Mostly pegged to the US dollar, stablecoins have established themselves as important pillars in the emerging crypto ecosystem. They act as a base currency on centralized exchanges and as a dollar alternative on their decentralized counterparts (DEXes). A look at the current state of the stablecoin market.

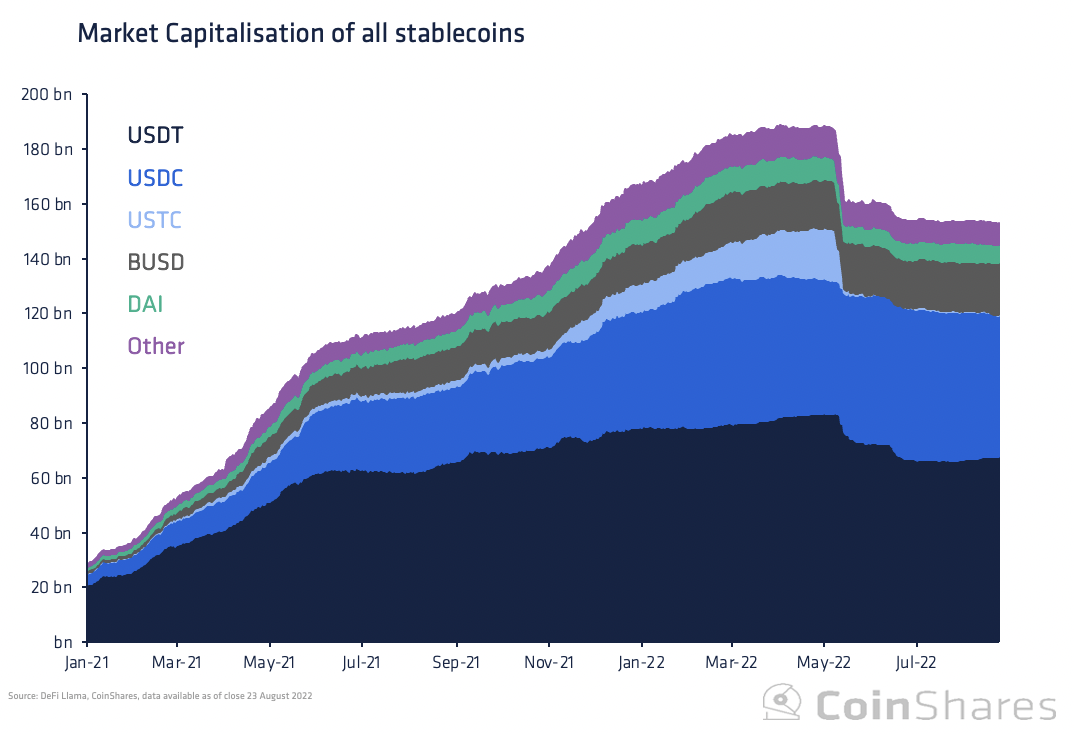

Centrally backed stablecoins are the leaders in the stablecoin market as they offer both scalable liquidity and strong stability. However, alternatives are still being experimented with. Since January 2021, stablecoins have grown 450% to $154bn and Tether, Circle and Binance account for over 90% of all issued stablecoins. In this report, we explore the purpose of stablecoins, the different types and risks and the current state of the market.

An emerging sub-sector

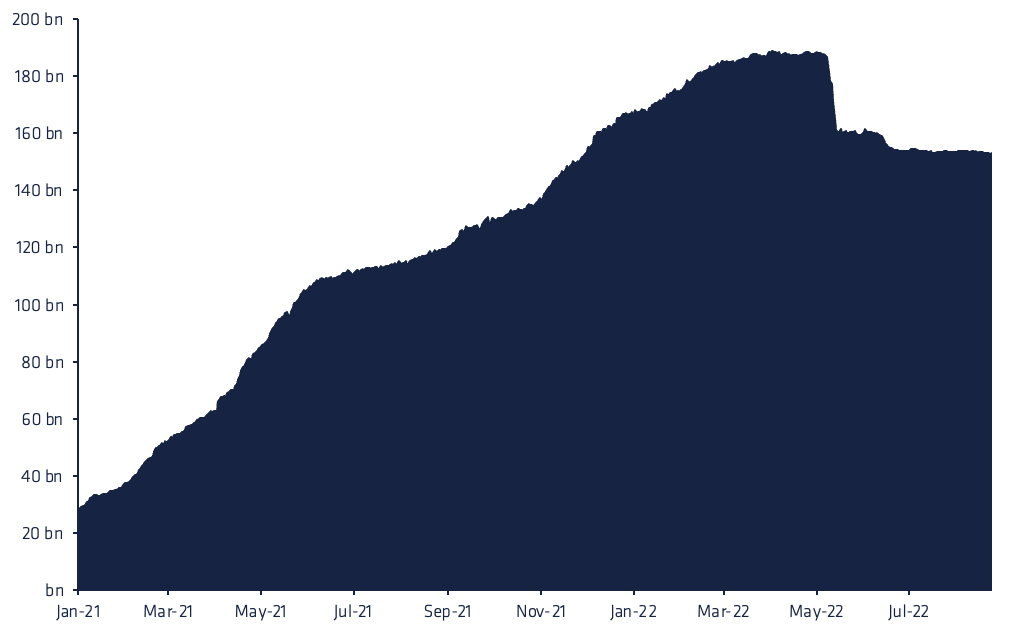

Stablecoins are a type of cryptocurrency that are pegged to a non-volatile asset (such as the US dollar). These stablecoins address the issues of inherent volatility risks within the crypto space and help to facilitate more predictable transactions. As evidenced below, stablecoins have become quite popular.

The sharp drop seen in May 2022 arose from the collapse of UST, a stablecoin native to the Terra blockchain which also collapsed as a result. The dissolution of the UST highlights that not all stablecoins are made equal and each type poses its own trade-offs and risks. There are three types of stablecoins:

- Fiat-backed stablecoins

- Collateralised debt positioned stablecoins

- Algorithmic stablecoins

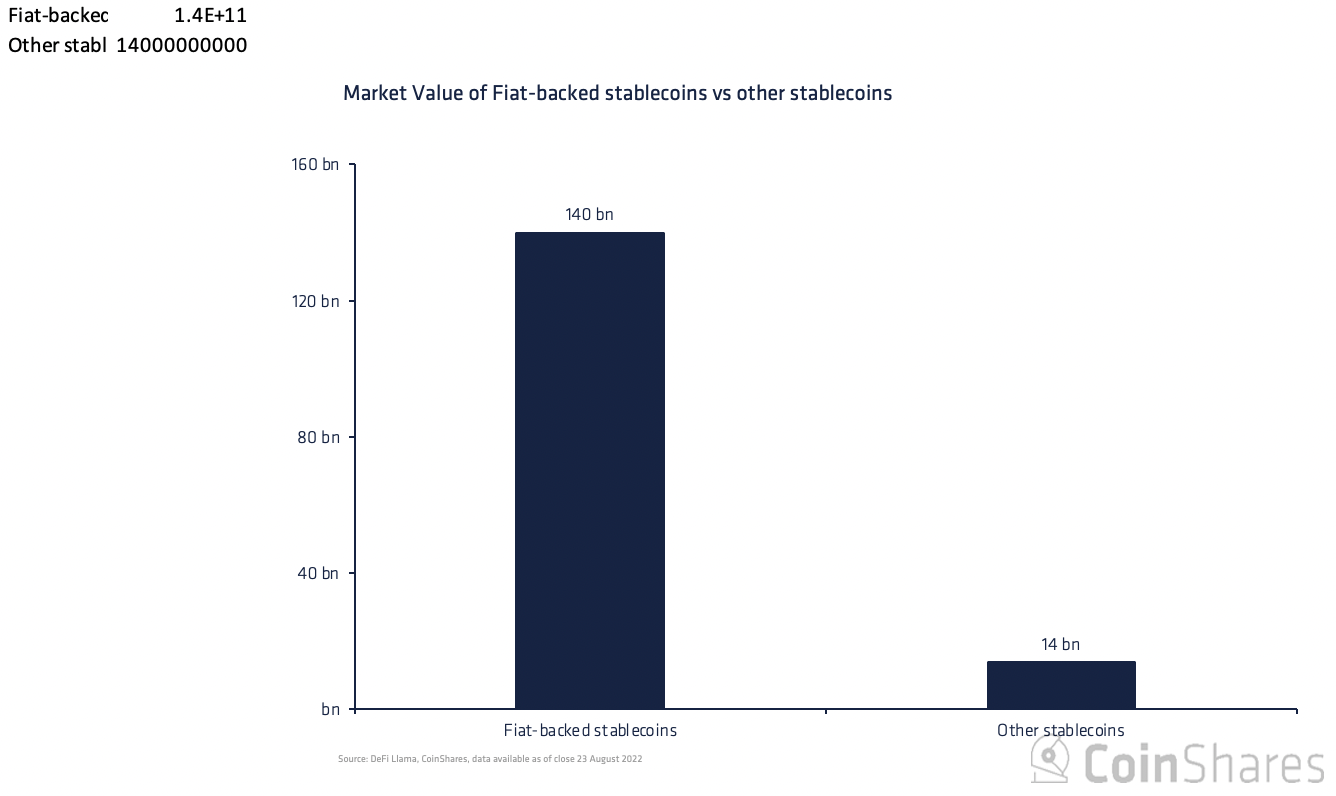

We examine these three types in greater detail below. Despite these issues and extra layers of trust, fiat-backed stablecoins are by far the most popular type on the market with over 90% market share.

Commonly used types of stablecoins

Fiat-backed stablecoins’ dominance is due to the ease at which stablecoins can be issued on-chain. The issuer receives deposits in a bank account and mints the equivalent amount on the chosen blockchain (in most cases Ethereum). We show the market share for fiat-based stablecoins below. The three most popular issuers are Circle, Tether and Binance, who account for ~98% of all fiat-backed stablecoins. Collateralised debt positioned (CDP) stablecoins differ from fiat-backed in the following ways:

- They are native to the blockchain (no physical bank account)

- They are overcollateralised

- They are backed by crypto-assets (including fiat-backed stablecoins)

As mentioned before, fiat-backed stablecoins work by depositing dollars into a bank account and the equivalent value is minted on-chain. CDPs are smart contracts that accept deposits on-chain and mint stablecoins that are less than the value of the deposited assets. The minted stablecoin is effectively a loan for the user and the deposits are the collateral used to take out this loan.

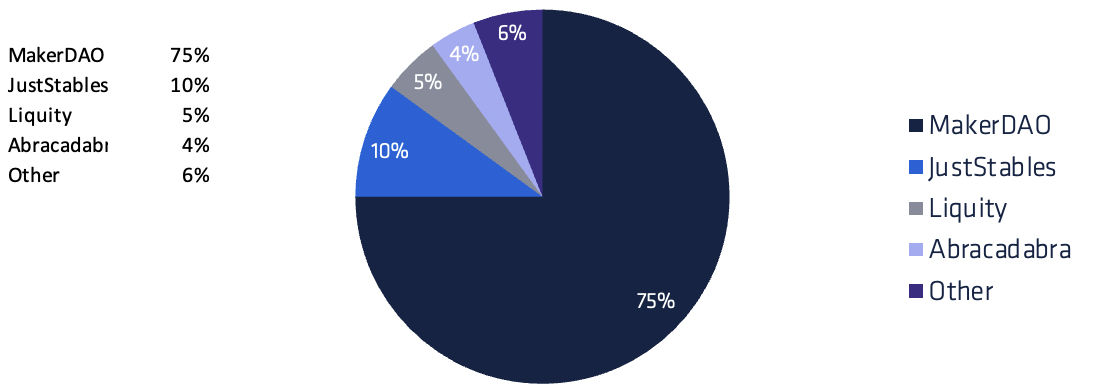

These deposits are crypto assets that have increased price volatility risk and hence loans are overcollateralised to compensate for this risk. Users can choose to return the stablecoin at any time in return for their deposited assets. The collateral ratio needed in return for CDP stablecoins depends on the crypto asset being deposited. For instance, an ETH deposit would require a 1.5 ETH deposit for every 1 ETH worth of stablecoin borrowed. Conversely, a USDC deposit that is less volatile would require a 1.25 USDC for every 1 USDC worth of stablecoin borrowed. Above we show a breakdown of the market share for the leading CDP protocols. MakerDAO is the clear leader as it pioneered the concept of CDPs in 2017. As of August 2022, the market value of all CDP stablecoins stood at ~$12bn.

Algorithmic stablecoins

Algorithmic stablecoins are a relatively new concept and distinct from the other two stablecoin types. Instead of relying on a reserve of assets, algo-stablecoins maintain their peg through algorithmic incentives or systems. For instance, rebasing was an early technique used to control the peg such that the supply of the stablecoin would change based on the price. A lower price would cause the supply to reduce and vice versa. However, this mechanism was unable to maintain stability over longer periods.

More modern algo-stablecoins utilise a two-token model to function with one token used to absorb the volatility of the stablecoin. The volatile token is burned to create the equivalent units of the stable token and vice versa. However, with the current implementations of algorithmic stablecoins, reliance on a volatile token to maintain the peg can be detrimental. This is because as the stablecoin loses its peg, the governance token also loses trust and value, so both coins rely on each other holding value otherwise both fall into a “death spiral” as has happened numerous times before.

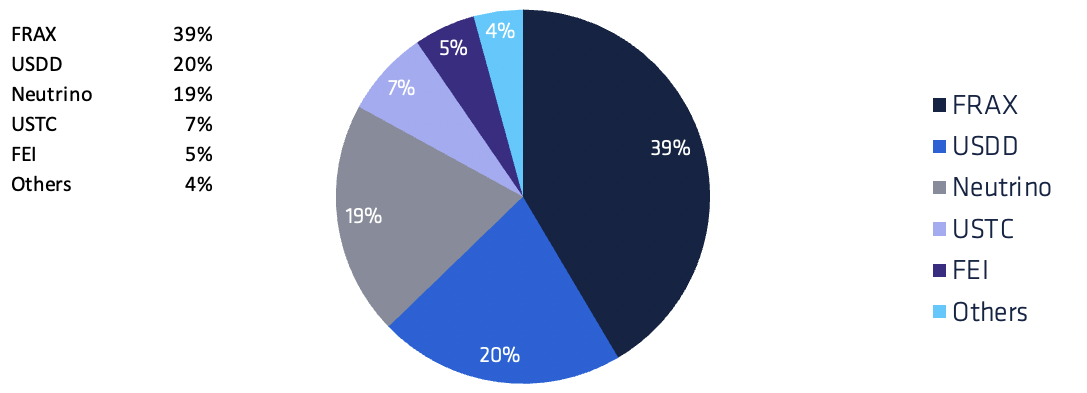

Generally, algo-stablecoins do not rely on collateral but there are also some that utilise a partial reserve model (partially backed by reserves, partially pegged by the algorithm). The specifications for all types of algo-stablecoins are still being tweaked, iterated upon, or completely redesigned. Above we show a breakdown of the market share for the leading algorithmic stablecoins. The algo-stablecoin market is valued at $3.7bn yet is more competitive than the others with the market leader, FRAX, opting for a partial reserve plus algorithmic model.

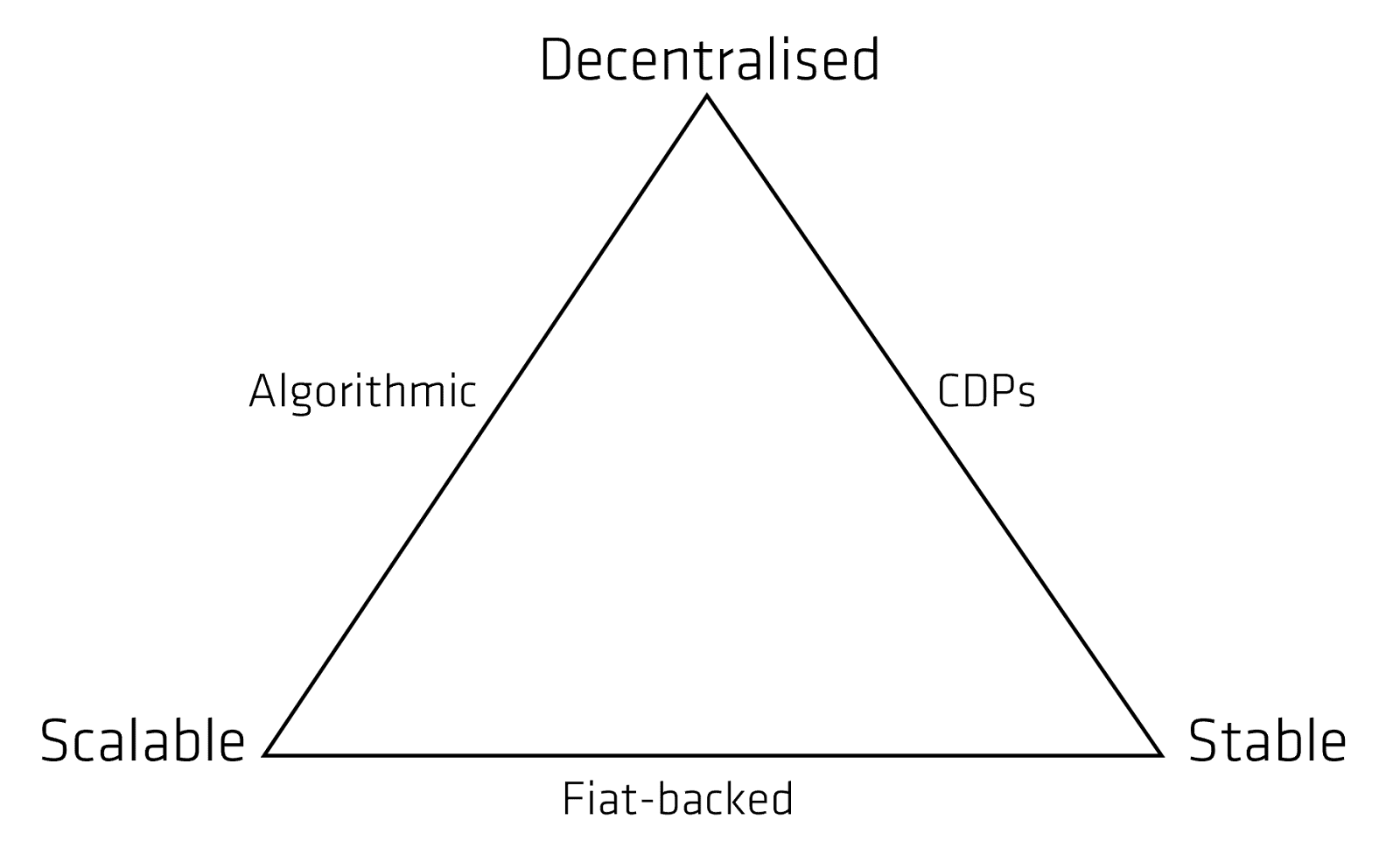

The Stablecoin Trilemma

The blockchain industry is known to love its trilemmas and stablecoins are no different. The end goal for the “ideal” stablecoin is to be stable, scalable and decentralised. So far, no stablecoin has been able to fulfil all three criteria. Fiat-backed stablecoins are scalable since it’s as easy as depositing dollars in a bank account. They’re also very stable as they’re essentially backed one-to-one by those same dollars in the bank. However, they are clearly not decentralised as there are only a few large, regulated entities which can mint these stablecoins, to begin with. Stablecoin issuers also have the ability to freeze these funds, preventing specific addresses from spending them.

On the other hand, CDPs can be decentralised so long as the crypto assets backing the borrowed stablecoins are decentralised as well. CDPs are also stable thanks to resilient risk management practices. Not every asset can be used as collateral, only those deemed pristine enough by the DAO. Furthermore, the mandated overcollateralization of these debt positions is the main factor driving this stability. However, requiring users to overcollateralise and borrow a fraction of their deposits is not inherently scalable.

Lastly, algorithmic stablecoins can possess both decentralisation and scalable properties. The algorithm dictates the mechanism so no one entity is in control - ideal for decentralisation. Likewise, the algorithms used tend to make it easy to create or burn the token allowing for increased scalability. Despite these dynamic capabilities, algo-stablecoins seem to continuously fail at maintaining a peg. A persistent peg for stablecoins may rely on faith more than a specific algorithm yet the search for the perfect algorithm continues.

State of the market

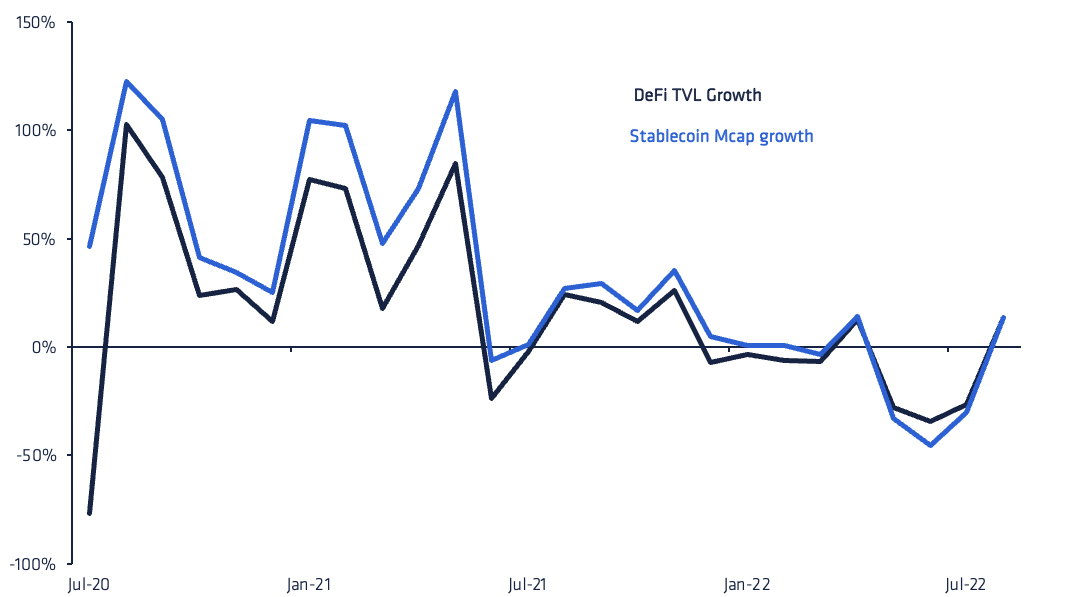

While stablecoins have become increasingly popular, the collapse of UST not only shrank the market size but also spurred redemptions in other stablecoins as well. Despite this implosion, the importance of stablecoins remains prominent across the entire ecosystem. We see below that the correlation between the growth of Total Value Locked (TVL) and the growth of stablecoins is persistently strong.

The above correlation analysis results in a correlation coefficient of 0.80. This strong link may be an important indicator moving forward for the health of the DeFi landscape. Zooming out a bit, with a first-mover’s advantage, USDT has long been the market leader although USDC has been gaining traction and is widely seen as more legitimate. We show a breakdown of this stablecoin growth below.

Year to date we see that market shares have not been that volatile though there has been some movement. Other stablecoins have lost ground while BUSD and USDC have materially gained. However, despite what most think, USDC's market share gain since the start of the year has mostly been due to Terra USD's demise as opposed to capturing it from USDT.

The integration of stablecoins within the traditional financial system provides easier access for users and adds to their legitimacy. In fact, on August 15th 2022, the US Federal Reserve’s governing board unveiled guidelines that will standardize applications for “master accounts” from institutions “with novel charters,” including “cryptocurrency custody banks and their trade associations.” What this means is that these stablecoin issuers now have another path to become further integrated into the traditional banking system.

CBDCs getting observerd closely

Another type of stablecoin being explored are Central bank digital currencies (CBDCs). Although there are not any CBDCs in use right now, proponents see them as an alternative solution to a digital currency tied to a fiat currency. The proposed differences between CBDCs and fiat-backed stablecoins are:

- The issuer is a central bank

- They’re partially backed by reserves and the faith of the government

- They would likely be built on a private blockchain for greater control

A CBDC built on a private chain would also fail to be decentralised but this is not a characteristic that central banks desire. China’s digital yuan has been in beta testing for a couple of years and is the most progressed CBDC among major economies. If its usage is mandated by a government, CBDCs pose a threat to stablecoins but also existing fiat dollars. Since central banks interface with banks and banks interface with the public, a CBDC could disrupt this two-tiered banking system and destabilise the financial system.

Another major concern surrounding CBDCs is privacy. The programming of CBDCs will allow for a level of control and transparency that is far more intrusive than any existing monetary system. Central banks will be able to change interest rates directly in savers’ accounts, monitor income and debt levels, as well as directly influence the spending of citizens. Given the controversial nature of this system, more research and legal clarity will likely be necessary for the fruition of any type of CBDC to proliferate within western democracies.

Conclusion

Stablecoins have found product-market-fit within the crypto industry. In fact, more projects continue to enter the stablecoin space with the fiat-backed entrant poundtoken getting the greenlight from the Isle of Man’s Financial Services Authority and Circle’s Euro Coin (EUROC). Algo stablecoins like USDN and USDD have also started to grow (though both have already depegged). Lastly, DeFi protocols Curve and Aave have both announced their intention to release CDP stablecoins in the near future. The appetite for stablecoins, from both the demand and supply side, is clearly as strong as ever. The total addressable market for stablecoins is trillions of dollars and given the already resounding success of these tokens, it is without a doubt crypto’s killer application.