In recent months, headlines about Bitcoin ETFs, institutional inflows, and new crypto initiatives by major US banks have become increasingly frequent. At first glance, this creates the impression that cryptocurrencies are on the verge of being fully integrated into the traditional banking system. A closer look, however, reveals a different picture: custody and trading services remain highly limited - and are typically reserved for a very small client segment.

Despite growing regulatory clarity and an expanding range of ETF products, most major US banks still do not offer broad-based crypto custody or active trading. Where services do exist, they are almost exclusively aimed at wealthy or institutional clients. For the mass market, access via banks remains the exception rather than the rule.

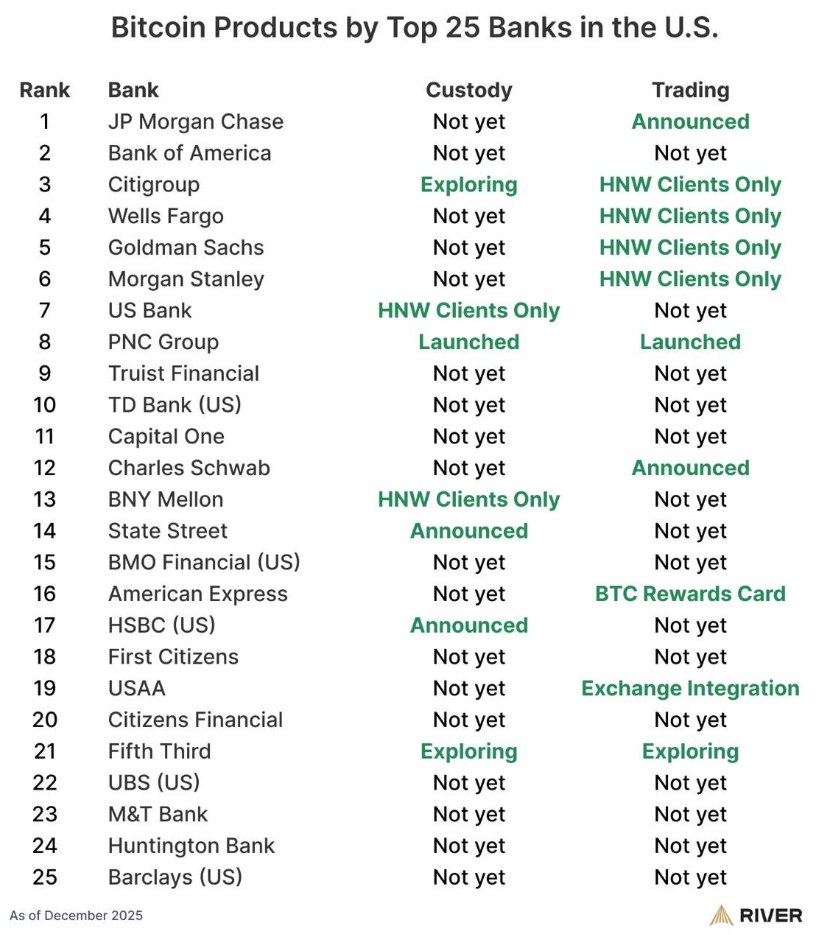

How many banks actually offer crypto custody?

An overview of the 25 largest US banks clearly illustrates how limited the current offering remains. Only a handful of institutions provide crypto custody at all, and even then usually in a restricted form. PNC is among the few banks that have already actively rolled out custody services. Other institutions such as Citi, Fifth Third, or State Street are still in the review or announcement phase. At many large banks - including JPMorgan, Bank of America, Wells Fargo, or Goldman Sachs - crypto custody is either not available at all or is restricted exclusively to ultra-high-net-worth clients. For retail customers, there is virtually no direct access in practice.

A similar picture emerges in crypto trading. While some banks have announced that they are exploring or planning related services, the user base remains very small. Citi, Wells Fargo, Goldman Sachs, and Morgan Stanley primarily provide crypto exposure through structured products or limited trading offerings - almost exclusively for very wealthy clients. Even at JPMorgan, which is publicly evaluating the option of offering direct crypto trading to institutional clients, these remain assessments rather than a broadly available product. For the majority of bank customers, direct trading of cryptocurrencies continues to sit outside the traditional banking offering.

ETFs create access - but not infrastructure

A key driver behind the perceived momentum is the launch of spot Bitcoin and Ethereum ETFs. While these products provide regulated exposure for institutional and retail investors, they do not replace custody or trading infrastructure within banks themselves. ETFs are balance-sheet investment products, not operational crypto services. Banks can offer them without having to deal with wallet custody, on-chain risks, or operational processes. This explains why ETF inflows are rising while custody and trading offerings show little growth.

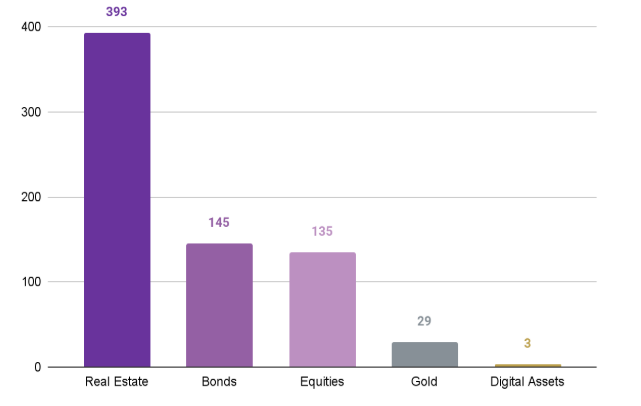

Even in a macroeconomic context, crypto remains small. The total cryptocurrency market currently stands at around USD 3 trillion. By comparison, real estate markets are estimated at USD 400 trillion, the global bond market at roughly USD 145 trillion, and gold at around USD 30 trillion.

Why banks are hesitant

The reluctance is not primarily technical in nature. Instead, regulatory uncertainties, liability issues, custody risks, and capital requirements play a central role. From a banking perspective, custody is significantly more complex than ETF distribution, as it involves operational responsibility and direct interaction with on-chain assets.

Despite growing attention, ETF success, and political debate, the crypto market has not yet reached the mainstream within the US banking system. Custody and trading are either not offered at all by most major banks or are limited to very wealthy clients. Current developments are less a sign of immediate mass adoption and more indicative of a gradual, cautious process of engagement.

raises billions through STRC: is the next Terra-Luna crash looming?")