Morgan Stanley is listing the Morgan Stanley Bitcoin Trust (MSBT) on NYSE Arca. As a result, it becomes the first major American commercial bank to issue a physically backed spot Bitcoin ETF under its own name. For the Bitcoin ETF market, this marks a new phase.

The annual management fee stands at 0.14 percent. Consequently, MSBT undercuts both BlackRock's IBIT at 0.25 percent and the Grayscale Bitcoin Mini Trust at 0.15 percent. Coinbase Custody handles Bitcoin custody in cold storage, while Bank of New York Mellon serves as administrator and transfer agent. Moreover, the fund uses the CoinDesk Bitcoin Benchmark 4 PM NY Settlement Rate as its benchmark. It launched with seed capital of approximately $1 million across 50,000 shares. In addition, the fund avoids derivatives, leverage, and active trading. On its first trading day, MSBT recorded net inflows of $30.6 million.

Aggressive fee structure as a distribution lever

The fee difference of 11 basis points compared to IBIT sounds marginal. However, when applied to large volumes, it has a significant impact. Morgan Stanley's wealth management division manages roughly $6.2 trillion in client assets and employs around 16,000 advisors. As a result, this distribution network - not the cost structure - is the real strategic advantage over pure asset managers like BlackRock or Fidelity.

MSBT is not primarily aimed at the open market. Instead, Morgan Stanley can integrate the fund directly into existing portfolios of its wealthy clientele. Since August 2024, the bank's advisors have been authorized to actively recommend spot Bitcoin ETFs to their clients. At that time, the approval was limited to IBIT and Fidelity's FBTC. Furthermore, the threshold stood at a minimum of $1.5 million in net worth and aggressive risk tolerance. With its own product, the bank no longer depends on third-party providers.

The timing is notable. Around 200 employees from risk, compliance, legal, and marketing worked on the launch. At the same time, Bitcoin is trading more than 40 percent below its all-time high of roughly $126,000. Since February, the price has ranged between $60,000 and $72,000. Therefore, Morgan Stanley is launching against the prevailing market sentiment. This suggests long-term conviction rather than short-term opportunism.

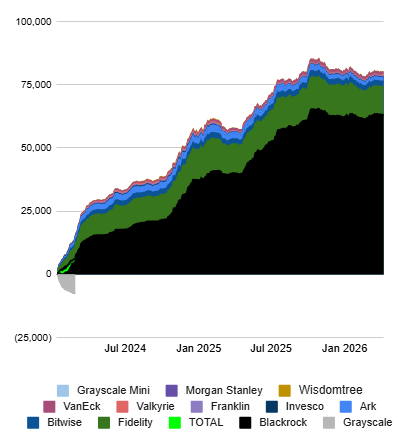

A market with over $85 billion and a clear leader

The US spot Bitcoin ETF market currently comprises more than ten products with a collective AUM exceeding $85 billion. BlackRock's IBIT dominates with approximately $54 billion in assets under management. Fidelity's FBTC follows at a considerable distance with around $13 billion. Since the SEC first approved eleven spot Bitcoin ETFs in January 2024, net inflows have surpassed $65 billion. In the first quarter of 2026 alone, $18.7 billion flowed in.

Nevertheless, the price decline has left its mark. Geopolitical tensions, uncertainty over US economic policy, and the unwinding of derivative leverage are weighing on the market. Nearly two years have passed since the last new spot Bitcoin ETF entered the market in July 2024. As a consequence, no issuer has dared to take the step since then.

According to Allyson Wallace, Global Head of ETFs at Morgan Stanley Investment Management, demand from wealthy clients was the catalyst. In the firm's view, the asset class is not going away. Moreover, recent 13F filings confirm this trend. Institutional ownership of spot Bitcoin ETFs stands at 38 percent. Consequently, the category is no longer a retail phenomenon. Morgan Stanley's entry as an issuer with direct access to 16,000 advisors is likely to further accelerate this dynamic.

Vertical integration rather than a standalone product

MSBT is part of a broader crypto offensive. In January 2026, Morgan Stanley also filed S-1 registrations for an Ethereum and a Solana ETF with the SEC. One month later, the bank submitted an application to the OCC for a National Trust Bank Charter. Specifically, the entity is named Morgan Stanley Digital Trust National Association. The application covers digital asset custody, fiduciary staking, and the purchase, sale, and transfer of tokens.

Furthermore, Morgan Stanley plans to offer direct spot trading of Bitcoin, Ether, and Solana through E*Trade during the first half of 2026. Zerohash serves as the infrastructure partner.

From the ETF to custody to direct trading, Morgan Stanley is building a vertically integrated crypto infrastructure. No other traditional financial institution in the US is currently pursuing a comparably comprehensive strategy. Moreover, preparations began as early as 2022, when the bank launched a crypto training program for all of its then more than 15,000 advisors. What often goes unnoticed: while competitors are still debating crypto strategy, Morgan Stanley is creating facts on the ground.

Regulatory foundation through OCC reforms

The Office of the Comptroller of the Currency provided the framework for Morgan Stanley's strategy. In late 2025, the regulator significantly lowered the regulatory barriers for national banks. Interpretive Letter 1186 allows banks to hold crypto assets on their balance sheets. Similarly, Interpretive Letter 1188 from December 2025 permits risk-free principal crypto transactions on behalf of clients.

In December 2025, the OCC approved five applications for new national trust bank charters in the digital assets space. Accordingly, Morgan Stanley's own charter application from February 2026 fits into this broader development. Specifically, the OCC reforms enable precisely the combination of custody, trading, and product distribution that Morgan Stanley is pursuing.

Other major wirehouses, by contrast, are responding far more cautiously. For instance, Merrill Lynch, UBS, and Wells Fargo continue to limit themselves to unsolicited crypto transactions. As a result, Morgan Stanley remains the sole active crypto intermediary among major US banks for now. The numbers speak clearly: whether competitors follow suit depends largely on the inflows MSBT generates over the coming months. Launching in the middle of a Bitcoin correction is either foresight or miscalculation.