A summarizing review of what has been happening at the crypto markets of the past week. A look at trending sectors, liquidity, volatility, spreads and more. The weekly report in cooperation with market data provider Kaiko.

The last 7 days in cryptocurrency markets:

- Price Movements: Bitcoin traded above $42k and Ethereum above $3k for the first time since mid-January.

- Volume Dynamics: Uniswap accounts for more than 80% of Ethereum DEX market share.

- Order Book Liquidity: Over the past week, price slippage has increased sharply for BTC and ETH trading pairs.

- Derivatives: Ethereum options volumes broke all time highs and equaled Bitcoin's for the first time.

- Macro Trends: European bond yields spiked after the ECB took a surprisingly hawkish turn.

Crypto markets slightly recover

Cryptocurrency markets recovered over the weekend following another massive DeFi hack and a dismal earnings report for Meta (formerly Facebook). More than $326 million in ETH was siphoned from Wormhole, a popular bridge connecting the Ethereum and Solana blockchains, ranking as one of the largest hacks in the history of crypto. Meta's rough earnings report also shook tech stocks and metaverse-affilated crypto projects, although traditional markets were buoyed by a stronger-than-expected jobs report, which demonstrated economic resilience despite rising inflation. Bitcoin traded above $42k and Ethereum above $3k for the first time in two weeks and altcoin markets showed signs of a slight recovery.

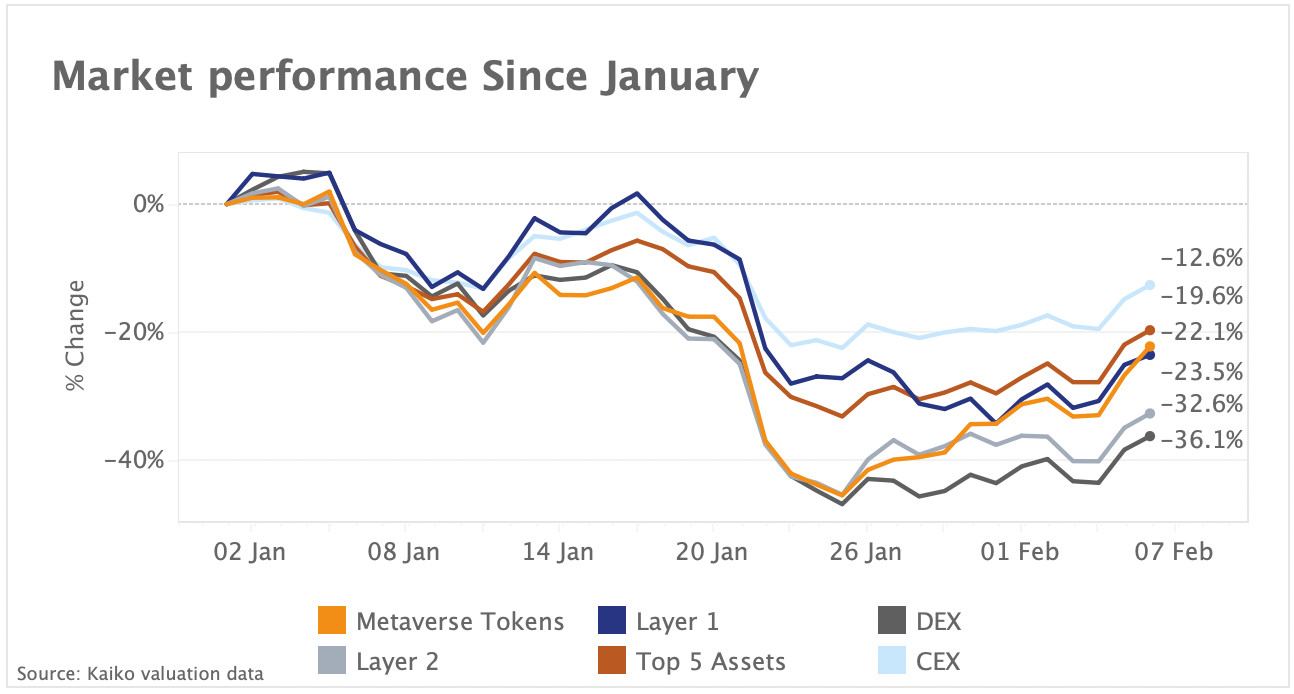

DEX and L2 tokens are worst performers of 2022

Overall, crypto assets remain tightly correlated to the price of Bitcoin. Yet, the magnitude of returns frequently diverges across sectors, and there have been strong differences in performance since the start of 2022. We built 6 simulated portfolios tracking composite returns of the top 5 tokens per sector ranked by market cap.

We can observe that our centralized exchange (CEX) token portfolio registered the smallest decline of around 13%, closely tracking Bitcoin’s spot performance. FTX’s FTT token contributed most to these gains, up nearly 17% after the exchange raised $400mn in a Series C funding round and acquired Japanese rival Liquid.

By contrast, decentralized exchange (DEX) tokens were the worst performers, down by over 36%. Despite Meta’s disappointing quarterly results last week, metaverse-linked tokens have gained ground, outperforming Layer 1 and Layer 2 scaling solutions. Most Layer 1 tokens took a hit following last week's hack of Wormhole, which suggests an interoperable, multi-chain future is far from being reality just yet.

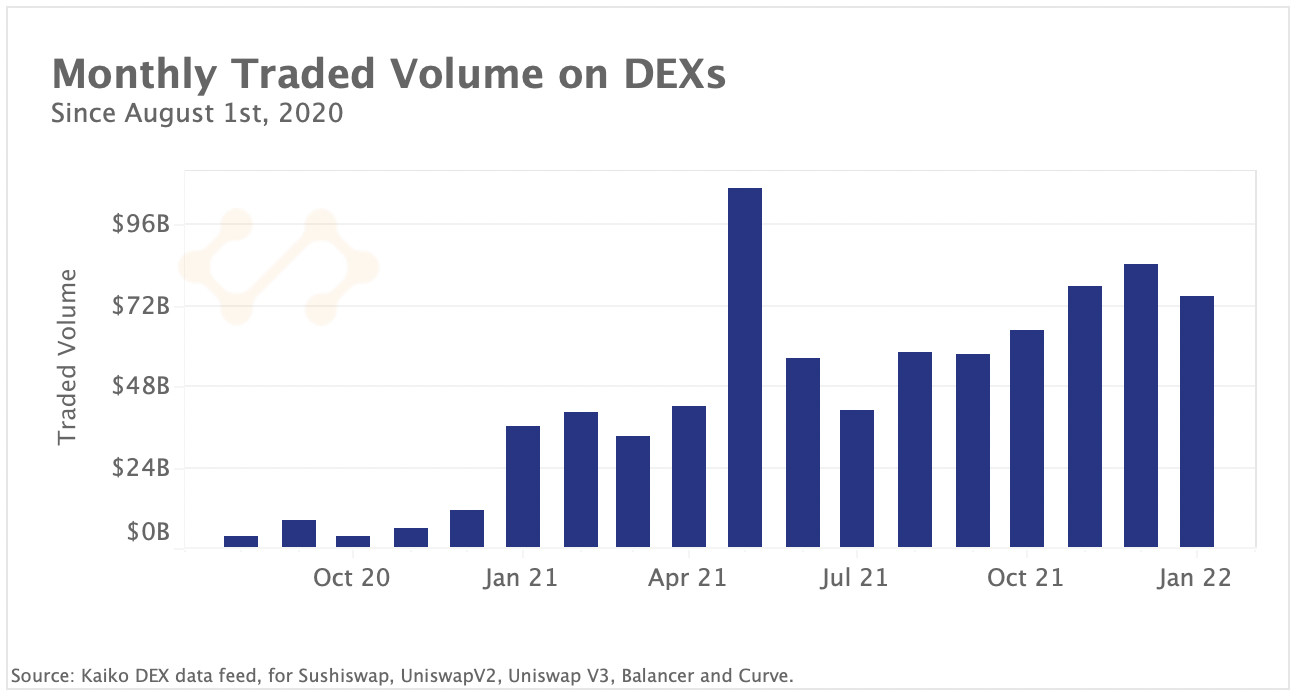

DEX volumes dip in January while Curve volume spikes

Trade volume on the leading Ethereum-based DEXs decreased in January to $75B, alongside the broader crypto market downturn. The decline was mainly due to falling trading activity on Uniswap which today accounts for 80% of total volume. Trading activity on Curve, a DEX optimized for stablecoin swaps, bucked the trend and saw volumes rise from $5B in December to $9B in January as investors flocked to the exchange in search of stablecoin liquidity.

On Jan 28, Curve’s daily volume spiked to its highest level since last May, as traders reportedly scrambled to trade out of algorithmic stablecoin Magic Internet Money (MIM). Confidence in the stablecoin plummeted following revelations that the issuing organization's treasurer Sifu is the co-founder of failed Canadian exchange QuadrigaCX and an alleged scammer. This triggered a liquidity crisis for MIM, and it quickly became the highest volume liquidity pool on Curve.

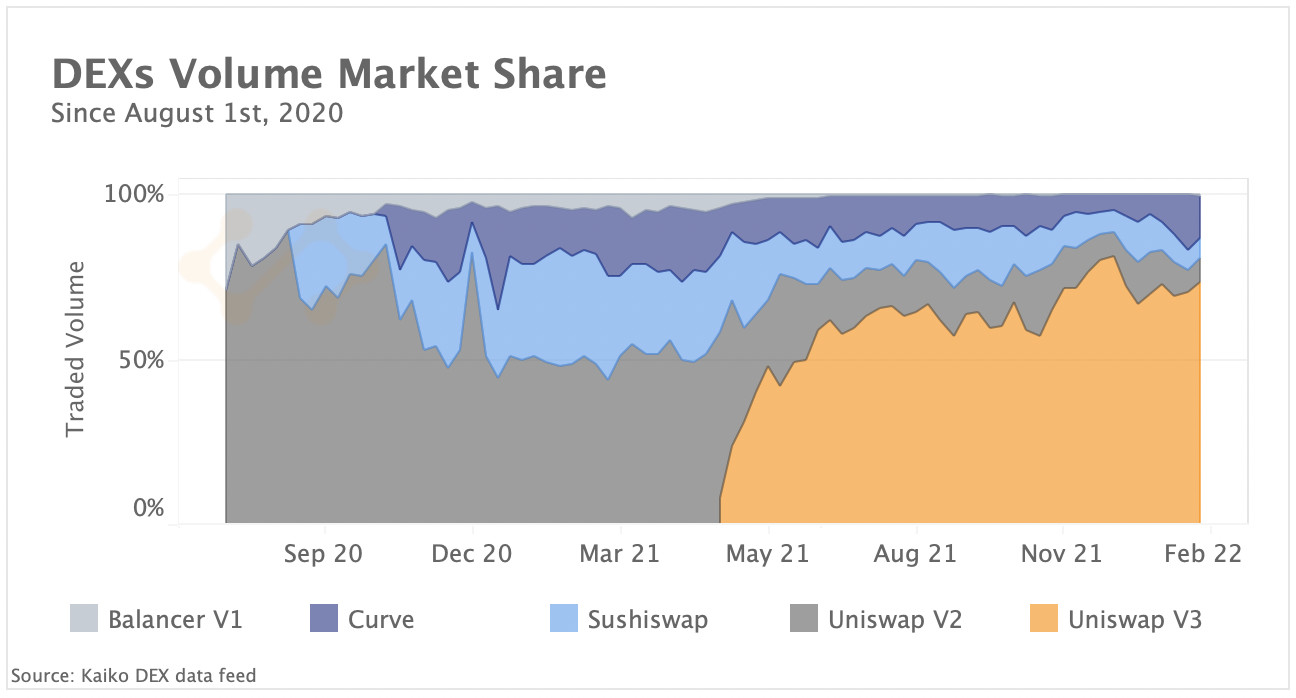

Overall trade volume on Curve remains relatively low compared with other DEXs. Below, we chart the market share of volume by exchange and we observe that Uniswap (V2+V3) remains the market leader with over 80% of total volume.

Curve’s market share increased over the past month hitting its highest level since May 2021, in part due to high volatility which attracts traders who tend to favor stablecoins in times of uncertainty.

Despite a relatively low market share, Curve holds the largest share of DeFi total value locked (TVL) on Ethereum (13%) -more than twice Uniswap’s TVL. This is due to Curve's unique model for issuing liquidity rewards, which has caused TVL to skyrocket as pools battle to attract liquidity, creating a phenomenon known as the “Curve Wars.”

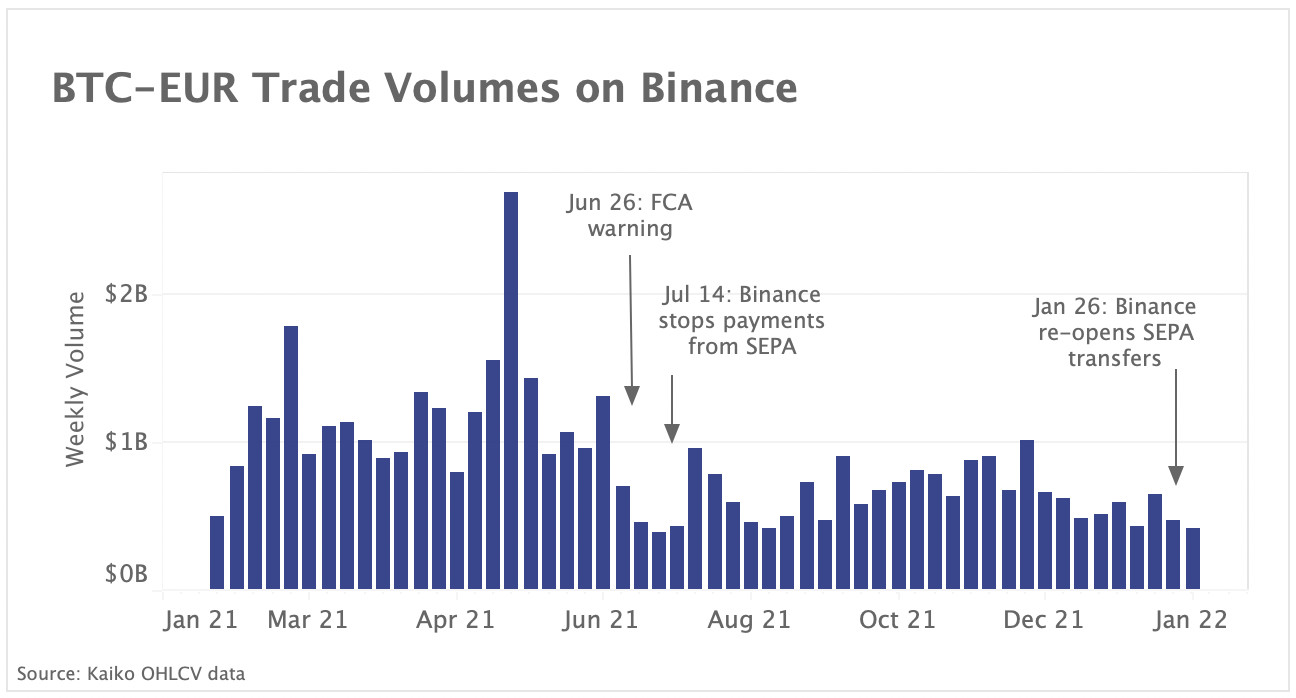

BTC-EUR volume falls sharply on Binance

Bitcoin trades executed against the Euro fell steeply last year following a regulatory crackdown on Binance in the region. In July, the exchange temporarily halted transfers from the European Union’s Single Euro Payment Area Network (SEPA) and discontinued its derivative offerings in Germany, Italy, and the Netherlands. The average weekly BTC-EUR volume hovered around €470mn last month, down from €800mn in November and over €1bn in the first six months of 2021. The exchange recently re-opened SEPA transfers, although this has yet to have an impact on euro-denominated transactions. The European Central Bank’s recent hawkish shift, which spurred a sharp rise in European bonds yields last week, could put additional pressure on crypto demand in Europe.

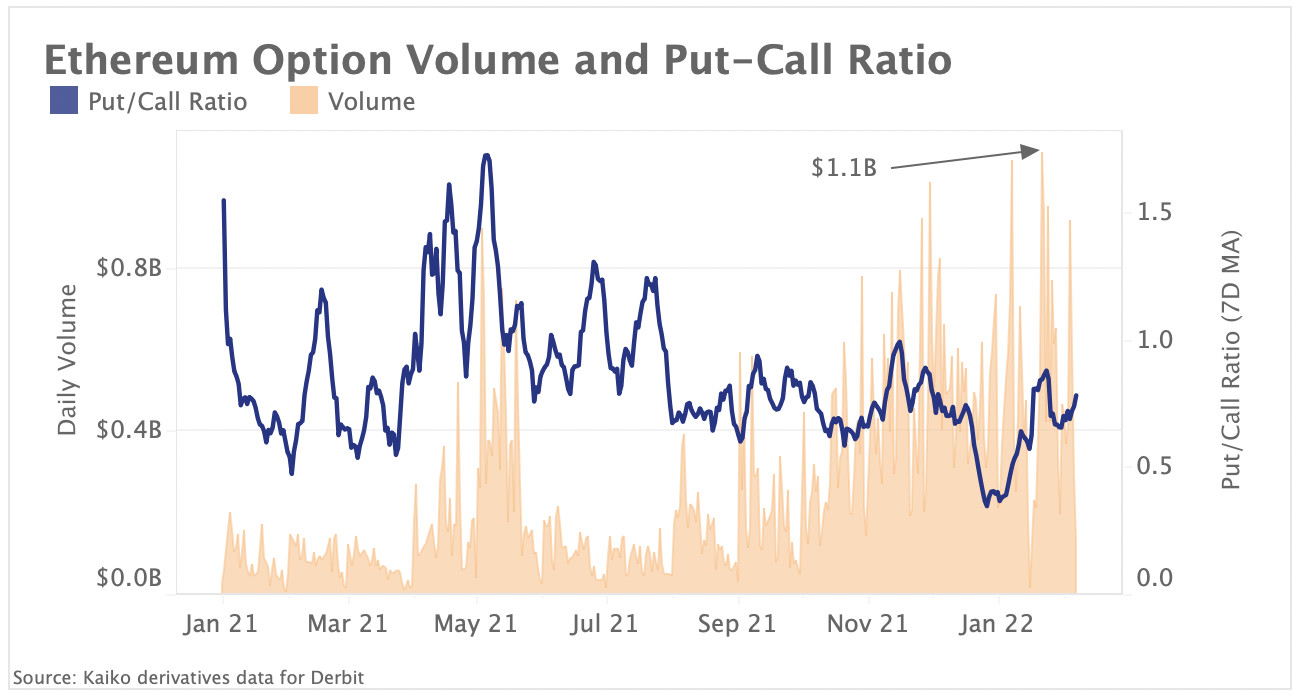

Ethereum options volume breaks all time high

Ethereum’s daily option trade volume broke all time highs above $1.1 billion at the end of January and equalled Bitcoin’s for the first time last week. The surge in options volume comes as spot volumes remain muted and prices suffer a steep correction. Options markets are still relatively underdeveloped compared with futures and perpetual futures, and more mature crypto options markets could strongly impact market structure and price discovery.

Above, we chart Ethereum’s daily trade volume on Deribit, the largest cryptocurrency options exchange, along with the put-call ratio. We observe that daily trade volume has surged since November along with Ethereum’s volatile put-call ratio, which is calculated by taking the ratio of the traded volumes of puts vs. calls. Typically, a rising ratio is viewed as bearish since it suggests that traders are purchasing more puts (bearish bets) than calls (bullish bets). The put-call ratio rose to .85 in the first half of January before declining to .78, suggesting options traders are uncertain about future price movements.

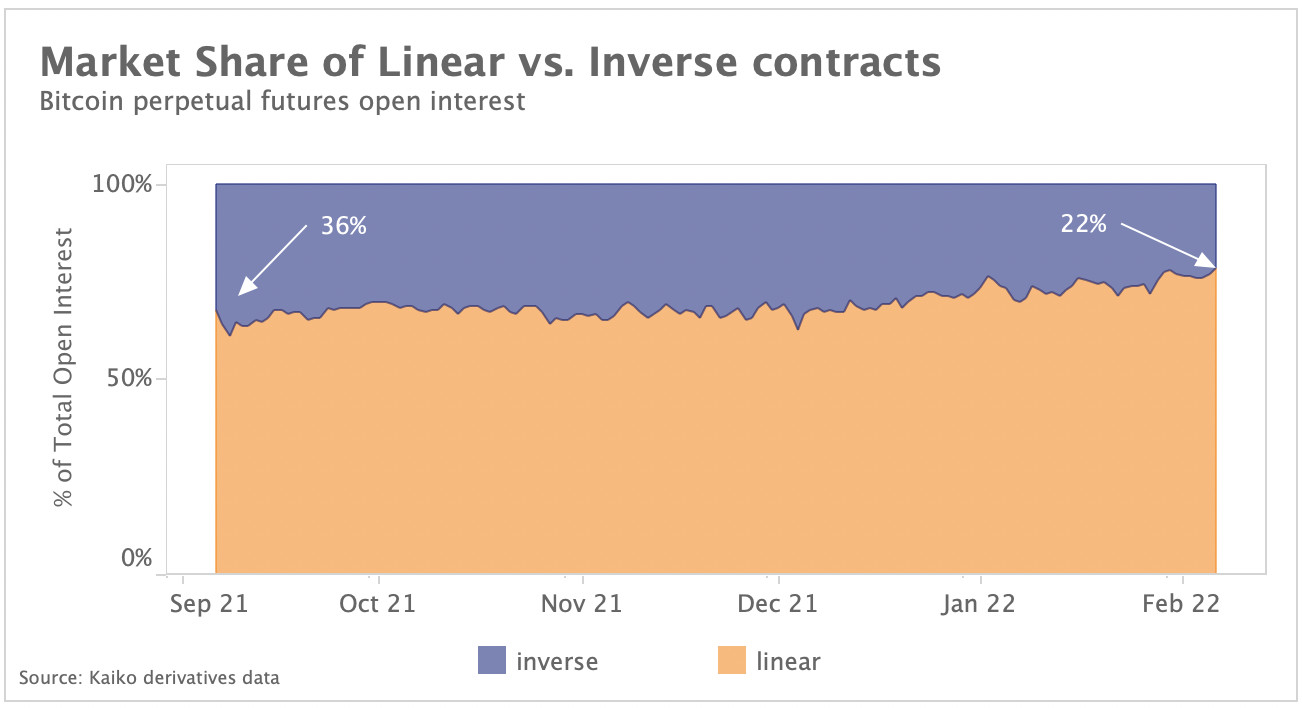

Traders increasingly prefer linear contracts

Cryptocurrency derivatives markets have historically suffered massive liquidation cascades with price volatility. While the latest sell-off triggered hundreds of millions in long liquidations, the magnitude of leveraged shakeouts appears to be lessening overall. One reason could be due to traders increasingly preferring linear contracts, as opposed to inverse.

Inverse contracts are margined and settled in the base currency (in this case Bitcoin) and the value of the margin varies with the asset's price movements, making them more vulnerable to liquidations. Linear contracts are margined with USD or stablecoins, thus the value of collateral does not shift with price volatility. Above, we chart the market share of open interest for inverse vs. linear perpetual futures contracts since the start of September. We can observe that the market share of inverse contracts has declined from 36% to 22% of total open interest since September. Together with lower leverage limits on major exchanges, this could explain why price volatility has had a more limited impact on derivatives markets over the past few months.

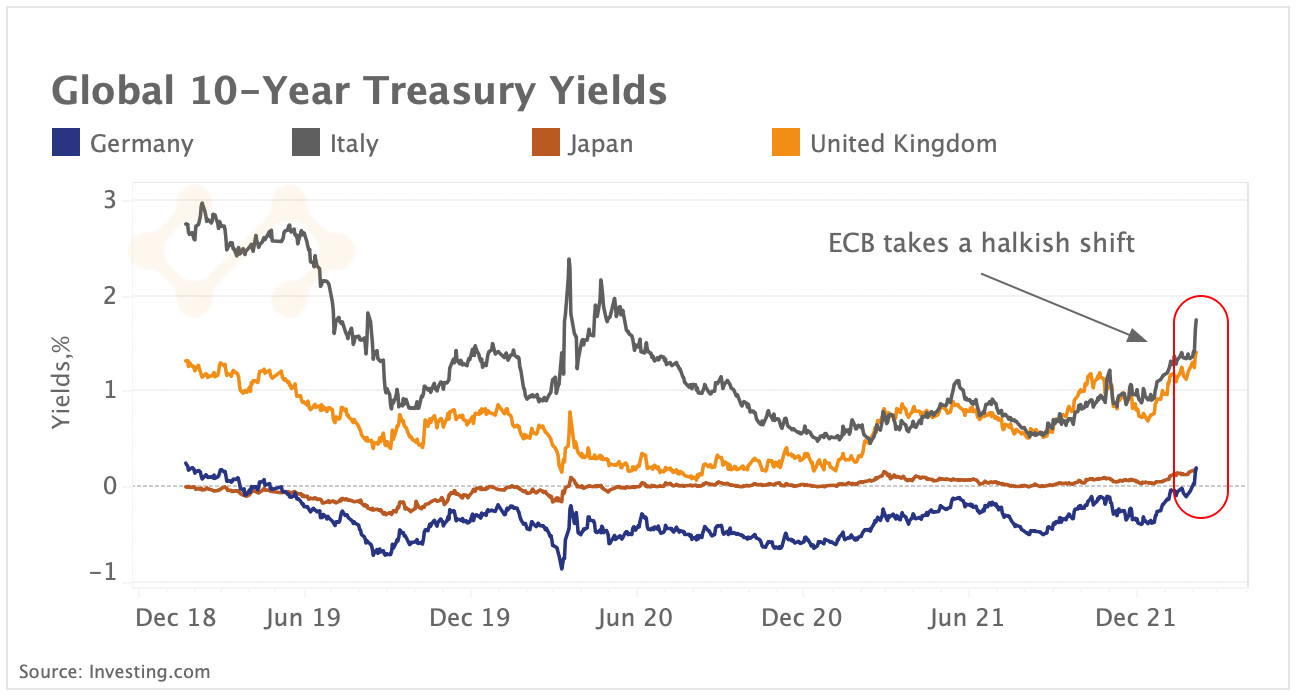

European yields rise as ECB takes hawkish stance

Markets ramped up global rate hike bets last week, after the European Central Bank (ECB) and the Bank of England (BoE) took a hawkish shift spurring a sell-off in European bonds. Above, we chart the 10-year treasury yields in Italy, Germany, the United Kingdom and Japan. We observe that yields - which move inversely to prices - spiked in all countries to multi year highs. Yields on Italy’s 10-year treasury notes registered the strongest weekly increase of over 40bps. German yields turned positive for the first time since 2019. Japanese yields hit their highest levels since the start of the country’s negative interest rates policy in 2016. While the European bond market has been protected by the ECB’s more dovish stance relative to the Fed over the past year, the recent ECB move has pushed investors to aggressively reprice interest rates expectations. This will add to rampant tightening fears and risk aversion which have dragged down riskier assets over the past months.

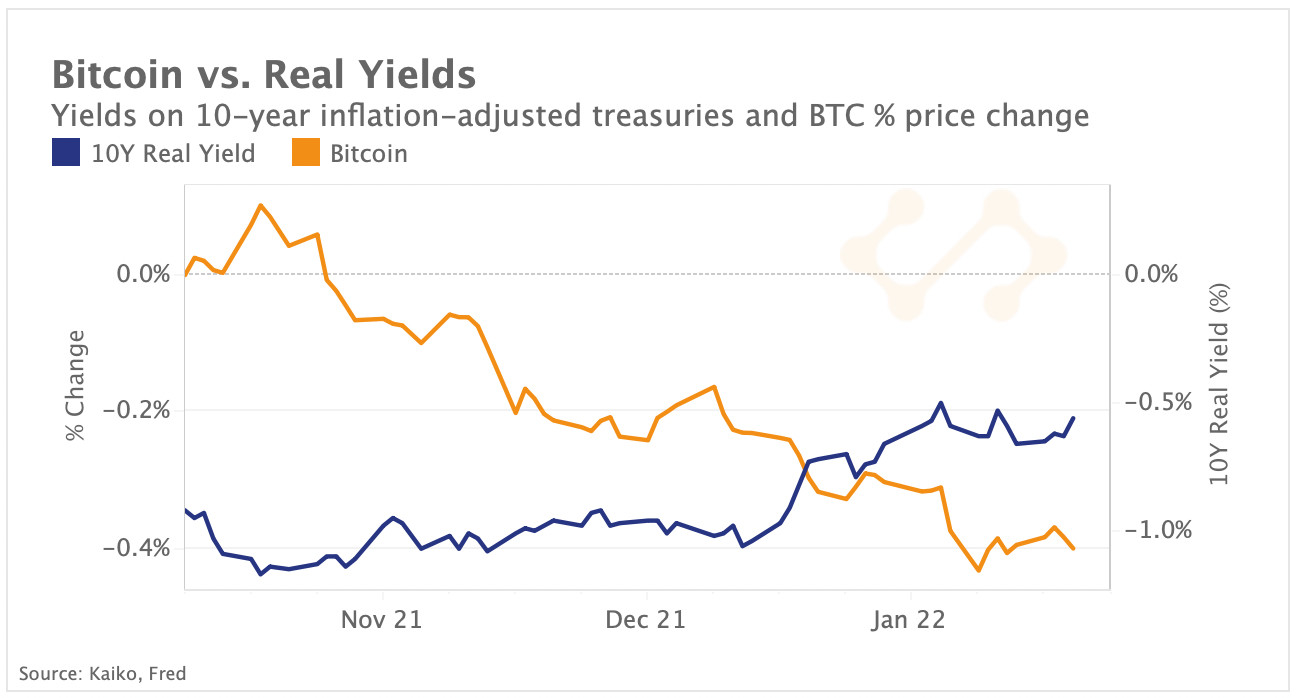

Bitcoin's correlation with yields

U.S. markets mirrored European and Asian markets after a surprisingly strong jobs report for January added to fears of tightening. U.S. real treasury yields - or the returns investors can expect after inflation is taken into account - climbed to their highest levels in more than a year last week.

Despite remaining in negative territory, real yields have increased by over 40bps in January, their biggest monthly increase since 2013. This has hurt risk assets such as tech stocks and crypto, which appear less attractive to investors than safe-haven bonds. The slowing of the Fed’s monthly bonds purchases is also expected to exacerbate the move higher in real yields as the supply of government debt available to ordinary investors increases. All eyes are now on this week’s U.S. consumer price inflation numbers which will signal how rapidly the Fed will move in hiking rates and shrinking its balance sheet.