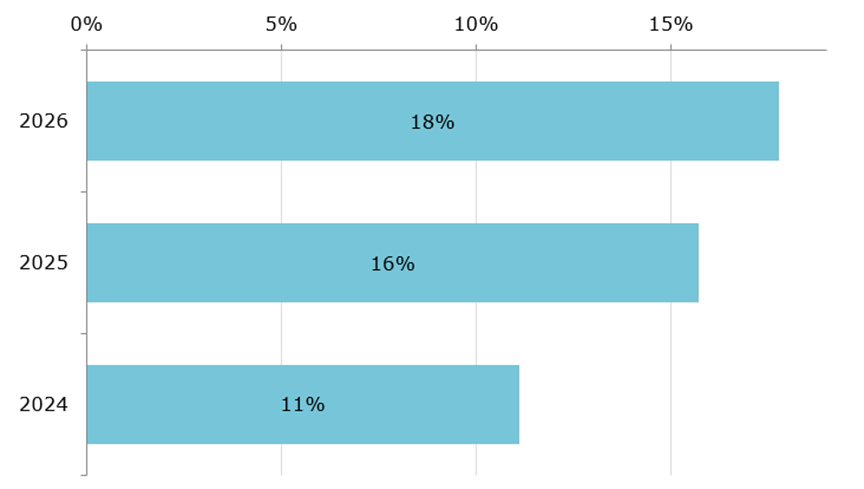

In 2026, 18 percent of the population hold crypto assets in Switzerland. That marks an increase of around two percentage points compared to the previous year. That is the finding of a new study by the Institute of Financial Services Zug (IFZ) and Luzerner Kantonalbank (LUKB).

The IFZ is the Institute of Financial Services Zug. It is a research unit of the Lucerne University of Applied Sciences and Arts, focused on retail banking. The LUKB is a Swiss cantonal bank, a public-law retail bank. It has offered its own crypto product since March 2024. For the survey published in June 2026, the authors questioned 1,772 people between February and March. The respondents came from German-, French- and Italian-speaking Switzerland. This continues a growth trend that still stood at 11 percent in 2024. However, the comparison figures come from studies with different commissioning parties and sample sizes. They therefore do not form a strictly comparable time series.

Crypto assets in Switzerland: adoption grows to 18 percent

In addition to current holders, a further 8 percent of respondents state that they previously invested in cryptocurrencies. Yet they no longer hold any positions. As a result, more than a quarter of the population has already gained experience with the asset class. Moreover, an estimated 140,000 new investors joined in the past year alone.

Returns furthermore reveal a clear difference between active and exited investors. While 57 percent of current holders report gains, the figure stands at 43 percent among former investors. Those who report gains apparently tend to stay invested. After all, the profit rate of active investors lies 14 percentage points above that of those who exited. Consequently, around 60 percent of today's holders plan to buy further crypto assets within the next two years. This high profit rate is likely to shape the continued willingness to buy as well.

The entry points correlate closely with the market phases. 26 percent of today's holders entered during the bull market of 2020 and 2021. A second concentration followed later during the ETF-driven rise in 2024 and 2025. Entries during bear markets, however, remain rare, which underlines the procyclical character of Swiss crypto adoption.

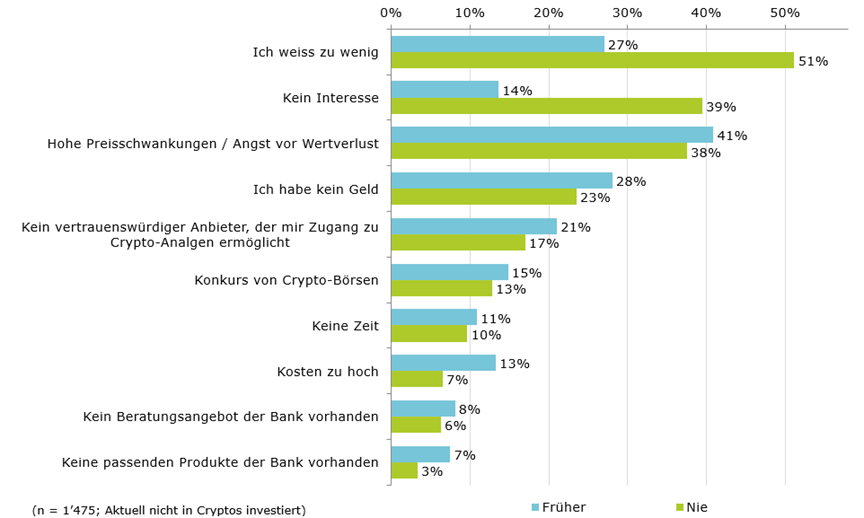

Knowledge gap as the main hurdle, not a lack of product offering

Among those who have never invested in cryptocurrencies, a single barrier dominates. 51 percent cite a lack of knowledge as the main hurdle, phrased as "I know too little." A lack of interest and high price volatility follow at a clear distance.

What is striking is what is barely mentioned. A lack of bank advice or an inadequate product offering plays only a minor role as a hurdle. This finding, however, turns the obvious banking logic on its head. Those who primarily launch new products do not thereby address the actual barrier facing non-investors. Because more than half of the abstainers name their own knowledge as the problem, the largest untapped market lies elsewhere. It consequently sits not in better products, but in understandable education. For retail banks, the strategic question therefore shifts away from the product range toward conveying basic knowledge.

How large this lever ultimately turns out depends on who is even willing to use a bank for entering crypto. Precisely here, the study shows considerable potential.

Up to 1 million potential advisory clients for Swiss banks

15 percent of respondents would "rather" or "very likely" use a crypto advisory offering from their bank. Extrapolated to the Swiss population, this corresponds to several hundred thousand up to around one million people. The figure comes from the study authors. Interest, however, varies strongly by generation. Gen Z reaches 27 percent, Millennials 21 percent, Gen X 9 percent and Baby Boomers 6 percent. The difference grows even sharper by experience. Current holders reach 34 percent, compared with 9 percent among those who have never invested. Advisory interest also grows with experience, which makes existing crypto clients the most obvious target group.

In competition with pure crypto platforms, banks hold a measurable advantage. In a decision experiment, respondents allocated a median of 31 percent of their gains to a cantonal bank. By comparison, only 21 percent went to Coinbase. This trust premium of around 10 percentage points proves robust against price. A doubling of the annual fees from 0.6 to 1.2 percent likewise barely influenced the investment decisions. Banks therefore do not have to compete on price. This trust advantage in particular could be scaled with targeted advice.

As a pioneer among the cantonal banks, the LUKB has offered trading and custody of cryptocurrencies since March 2024. Its partners are the crypto bank Sygnum, the custody provider Fireblocks and the trading platform Wyden. Other retail banks have followed suit. These include PostFinance, Swissquote and Valiant, as well as the cantonal banks of Zurich, Zug and Thurgau. Moreover, tailwind comes from regulation. Since 1 January 2026, the Crypto-Asset Reporting Framework has imposed a reporting obligation for Swiss crypto service providers. This rule tends to favor regulated providers.

Experience beats demographics as a predictor of investment

Which factors actually explain the willingness to invest, the authors examined with a regression analysis. At first, a purely demographic model based on age, gender and income explains only 17 percent of the variance. Supplemented by previous crypto experience and risk appetite, the explanatory power rises to 42 percent. The jump from 17 to 42 percent therefore shows that behavior and attitude weigh more heavily than the sociodemographic profile. The strongest single predictor is thus current crypto ownership, not age or income.

Two partial findings finally stand out. The frequently cited gender difference largely dissolves in the multivariate model, because it predominantly traces back to differing risk appetite. It is moreover notable that currently invested Baby Boomers show a higher willingness to reinvest than formerly invested Millennials. For banks, this consequently means one thing. It is not the age cohort that marks the relevant target group, but the level of experience.