Fidelity Investments is entering the stablecoin market. The company announced the Fidelity Digital Dollar (FIDD), a US dollar-pegged stablecoin running on the Ethereum blockchain. Its launch is expected in early February 2026.

With approximately $6.4 trillion in AUM, this marks the first time a traditional financial giant of this scale has brought its own stablecoin to market. FIDD will be available to institutional clients through Fidelity Digital Assets and to retail investors through Fidelity Crypto.

FIDD in detail: structure and availability

The Fidelity stablecoin follows a conservative reserve structure. Each FIDD token is backed 1:1 by US dollars, cash equivalents, and short-term US Treasuries. Fidelity promises daily disclosure of issuance volume and reserves. Regular third-party attestations add further transparency. Additionally, the GENIUS Act requires monthly reports audited by a registered public accounting firm and certified by both CEO and CFO.

Users can trade FIDD on the in-house platforms Fidelity Digital Assets, Fidelity Crypto, and Fidelity Crypto for Wealth Managers, as well as on major crypto exchanges. Beyond that, the stablecoin can be transferred to any Ethereum mainnet address. Fidelity is already planning expansion to additional blockchains and Layer 2 networks.

Fidelity Digital Assets, National Association serves as the token issuer. This federally chartered National Trust Bank is headquartered in Boston. On December 12, 2025, the Office of the Comptroller of the Currency (OCC) granted conditional approval for conversion into a national trust bank. In total, the OCC approved five such applications that day: Fidelity, Circle, Ripple, BitGo, and Paxos.

Regulatory tailwind from the GENIUS Act

The launch comes at a strategically favorable moment. On July 18, 2025, President Donald Trump signed the GENIUS Act into law. This first comprehensive federal stablecoin legislation in the US establishes clear requirements for reserve backing, transparency, and oversight.

"[The GENIUS Act] creates a clear regulatory framework for what reserves should look like and how they should be managed. That is good for the industry and made this the right time for us to bring a product to market." - Mike O'Reilly, President, Fidelity Digital Assets

Specifically, the law requires full reserve backing with US dollars, bank deposits, or short-term Treasuries. Reserves must be strictly separated from corporate assets. Rehypothecation is permitted only in narrowly defined exceptions, such as margin coverage or short-term repo transactions. Furthermore, stablecoin issuers are prohibited from paying interest or staking yields to holders.

The supervisory structure is tiered by size. Initially, issuers below $10 billion can operate under state-level regulation. Above $10 billion, federal oversight applies, with a transition period of 360 days. Moreover, the law requires annually audited financial reports for issuers above $50 billion. In the event of insolvency, stablecoin holders enjoy priority over all other creditors.

")

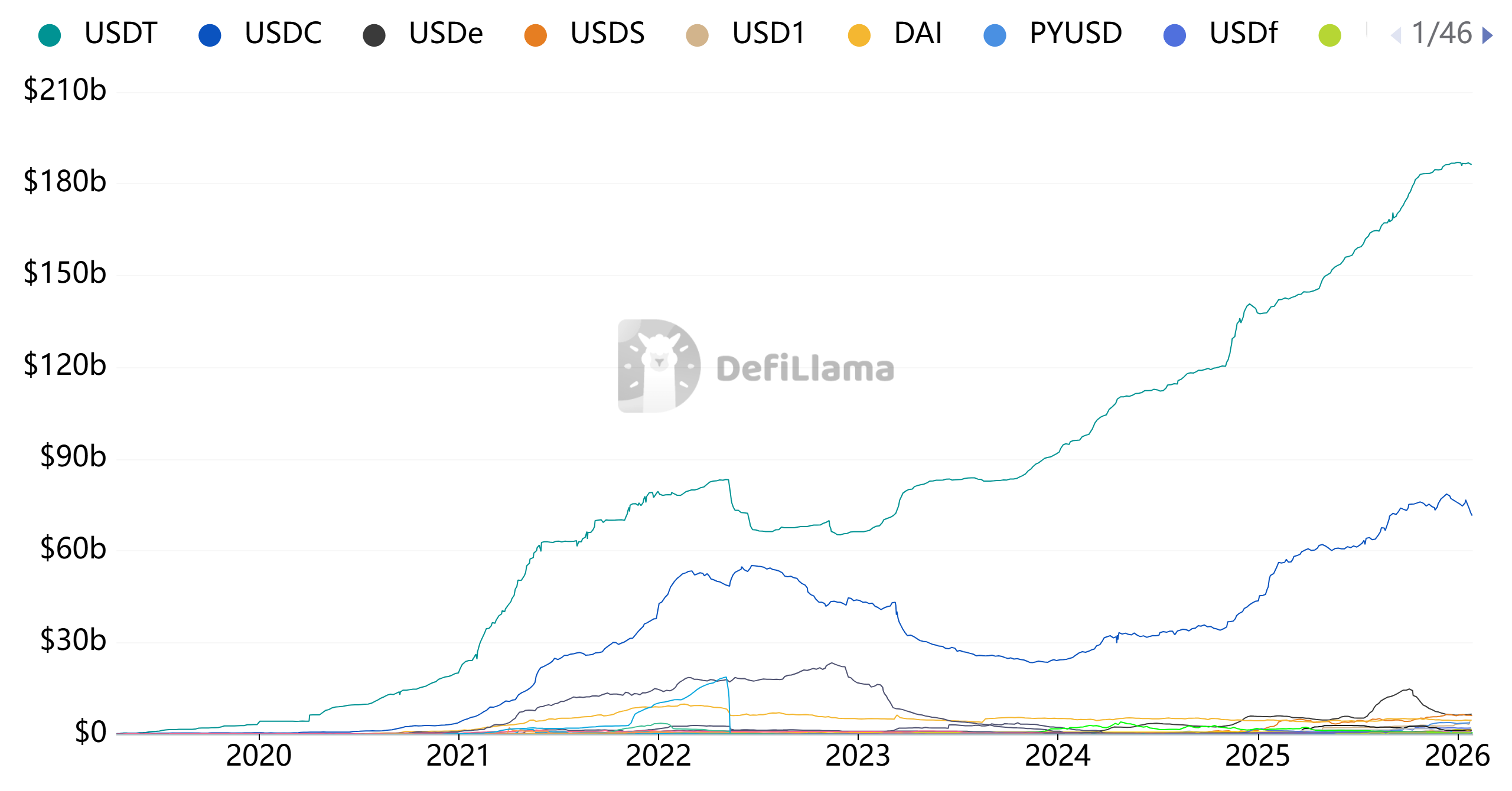

A market in transition

The stablecoin market recently surpassed the $310 billion mark in total capitalization. Tether (USDT) dominates with roughly 60 percent market share and approximately $187 billion. Circle's USDC follows with a capitalization of around $72 billion. Together, the two incumbents control over 90 percent of the market.

Still, new competitors are pushing forward. PayPal's PYUSD grew 216 percent to $3.8 billion in less than 90 days. Ripple's RLUSD reached approximately $1.3 billion since its December 2024 launch. One day before Fidelity's announcement, Tether launched USAT, a new federally regulated stablecoin through Anchorage Digital Bank.

Competition remains intense, yet the successes of new entrants need context. PayPal and Ripple, despite strong growth, have not even reached 10 percent of Circle's market capitalization. As such, the market remains highly concentrated. US Treasury Secretary Scott Bessent nonetheless projected a potential of up to $3.7 trillion by the end of the decade.

Fidelity's crypto history

The Fidelity stablecoin is the logical continuation of a strategy spanning over ten years. Back in 2014, Fidelity began Bitcoin mining and established a blockchain incubator. Then in October 2018, the company launched Fidelity Digital Assets as an institutional custody and trading platform. Fidelity was the first traditional financial firm to offer Bitcoin custody.

By 2019, the company had received a New York Trust Charter from the NYDFS. Then in April 2022, Fidelity became the first major retirement platform to introduce a Bitcoin option in 401(k) plans. FBTC followed in 2024 as the second most successful Bitcoin ETF of the year, with approximately $11.7 billion in net inflows. Most recently, the OCC approval as a National Trust Bank in December 2025 set the stage for the stablecoin launch.

This positioning sets Fidelity apart from the competition. The company combines over ten years of crypto experience with the reputation of an established asset manager. Both institutional and retail distribution channels operate under one roof.

Strategic significance for TradFi

FIDD signals a broader shift in the financial sector. Traditional institutions increasingly view blockchain as infrastructure for more efficient settlement and payments. Accordingly, stablecoins enable 24/7 transactions without the constraints of traditional banking hours.

For institutional clients, FIDD offers direct on-chain settlement. Retail users, on the other hand, gain a bridge between traditional Fidelity accounts and the crypto ecosystem. Integration into existing wealth management offerings could make FIDD accessible to clients who avoid conventional crypto platforms.

The business model is based on interest income from reserve holdings. At current Treasury rates, this interest margin proves attractive. Yet the GENIUS Act prohibits passing these returns on to stablecoin holders. As a result, the spread between zero-percent yield for customers and the returns from short-term government bonds flows entirely to the issuer.