")

The Swiss Bankers Association (SBA) has published a white paper describing the digital future of payments in Switzerland. The study focuses on the introduction of book money tokens (BGT) as a digital franc issued as a stablecoin by Swiss banks.

The tokens issued by the Bankers Association are intended to act as the digital equivalent of the Swiss franc and enable banks to process faster and cheaper payments. By using blockchain technology, the described book money tokens (BGT) could be managed securely and transparently. The whitepaper describes how digital francs can be integrated into existing payment systems to improve payments in Switzerland. Issuance by regulated banks is expected to contribute to Switzerland's future competitiveness, innovation and sovereignty.

raises billions through STRC: is the next Terra-Luna crash looming?")

")

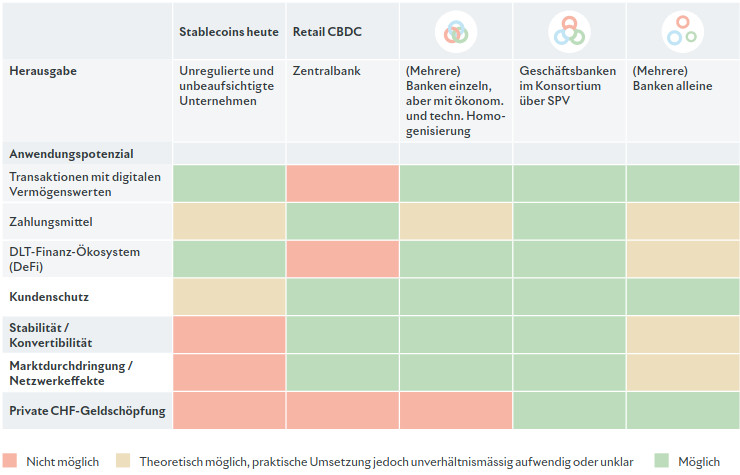

Book money token (BGT) as CBDC alternative

While central banks around the world are flirting with the introduction of CBDCs for the general public, the Swiss National Bank (SNB) sees innovation in this area as a matter for the private sector. The introduction of book money tokens (BGT) should help make the Swiss financial industry more competitive and facilitate access to digital payment options.

The Swiss Bankers Association (SBA) sees this as a new concept that could revolutionize the Swiss economy. BGT is issued by authorized Swiss banks and is accessible to everyone. The programmable token is also intended to enable banks to adapt their services to changing customer needs.

From the SBA's perspective, the BGT will play an important role in digital payments and trading of tokenized assets. A digital franc, it says, offers a simple and secure way to store and transfer money without worrying about price movements. The system is easy to use and can be managed online or via a mobile app on a smartphone, he said. The advantages of BGT, he said, lie primarily in its security and stability.

Swiss Banks Stablecoin

According to the Bankers Association, the ever-changing landscape of cryptocurrencies underscores the need for a stable and secure digital currency. Private stablecoins have often been volatile lately, he said. They also lack a key component necessary for widespread adoption: the official, regulatory support that only traditional money has, he said. Because the digital token is pegged to the Swiss franc, price fluctuations would be minimal and there would be no risk of the value moving sharply.

A crucial aspect for building trust is that the book-money token can be exchanged for conventional money at any time and at any institution that participates. BGT, like normal cash, is to be backed by assets such as balances at the Swiss National Bank or money market instruments on the issuer's balance sheet. Participating commercial banks issue BGT via a common investment vehicle and use reserves to secure the value of the digital franc.

"A special purpose vehicle (SPV) held jointly by participating commercial banks issues a single BGT backed by 100% or less of safe and highly liquid reserves." - Swiss Bankers Association (SBA) book-money token whitepaper

The book-money token would be issued and redeemed via smart contracts, with the token itself issued as a so-called registered security. However, in the white paper's most likely scenario, the joint tokens would be handled more like traditional deposits, rather than being 100% backed by highly liquid assets. A significant disadvantage compared to some stablecoins.

Advantages of a digital franc

The white paper reveals three basic variants for the book-money token, each with different economic, legal and technical characteristics. A centralized BGT system could be issued by a single bank. While this would be easy to implement, it would lead to a concentration of power and control that could threaten financial stability.

For local banking, the SBA sees the decentralized system, issued jointly by several banks, as making the most sense. This model is less prone to concentration of power and control, it says, but may be more difficult to implement. Ultimately, the choice of BGT design depends on specific requirements and objectives. A well-designed book-money token could help improve the efficiency of the financial system and increase consumer confidence.

A digital franc would have the potential to strengthen Switzerland's position as a global financial center. By providing a safe and stable digital currency, Switzerland could attract companies and investors looking for a safe haven for their funds. This would have a positive impact on the country's economy and create new employment opportunities in the banking and financial services sector.

Regulatory and technical issues

Important regulatory and technical issues remain to be resolved before the book-money token can become a reality. The results could potentially cause the project to fail. A fundamental issue is the question of legal certainty, as this is the only way people can fully trust the digital currency. The authors believe that the foundations for this are in place in Switzerland, in the form of the innovative DLT legislation.

Basically, it must be clarified whether the banker's construct BGT is considered a means of payment or would be a security after all due to the deposits. This decision is in the hands of the Swiss Financial Market Supervisory Authority (FINMA). Should the token be classified as a security, this would be associated with such significant restrictions that it would probably mean the end for a digital franc project.

As with a CBDC, important questions remain open for consumers, such as the anonymity of payments and guarantee of privacy. This is all the more true because with a blockchain-based currency, the entire chain of transactions can be tracked. Conventional public blockchains such as Bitcoin and Ethereum cannot protect the privacy of accounts in their current form.

![S&P Dow Jones Indices licenses the S&P 500 to Trade[XYZ] for the first officially licensed S&P 500 perpetual contract on Hyperliquid.](https://cryptovalleyjournal.com/wp-content/uploads/2026/03/CVJ.CH-SP-Dow-Jones-SP-500-Hyperliquid-450x300.jpg "S&P Dow Jones Indices licenses S&P 500 for perpetual contracts on Hyperliquid")