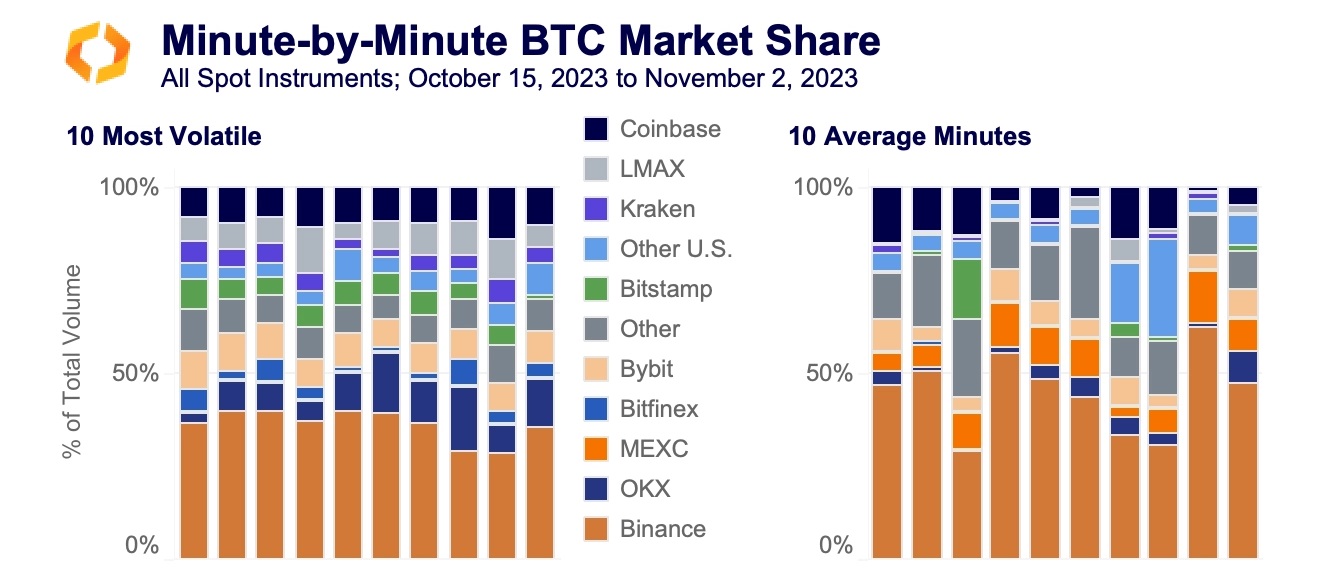

These most volatile minutes have volume profiles that are distinct from the average minute. Surprisingly, the breakdown of volumes is actually fairly consistent when volatility is highest. The chart on the left shows volume share by exchange for the 10 most volatile minutes in the same time period as above. Coinbase regularly captures about 10%, LMAX 7%, Kraken 5%, Bitstamp 5%, Bybit 10%, and Binance about 35%.

In average minutes, Binance often captures more than 50% share (in large part driven by its no-fee BTC-FDUSD instrument), while MEXC, which also has no fees and whose share is too small to see on the left, captures between 5% and 15%. Kraken, LMAX, and Bitstamp all have significantly smaller shares on the right. Meanwhile, Coinbase varies between 1% and 15%. Finally, we can compare this to the same time period in 2021 to see how things have changed since the SEC’s last batch of rejections.

Besides the most volatile two minutes on the left, Coinbase, Itbit, LMAX, Kraken, Gemini, and Bitstamp, the exchanges on which BlackRock’s ETF pricing would be based, accounted for around 30% of volumes. This is roughly the same as now, the main difference being that Binance has absorbed market share from FTX, HTX, and other off-shore exchanges, while much of Itbit and Gemini’s share has been taken by other U.S. exchanges. Coinbase’s market share was smaller and less consistent than it is today.

Bitcoin spot ETF on the horizon?

So, is the surveillance sharing agreement with Coinbase enough? Since 2021, the exchange has grown its market share during the most volatile minutes and consistently has the 2nd or 3rd highest volumes when prices are swinging the most. Put simply, it’s hard to imagine a scenario in which an entity could manipulate an ETF’s price over a short time frame without also attempting to manipulate the price on Coinbase, meaning it should fit the definition of “significant market”. Should this not be enough, a self-regulatory organization like the Intermarket Surveillance Group – in this case composed of top crypto exchanges – would further bolster the anti-manipulation case and likely serve as a net positive to the industry in the long run.