After two years of caution and consolidation, 2025 has emerged as the most significant turning point for digital assets since the last bull cycle in 2021. In just six months, investor sentiment has swung decisively back in favour of the crypto sector.

Public listings are back on the calendar, institutional funds are deploying at scale, and venture capital flows have returned to levels last seen in early 2022. Far from a speculative resurgence, this capital is now flowing with far more discipline. Investors are backing infrastructure, compliance, custody and real-world blockchain applications. The result is a crypto market that is maturing visibly, aligning itself with institutional standards and capital market expectations.

The macro turnaround

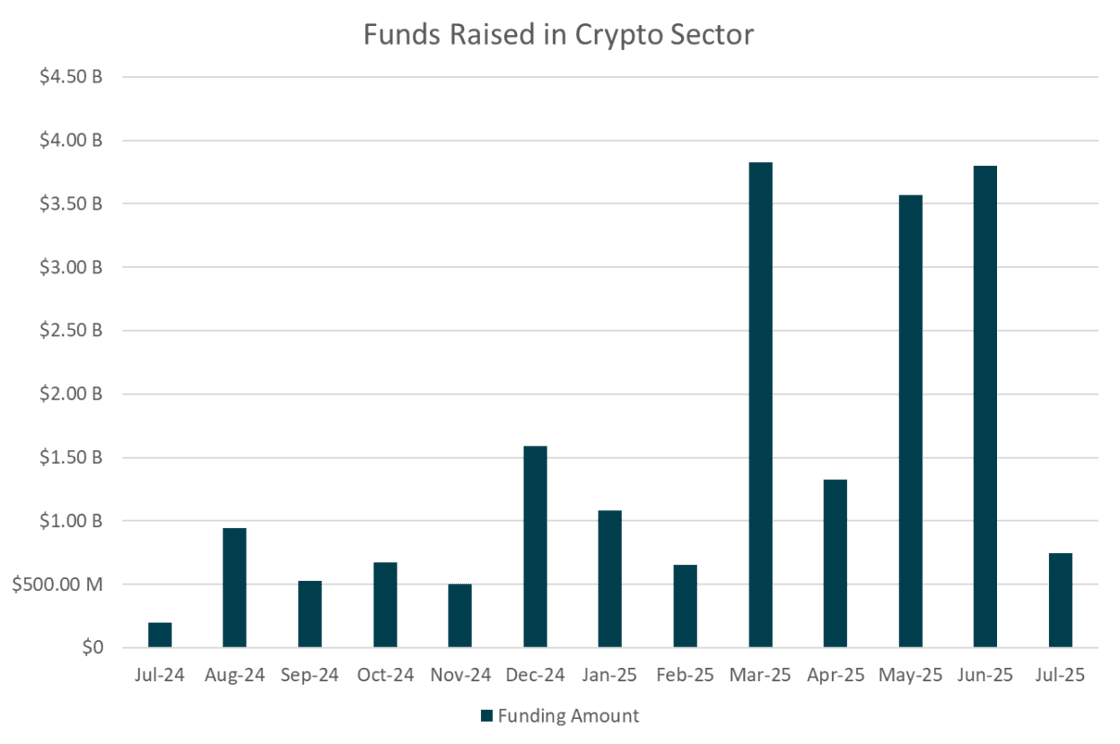

Venture capital investment in digital assets soared to 10.03 billion USD in the second quarter of 2025, marking a 100 percent increase year-on-year. June alone contributed 5.14 billion USD, the highest monthly figure since January 2022. The breakout moment came on 4 June when Circle Internet went public on the New York Stock Exchange. Its 1.1 billion USD IPO was upsized before launch and went on to close 168 percent higher on its first day. By the end of Day 2, shares had gained over 250 percent.

The listing served as a signal for the entire sector. Circle's success did not just reflect investor demand for stablecoins. It confirmed that companies with real revenue, regulatory alignment and global scale could once again find deep liquidity in the public markets.

In tandem with Circle's debut, the regulatory tide in the United States began to turn. The GENIUS Act, signed into law on 18 July, created a formal framework for stablecoin issuance, while the White House continued to push a pro-digital assets agenda. These developments triggered a wave of confidential S-1 filings from exchanges, custodians and infrastructure providers that had been waiting for clarity before going public.

Listings signal a structural shift

Since Circle’s listing, several other firms have followed. EToro, an investment and trading company based in Israel, raised an estimated 640 million USD on Nasdaq. Chime Financial, a FinTech company based in San Francisco, California, US completed a 700 million USD IPO, positioning itself as a neobank with a strong USDC savings product. Galaxy Digital completed its long-awaited uplist to Nasdaq, and CoreWeave, a GPU cloud provider powering blockchain and AI workloads, raised 250 million USD earlier in January.

Looking ahead, the IPO pipeline is expanding quickly. Bullish, Gemini and BitGo have already initiated filings or hired underwriters, with public prospectuses expected in September. OKX and FalconX are also preparing to list or raise pre-IPO capital. Ether Machine has opted for a SPAC listing targeting the fourth quarter with a 1.5 billion USD valuation.

Big money themes in private markets

Investor capital this year has been concentrated at the top end of the market. The focus is firmly on firms with validated revenues, operational compliance and strategic relevance. Strive Asset Management raised 750 million USD through a private placement. The capital is earmarked for strategic Bitcoin accumulation and includes warrants that could double the investment size. TwentyOneCapital followed with a 585 million USD raise, focused on Bitcoin basis trading and tokenization of real-world assets.

Securitize, known for its real-world asset tokenization platform, launched a new institutional crypto index fund in partnership with Mantle, which committed 400 million USD as the fund’s anchor investment. Digital Asset raised 135 million USD to grow the Canton Network, an interbank settlement system already supported by Goldman Sachs and DTCC.

Infrastructure remains a core theme. Auradine raised 153 million USD to fund its 3-nanometre mining chip line and AI-native network products. ZenMEV closed a 140 million USD Series A to build out a neutral block-builder ecosystem tailored for MEV resistance.

Sectoral conviction in H1 2025

Capital allocation in the first half of the year shows where investor confidence has concentrated. Trading and exchanges attracted the largest share by far, with 48 percent of total venture capital. Binance’s 2 billion USD strategic round and Bullish’s listing progress highlight the continued dominance of compliant centralised platforms.

DeFi and liquidity platforms received 15 percent, anchored by Kalshi’s 185 million USD raise following its regulatory clearance from the CFTC. Infrastructure and data availability followed with 12 percent. Auradine and Celestia ecosystem grants illustrate renewed faith in modular and bandwidth-efficient blockchain design. Custody and compliance players received 10 percent. BitGo and Fireblocks are drawing increased attention from institutional allocators who prioritise security and regulatory clarity.

AI-powered decentralised infrastructure claimed 8 percent, with ZenMEV and Bittensor validator networks leading the charge. These projects are at the intersection of compute, protocol design and intelligent routing. Even NFTs, gaming and decentralised social apps received 7 percent, with Magic Eden and Limit Break remaining active through acquisitions and strategic capital raises.

Regulation reshapes the map

The passage of the GENIUS Act has permanently changed the outlook for regulated stablecoin issuance in the United States. It provides reserve standards and compliance requirements, but more importantly, it removes the ambiguity that has long haunted both issuers and their banking partners.

March guidance from the SEC clarified that proof-of-work mining does not constitute securities issuance, giving listed miners like Riot and Marathon a clearer path forward. Meanwhile, regulators in Asia have taken a tougher stance on exchanges, prompting firms like OKX and Bybit to pursue US compliance as a long-term strategy.

What to expect in the second half

Momentum is expected to build sharply in the months ahead. Prospectuses from Bullish, Gemini and BitGo are likely to be published in September once SEC reviews are complete. These listings will test public market appetite for compliant infrastructure firms that generate predictable, SaaS-like revenues.

There is also increasing crossover between mining and AI infrastructure. Riot Platforms and Marathon Digital are preparing to spin off AI compute subsidiaries that leverage existing mining hardware as collateral for high-performance computing.

On the venture side, Paradigm, a16z Crypto and Binance Labs are all raising new funds exceeding 1 billion USD each. Their ability to deploy capital over the coming year will shape the direction of the next wave of crypto innovation.

Conclusion: A market that has grown up

This is not a speculative rally. It is a reorganisation of the digital asset space around long-term infrastructure, verifiable revenue and regulatory alignment.

The return of public listings confirms that crypto firms with compliant frameworks and institutional relevance can access the capital markets on competitive terms. Venture capital is flowing, but with far greater focus. Firms are no longer being funded for potential alone. They are being backed for execution, integration and measurable traction.

Crypto in 2025 is no longer pleading for mainstream relevance. It is earning it through scale, compliance and discipline. The second half of the year is poised to carry this momentum forward. And for the first time in years, digital assets are not just part of a tech cycle. They are helping to lead it.