A summarizing review of what has been happening at the crypto markets of the past week. A look at trending sectors, liquidity, volatility, spreads and more. The weekly report in cooperation with market data provider Kaiko.

The last 7 days in cryptocurrency markets:

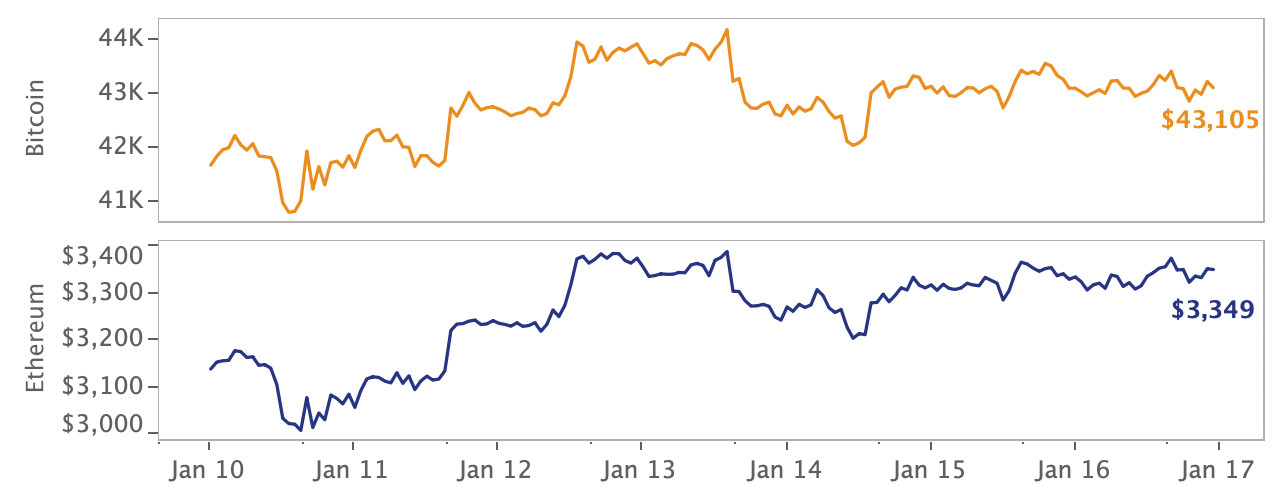

- Price Movements: Bitcoin recovered slightly following the release of the latest inflation data, although risk sentiment remains highly volatile.

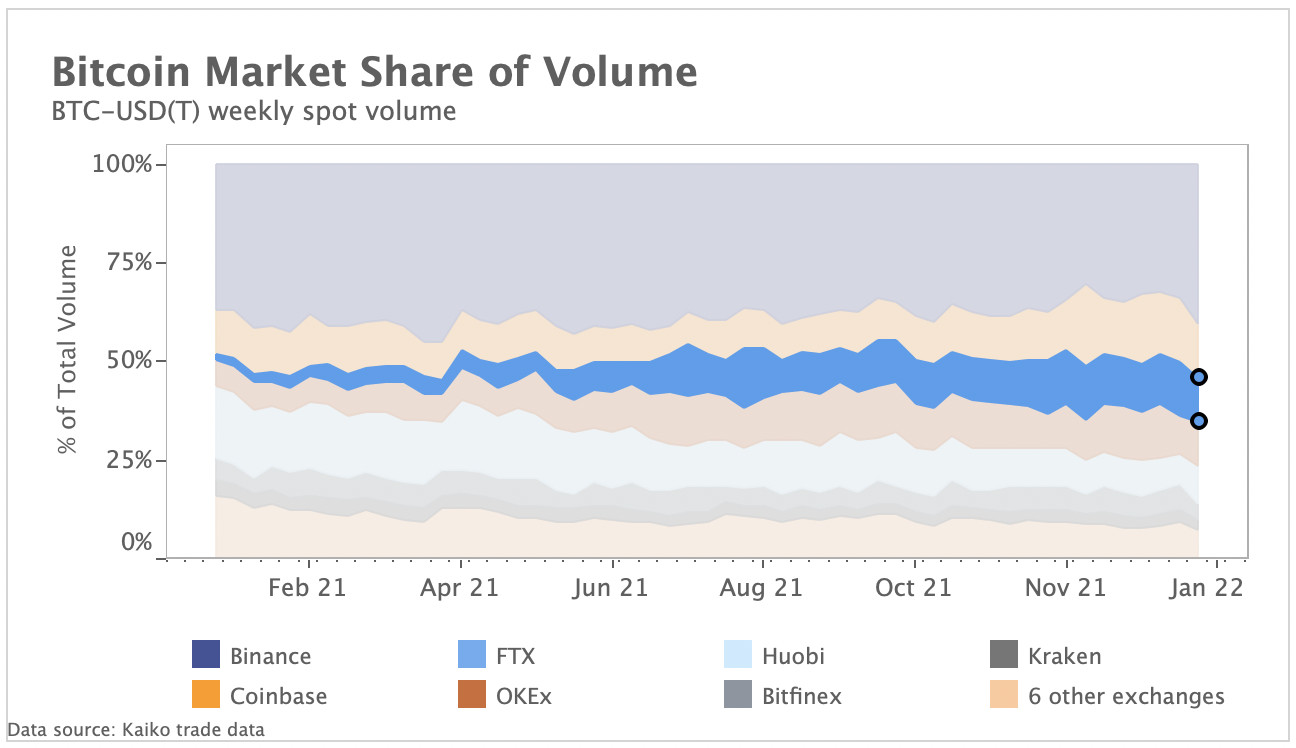

- Volume Dynamics: FTX's market share continues to gain ground versus its biggest competitors.

- Order Book Liquidity: Liquidity is highly fragmented between assets on the same exchange.

- Derivatives: Funding rates flipped negative on all exchanges for the first time since early December.

- Macro Trends: Publicly-listed crypto mining companies have crashed double digits over the past few months.

Volatile Risk Sentiment Fuels Soft Recovery

Bitcoin and Ethereum showed signs of recovery following the release of the latest CPI numbers revealing inflation is at 40-year highs. Meme coins and Layer 1 tokens also made strong gains last week, although overall market sentiment remains uncertain. Trade volumes have been stagnant since early December and derivatives markets show few signs of exuberance, with the CME’s futures premium all but evaporating and funding rates flipping negative. In wider industry news, exchanges continued their acquisition binge: Coinbase acquired a regulated derivatives exchange, Gemini acquired a digital asset management startup, and Brazil’s Mercado Bitcoin acquired a Portuguese exchange.

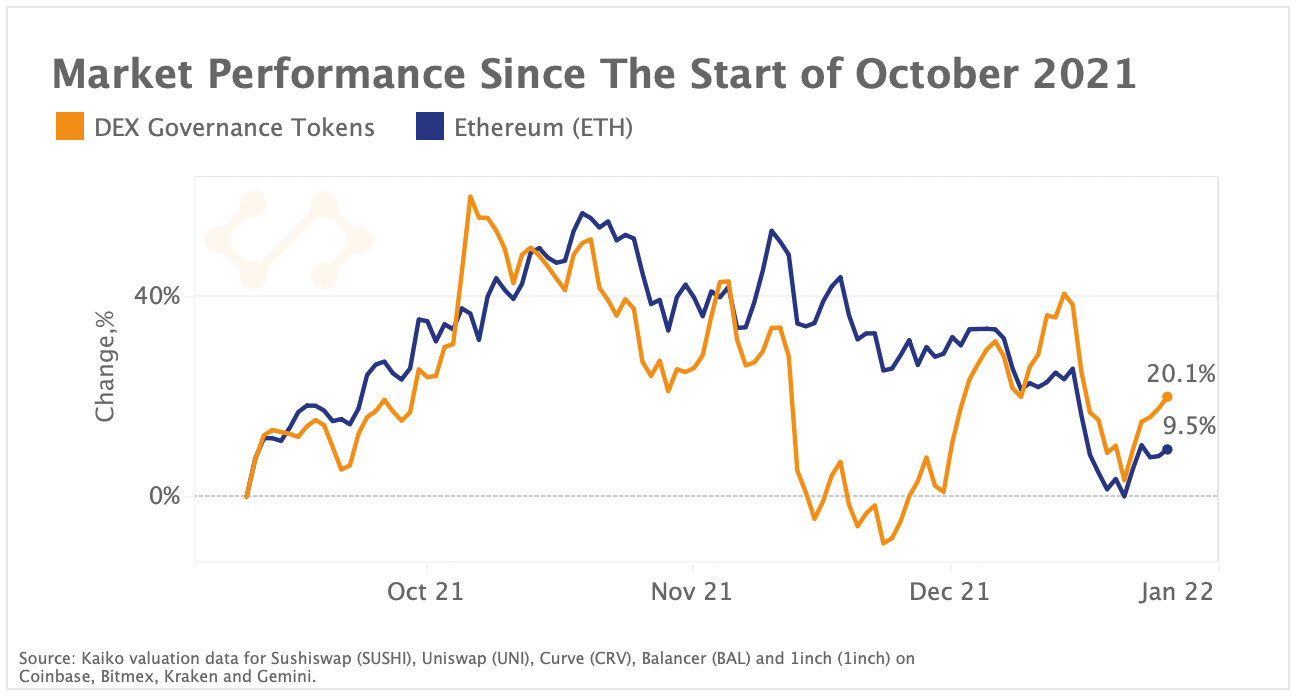

DEX tokens outperform ETH

Historically, DEX tokens have been tightly correlated to the price of ETH, but over the past two months we can observe a divergence in price action. The majority of DEX activity happens on the Ethereum blockchain, but high transaction fees have taken a toll on the profitability and growth of these protocols, leading several to launch on alternative Layer 1 networks and Layer 2 scaling solutions. Above, we compare the performance of ETH and a simulated DEX portfolio tracking the composite returns of the native tokens for Uniswap (UNI), Curve (CRV), Sushiswap (SUSHI), Balancer (BAL), and DEX aggregator 1inch.

DEX tokens diverged sharply from ETH at the start of December, and since October have outperformed ETH significantly. The shift comes following a series of positive updates for the industry, including the launch of Uniswap on the Layer 2 network Polygon and the continued growth of yield farming on Curve Finance. Conversely, ETH has failed to capture investor attention amid rising macro uncertainty and scalability struggles. Should DEX’s continue to expand and gain users on alternate networks, we can expect its correlation with ETH to weaken.

FTX gains market share to Binance

The increasingly high-stakes competition between cryptocurrency exchanges reached a new level this week following Coinbase’s acquisition of a regulated derivatives exchange, a few months after FTX announced a similar purchase. FTX has always been well known for their derivatives products, but struggled in spot trading relative to giants like Binance and Coinbase. However, that all changed this year.

Above, we chart the market share of spot volume for BTC-USD(T) pairs on 13 exchanges. In just 1 year, FTX’s market share increased 7-fold, from ~2% in early 2020 to 14% as of January 2022. Coinbase’s market share spiked from 10% to 16% over the same period. By contrast, the world’s largest exchange Binance saw its share shrink from 40% to 33%. Huobi registered an even stronger decline from 17% to 8%. Both exchanges have likely been impacted by China’s crypto crackdown and strong regulatory restrictions around the world.

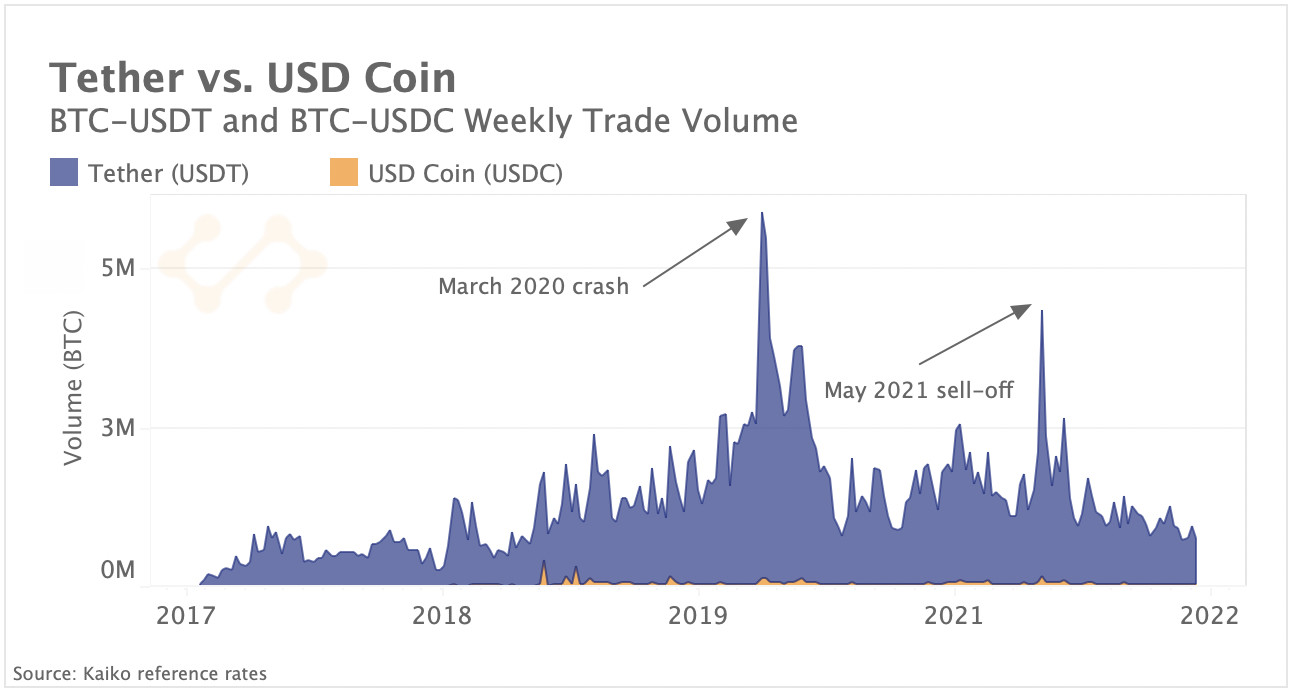

USDC volume remains low on centralized exchanges

Last week, it was reported that the stablecoin USD Coin’s (USDC) total supply on the Ethereum network surpassed Tether’s (USDT) for the first time. This is big news considering the fact that Tether has been the dominant stablecoin for years and underpins the majority of all trades that occur on centralized exchanges. Today, USDC is mostly used in decentralized finance and is one of the highest volume assets trading on DEXs. Its growing use in DeFi has contributed to its exponential increase in total supply.

Yet, when it comes to the stablecoin’s use in centralized markets, it strongly trails Tether and has not undergone a significant increase in usage. Above, we chart the total volume for Bitcoin - Tether and Bitcoin - USDC pairs aggregated across all exchanges. We can observe that BTC-USDT volume is magnitudes greater than BTC-USDC volume, which suggests USDC doesn’t play a strong role in price discovery. The unique features of DeFi incentive models could be contributing to USDC's increasing supply, while Tether's supply has stayed flat amid low centralized exchange volumes.

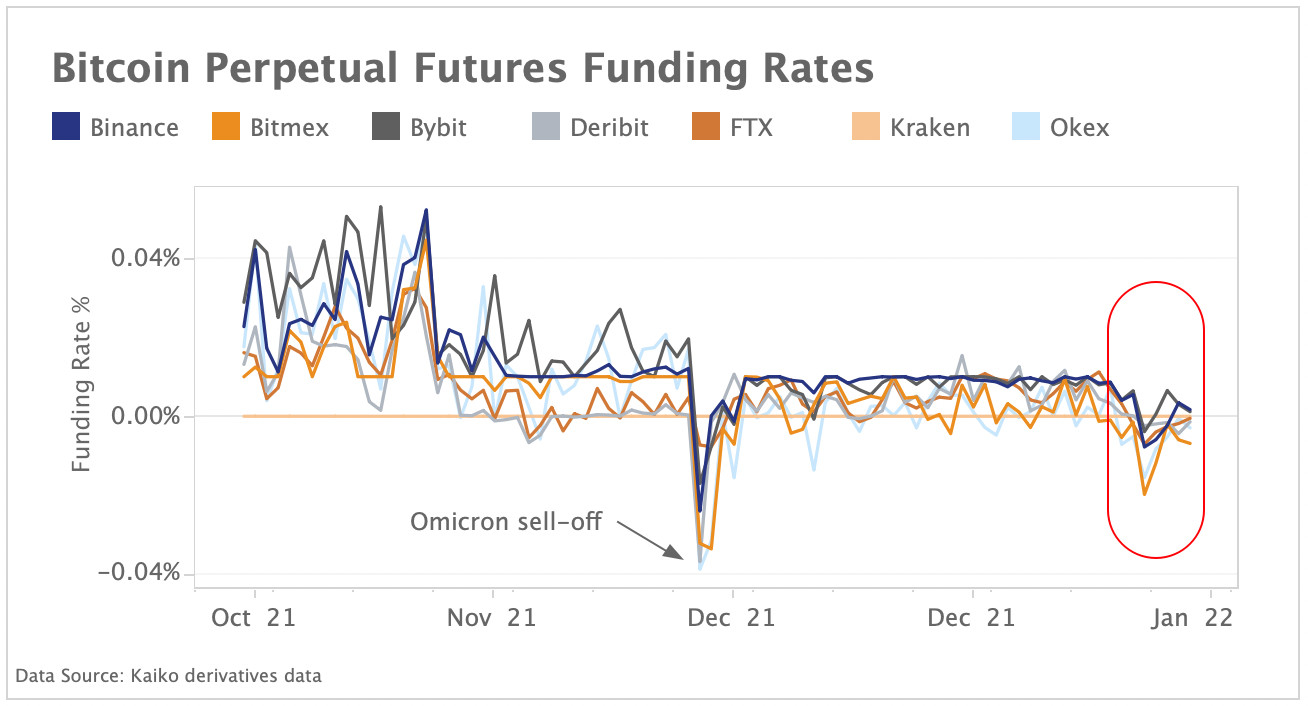

Funding rates flip negative, open interest stagnates

Bitcoin’s funding rates turned negative last week for the first time since the Omicron sell-off in early December. Strong inflation readings in the U.S. injected volatility into the market with Bitcoin trading sideways last week despite ending the week in the green. Funding rates are the cost of holding a long position and a gauge of overall market sentiment and bullish demand. When they are negative it means that shorts are paying longs to hold their position and bullish demand is muted. Funding rates (charted above) fell to as low as -0.02% on Bitmex and Okex on Jan 12, and remained negative on most exchanges throughout last week despite recovering on retail oriented Binance and Bybit.

Bitcoin’s perpetual futures open interest has also declined since November’s highs. Despite recovering slightly after the Omicron sell-off, it currently sits around $10B indicating that capital inflows into the market are low. Open interest dipped following the release of the Fed minutes on January 5th, and have since yet to recover.

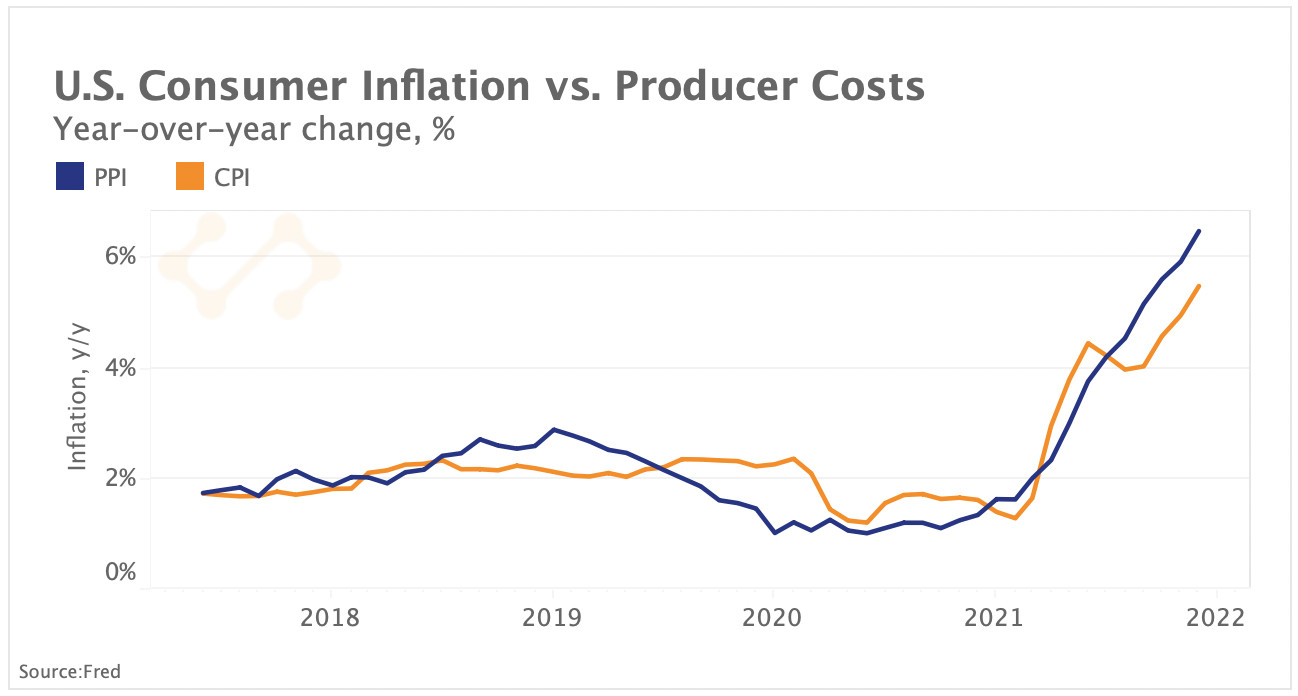

Risk sentiment remains volatile as inflation hits decade highs

Investors recovered some risk appetite last week after U.S. headline consumer inflation matched market expectations, despite hitting a four-decade high. Both equities and bitcoin rose immediately following the release of inflation data before losing their gains over the next days as markets focused again on the U.S. central bank tightening cycle. Above we chart the consumer (CPI) and producer (PPI) price indexes, excluding volatile food and energy prices. Both have been rising steadily over the past year hitting multi-decade highs, as surging demand for goods coupled with ongoing supply constraints push prices up.

The PPI, which is often seen as an early measure of inflation because it considers the change in prices producers receive at the factory gate, has increased faster than consumer prices since July. While most companies have been able to manage rising costs and earnings have been exceptionally strong over the past year, wage growth and persistently high inflation are putting pressure on profit margins and equity performance.

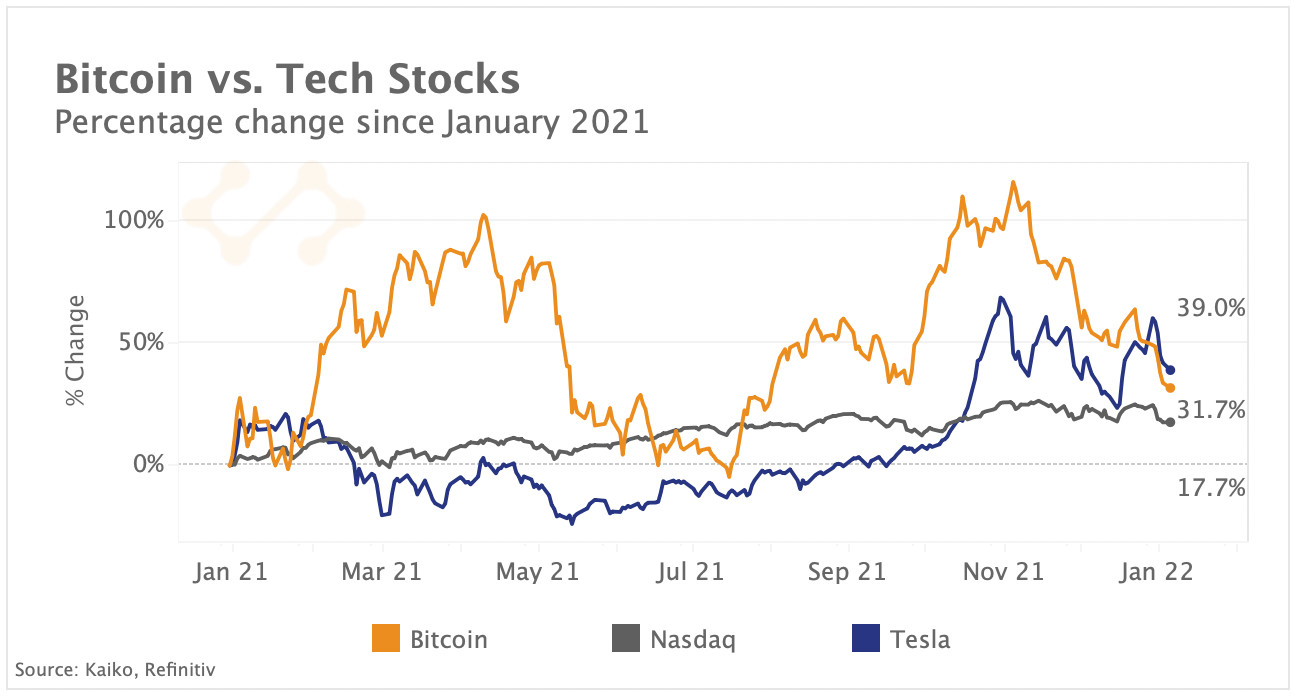

Bitcoin is highly correlated with tech stocks

With the U.S. central bank preparing for its first rate hike in four years, risk assets such as tech stocks and crypto have experienced a rocky start to the year. The Nasdaq composite flirted with correction territory last week - a 10% fall from its recent peak - as investors aggressively rotated from rate-sensitive growth stocks to value stocks. Above, we chart the percentage change in price returns of Bitcoin, the Nasdaq Composite Index and Tesla since January 2021. The electric car-maker which added $1.5B worth of BTC to its balance sheet in early 2021, has been strongly correlated with Bitcoin over the past year (0.52 positive correlation in December). Overall, both BTC and Tesla outperformed the broader tech-heavy Nasdaq in 2021.

However, since the U.S. Fed took a decisively hawkish shift in November, both crypto and tech stocks tanked, underperforming the broader index. Bitcoin is down 30% since November with most altcoins following suit while Tesla lost 13%.

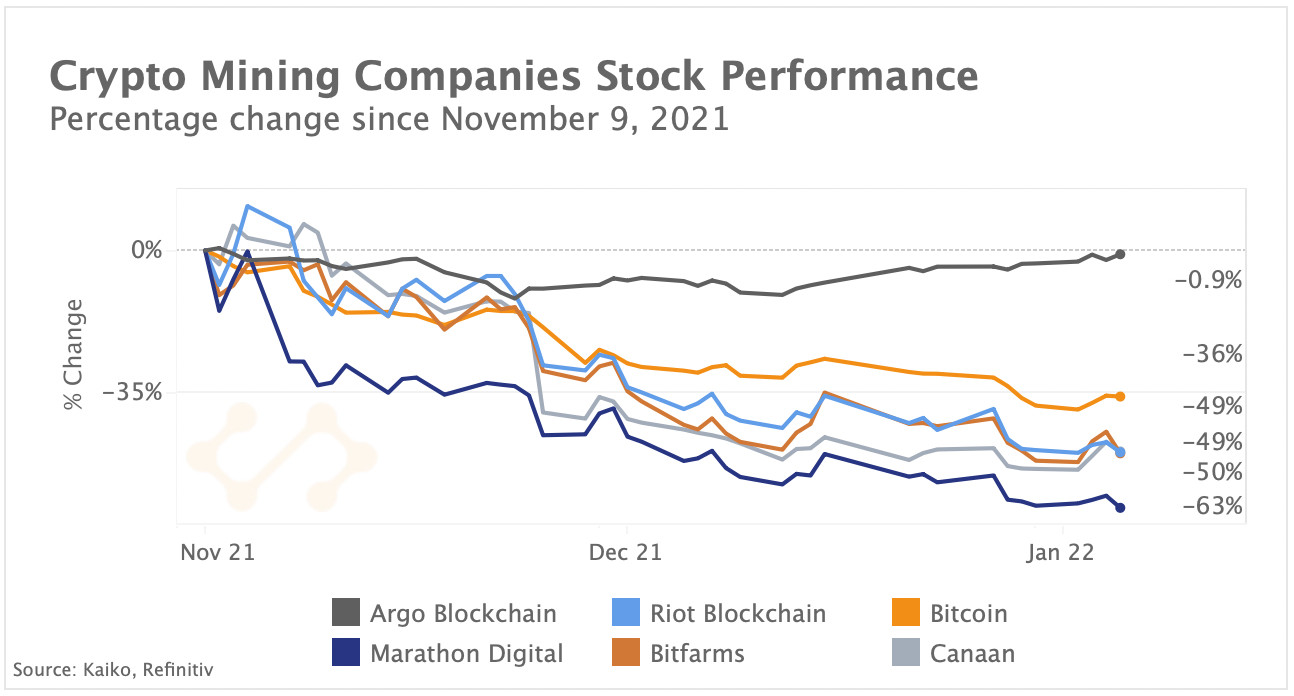

Crypto mining stocks suffer double-digit losses

Crypto mining companies, which are often viewed as a way to gain exposure to Bitcoin, have suffered along with BTC’s price since November. Nasdaq-listed Marathon Digital was the worst performer, falling by 63% since BTC’s all-time high on Nov 9. However, despite the overall risk-off sentiment, London Stock Exchange-listed Argo Blockchain outperformed Bitcoin registering a relatively small 1% decline. U.S. mining companies have benefited heavily from Bitcoin miners’ migration from China, following the country’s crackdown last year. To expand their activity, miners are increasingly relying on debt financing and equity issuance, instead of selling their Bitcoin holdings.

Furthermore, some companies are actively accumulating Bitcoin with the largest U.S. miners collectively holding over $1.1B worth of BTC according to the Block. While this strategy has reduced selling pressure in the market, it might prove risky during strong market volatility such as the March 2020 market crash.