Pick up a crypto card in Zurich and a Swiss thing happens that almost never happens anywhere else: there is a real chance the company whose name is on the card also holds the licence that issues it.

Fiat24 runs on a FINMA fintech-bank licence held by SR Saphirstein AG (the same entity now also behind Mantle's UR neobank card). Swissquote, a fully licensed Swiss bank, issues its own debit Mastercard that spends from fiat or any of 52 cryptocurrencies. In both cases the brand on the front and the licence in the background are the same company. You know exactly who stands behind your money.

That is the exception. For most crypto cards on the market, the brand and the licence are two different companies, and the cardholder is rarely told which is which. After mapping the issuing layer behind the 141 crypto cards I track, I think that gap is a risk almost nobody prices in, and Switzerland is a useful place to explain why.

The four layers, and the one you see

To put a card on the Visa or Mastercard network you need to be a principal member, which means a banking or e-money licence, regulatory capital, and a compliance function. Most crypto companies have none of that. So they rent it. The arrangement is called BIN sponsorship: a licensed bank or e-money institution lends its Bank Identification Number, and the crypto company builds the brand, the app, and the support on top.

Four layers end up stacked behind a single piece of plastic: the network, the licensed sponsor, the program manager that wires it together, and the consumer brand. Only the last one is printed on the card. A US self-custody card might say nothing more than its own name, while the entity that can actually switch it off is a state-chartered bank in Tennessee you have never heard of. The Swiss self-issuers collapse those four layers back into one. Everyone else keeps them apart, and keeps the cardholder on the outside.

None of this makes BIN sponsorship a racket. Renting a licence is why most crypto cards exist at all: it lets a wallet ship a card without spending years and millions to become a bank. The Swiss route is the opposite trade, a FINMA licence that is slow and costly.

Poland, January 2026

Here is what the gap looks like when it breaks. On 21 January 2026 Poland's financial regulator, the KNF, withdrew the payment-institution authorisation of a small company called Quicko, citing unstable management and ties to a platform that had let Russian users buy crypto in breach of EU sanctions. Quicko was not a brand anyone held in their wallet. It was the licensed issuer behind several crypto cards, and once its licence was gone, so was its ability to issue. CEX.IO told its users that card payments would stop on 3 February. The CEX.IO brand had done nothing wrong. The thing that made its card work had simply disappeared.

Not every brand on Quicko's rails died. Some had, or quickly found, a different sponsor and kept going; Mercuryo's spend card, for instance, runs today on a separate UK e-money institution. When your card lives or dies by a licence you did not choose and were never shown, your fate depends on whether the company behind the brand kept a second issuer in reserve. Most cardholders have no way of knowing whether it did.

The market looks fine until you split it

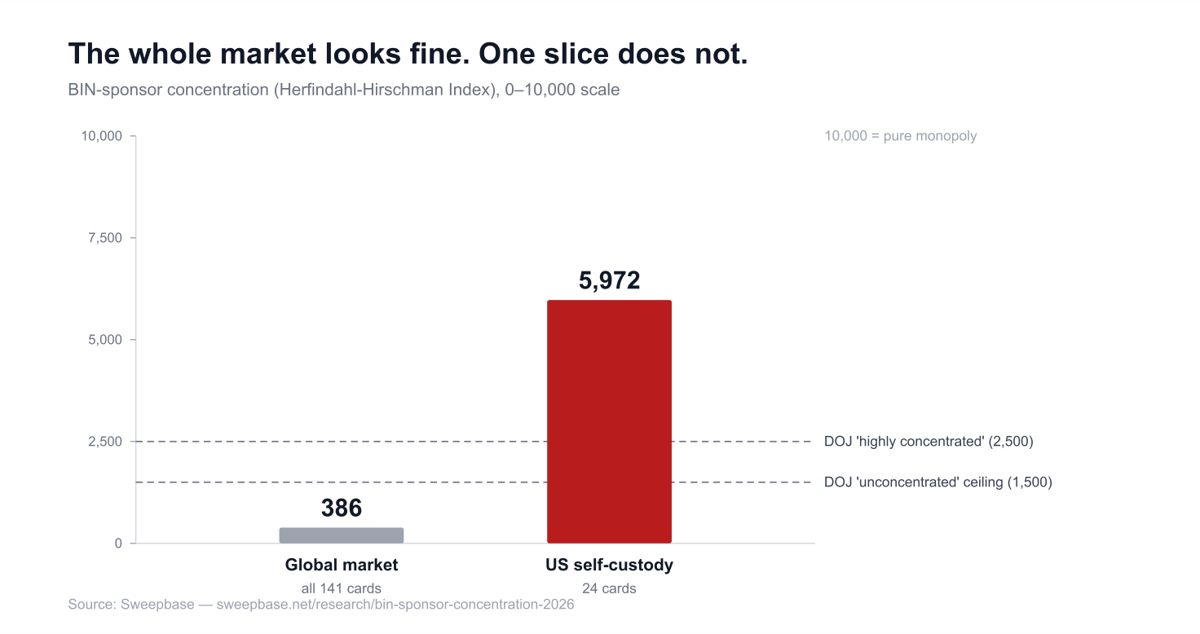

Measure concentration across all 141 cards at once and nothing looks wrong. Using the Herfindahl-Hirschman Index, the standard concentration measure, the whole market scores around 390, comfortably inside the US Department of Justice's "unconcentrated" zone (anything below 1,500). By that number the crypto-card market is healthy and competitive.

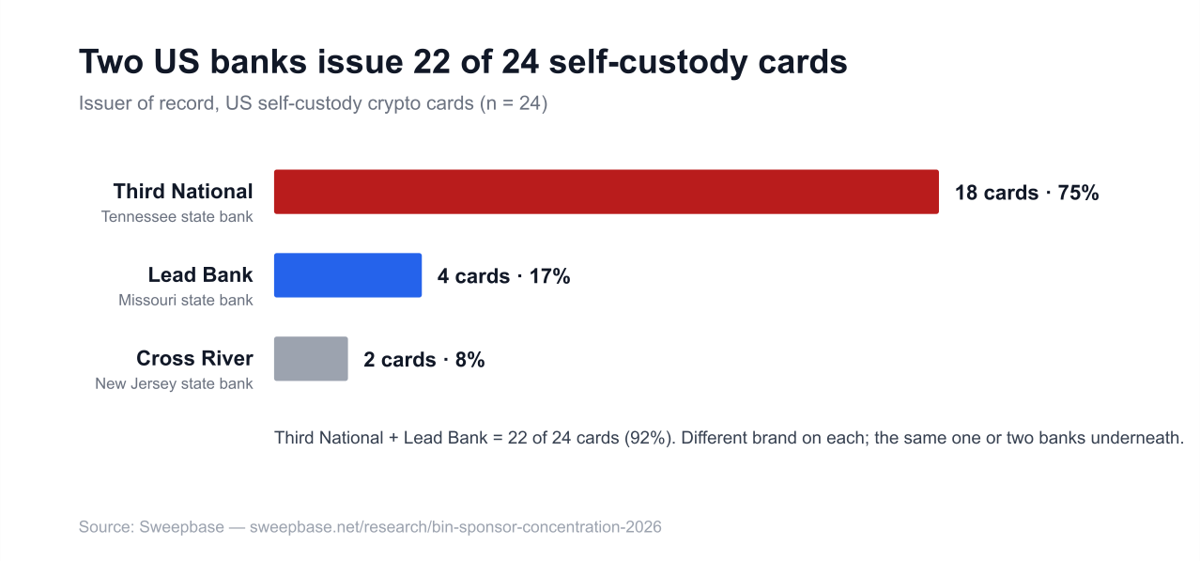

The number is misleading, because a dollar self-custody card issued in Tennessee does not compete with a Swiss franc account issued in Zurich. Split the data into the markets a user actually chooses between and it changes hard. Among US self-custody cards, two banks do almost all the issuing: Third National in Tennessee issues 18 of the 24 cards I track (75 percent), and Lead Bank in Missouri four more, so the two of them cover 22 of 24, around 92 percent. That segment's HHI is close to 6,000. A market shared evenly by four firms scores 2,500, which is already the line where US regulators call concentration high; this one sits closer to two firms splitting almost everything. Unlike the European reading below, the figure barely moves however you draw the segment, because both banks are named outright in the cards' own terms (Solayer's name Third National, Phantom's name Lead Bank). Different brand on every card, same one or two banks underneath.

Europe tells a quieter version of the same story. No single sponsor is quite as dominant across all of EU and UK self-custody, and anyone who quotes you one tidy concentration figure for it is probably drawing the segment to fit the number. But one name keeps recurring: Monavate, the e-money institution behind Gnosis Pay, 1inch, and the European side of cards like Ledger and MetaMask. In 2026 that node got absorbed. Exodus, a self-custody wallet, had agreed in November 2025 to buy Monavate's parent. The deal restructured, and on 1 May 2026 Exodus closed it through UK-appointed receivers after the parent defaulted on a loan that Exodus itself held. Rather than pay cash, Exodus bid that debt, taking the Monavate and Baanx shares for the $76 million still owed, plus up to $30 million more for the US arm. That is about $106 million in all, against the $175 million agreed in November. One wallet company now owns the issuing infrastructure behind several of its competitors. Owning your own rails is ordinary vertical integration; owning your rivals' rails is the part worth watching. There is no sign yet that Exodus has used the position against anyone, and almost nobody has remarked on it.

Why the Swiss model reads differently

Set the Swiss self-issuers against that backdrop and the contrast is the point. When Fiat24 or Swissquote issues your card, there is no rented licence to lose: a problem becomes a Swiss bank or fintech-bank matter handled by FINMA, not a cascade triggered by a foreign regulator pulling a sponsor you never knew existed.

How much of this actually touches Switzerland? Of the cards I track, only a handful carry any Swiss nexus, and just seven are issued under Swiss supervision: SR Saphirstein's six and Swissquote's own. The rest a Swiss resident can reach are issued somewhere else, and that distinction matters, because a Swiss licence is a different instrument from the EU one most crypto cards rent. A FINMA fintech-bank licence under Article 1b answers to the Swiss regulator directly, rather than being passported in from an e-money institution in Vilnius or Paris. For a cardholder that changes who answers when something breaks.

This is not a claim that Swiss cards are automatically safer on every axis. Concentration shows up in Switzerland too: SR Saphirstein's single licence sits behind six different card programs, so a problem there would touch all of them at once. The protection is not uniform either. Swissquote is a full bank, so balances sit under Swiss deposit insurance up to CHF 100,000. SR Saphirstein holds the lighter Article 1b fintech-bank licence, which caps deposits at CHF 100 million, pays no interest, and carries no deposit insurance at all; the law makes it tell customers their balances are not protected. What Switzerland gives you is narrower than a guarantee: you can find the entity and see which rulebook it sits under. A Swiss address does not even promise that much. The SwissBorg card, launched this year, still does not publicly name the bank or e-money institution that issues it, and SwissBorg's own MiCA registration is a crypto-asset licence, not a card-issuing one.

What a cardholder can actually do

The takeaway is not alarm, it is plumbing. Before you load real money onto a crypto card, find out which licensed entity issues it and which regulator would step in if that entity failed. The better cardholder agreements tell you in the first few paragraphs; the ones that never name an issuer at all are telling you something by omission. Treat the card as a way to spend, not a place to store value, and if serious money runs through your cards each month, do not route all of it through a single sponsor. The people who barely noticed when Quicko's licence vanished were already carrying a second card on a different rail.

Switzerland does not have this figured out perfectly. But its handful of self-issuing card programs show the cleanest version of the fix, slow and costly as it is: let the company you can see be the company that holds the licence. The full dataset behind this piece, with the issuer, regulator, and source document for each of the 141 cards, is open at sweepbase.net/research/bin-sponsor-concentration-2026.