Stablecoins have swiftly become the backbone of the crypto world, driving 50% of all on-chain activity. Bridging the gap between volatile crypto assets and fiat, they provide stability and a trusted medium for transactions.

Seamlessly integrated into platforms like Stripe and PayPal, stablecoins empower users to engage with crypto without technical know-how. With fast, low-cost payments, stablecoins are revolutionizing remittances and cross-border transactions, especially in regions facing currency challenges, like 70% of the African continent. Their unique appeal to crypto veterans and newcomers fuels widespread adoption, positioning them as a key driver in the evolution of finance.

What are stablecoins?

Stablecoins are crypto assets designed to maintain a stable value, usually pegged 1:1 to a commodity like gold or a fiat currency like the dollar. This design makes them ideal for everyday transactions and remittances.

- Fiat-collateralized: backed by fiat currencies, they represent the wholesome of this segment’s adoption. (Examples: Tether’s USDT and Circle’s USDC)

- Crypto-collateralized: backed by crypto, and to account for their volatility, they are often overcollateralized. (Example: MakerDAO’s DAI)

- Algorithmic: backed by algorithms and smart contracts to maintain their peg without any reserves. Instead, the peg is maintained by programmed mint and burn mechanisms. (Example: Aave’s GHO)

Stablecoins maintain a peg through specific collateralization strategies and market mechanisms designed to defend against price fluctuations.

Fiat-collateralized stablecoins

USDT and USDC are issued by centralized entities like Tether and Circle and are backed mostly by fiat reserves held in off-chain bank accounts. Tether invests around 15% of its reserves in assets like Bitcoin and secured loans to drive revenue while keeping most of its holdings in cash or equivalents to ensure it can meet redemptions, as outlined in its Transparency Report.

- Operates on a 1:1 model, where each token is backed by an equivalent amount of fiat or cash equivalent (e.g., 1 USDC = $1).

- Issuers can liquidate reserves when needed, ensuring sufficient collateral to cover all outstanding tokens and maintain stability.

- Their straightforward design makes them highly efficient for trading and as collateral in DeFi, where liquidity is essential.

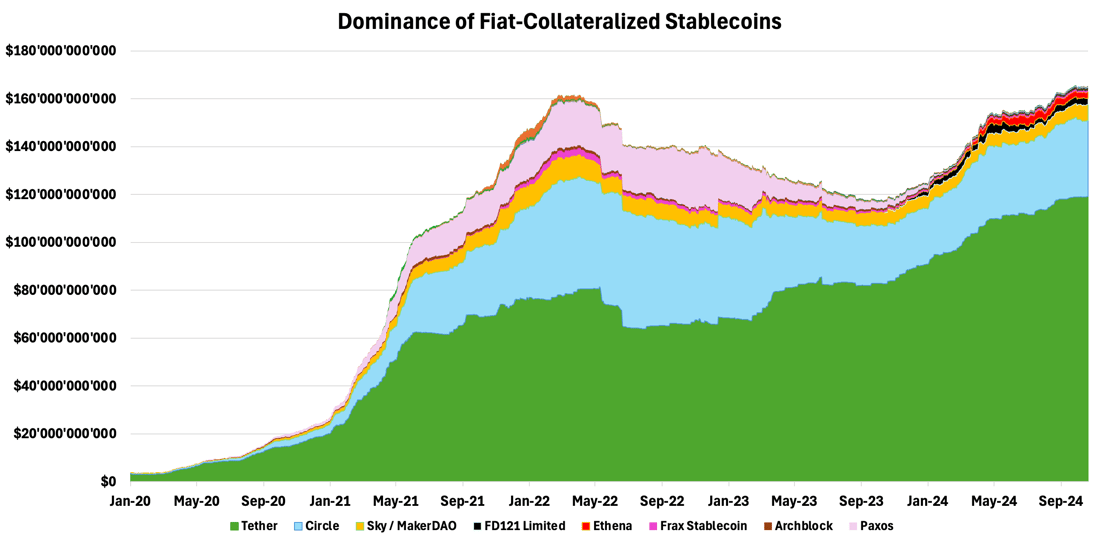

Thanks to their simplicity and reliability, fiat-backed stablecoins dominate the market—USDT and USDC alone boast over $140B, controlling over 90% of the market, as shown in Figure 1.

Crypto-collateralized stablecoins

Often operating without centralized oversight, they rely on smart contracts and crypto assets as collateral to maintain stability.

- Typically, over-collateralized means users must lock up more value in crypto than the stablecoins they mint, creating a buffer to ensure stability even in volatile markets.

- If collateral falls below the threshold, users forfeit it to the protocol, protecting the peg. Price oracles automatically trigger liquidations to maintain solvency.

- While decentralized, this model requires a robust system of smart contracts. Interactions between smart contracts introduce technological risks that must be carefully managed to prevent potential failures.

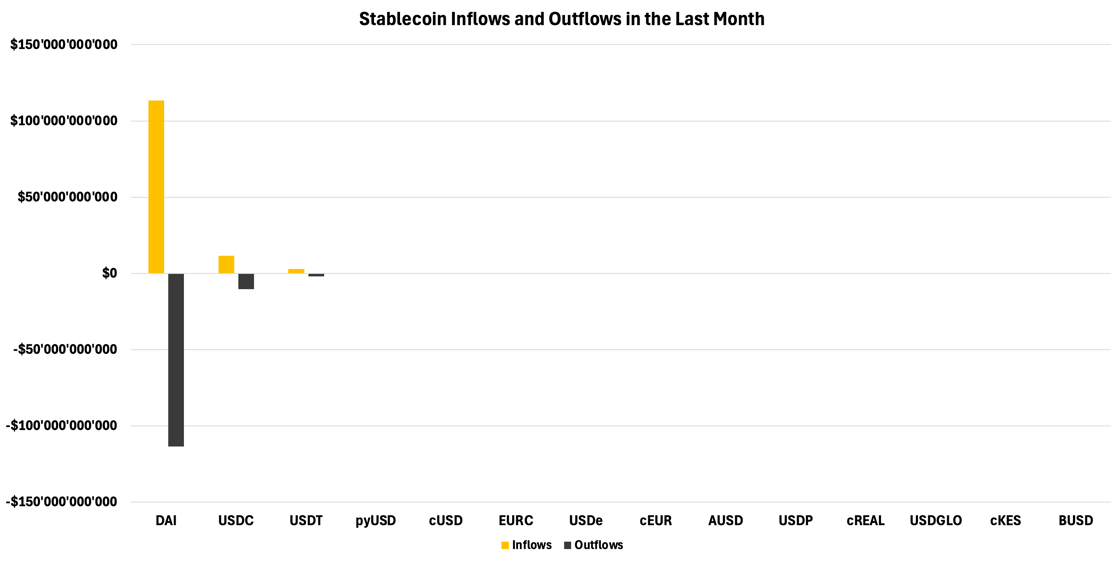

A prime example is MakerDAO's DAI, where users lock up ETH as over-collateralized debt. MakerDAO adjusts interest rates through on-chain governance, balancing supply and demand to maintain the peg. Due to its decentralized nature and internal management, DAI processed over $113B in inflows and outflows last month, as shown in Figure 2.

Algorithmic Stablecoins

Aiming to maintain stability without using collateral, they rely instead on smart contracts and supply adjustments.

- Protocols like Ampleforth (AMPL) target a CPI-adjusted dollar by adjusting token supply based on price changes. If the price rises above the peg, the supply increases; if it falls below, the supply contracts through a process called rebasing.

- Some designs, like UST, used a second "bond" token, LUNA, to expand and contract supply.

While innovative, these attempts have proven less reliable than collateral-backed models. Miscalculations or design flaws can lead to Black Swan events, as seen in the UST collapse.

Stablecoins on exchanges

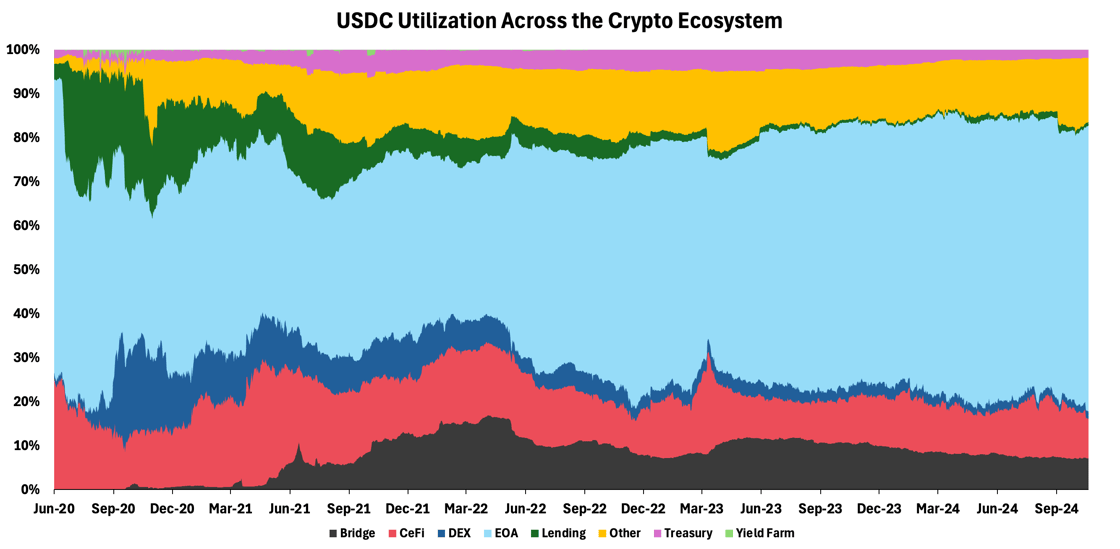

Due to their stability, stablecoins have become integral to crypto trading, serving as both a store of value and a medium of exchange. Analyzing the two largest fiat-collateralized stables by market cap echoes this pattern. For USDC, approximately 60% of its supply resides in Externally Owned Accounts (EOAs), with 11% in Centralized Finance (CeFi) platforms, as demonstrated in Figure 3.

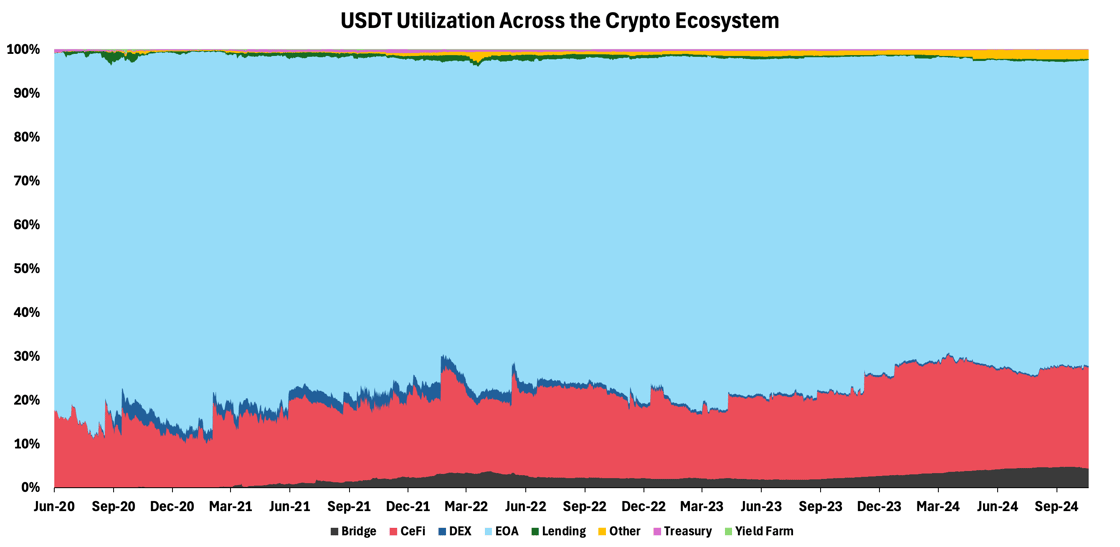

USDT shows an even stronger trend, with 70% in EOAs and 25% in CeFi platforms, as depicted below. USDT is more popular, as Tether is quicker to deploy to lesser-known blockchains and integrate with a broader swath of centralized platforms.

This distribution underscores stablecoins' key value: providing stability. EOAs (non-custodial wallets like Metamask and Phantom) often serve as havens where users convert crypto to stable assets. CeFi platforms, including major exchanges like Binance and Coinbase, offer similar conversion options but also facilitate cross-border transactions. This is particularly relevant as they support USDT's widespread presence on various networks, particularly Tron, which makes it a preferred choice for users in emerging economies across Latin America and Africa. This highlights stablecoins' dual role in both investment preservation and global financial accessibility.

Blockchain dollars in DeFi

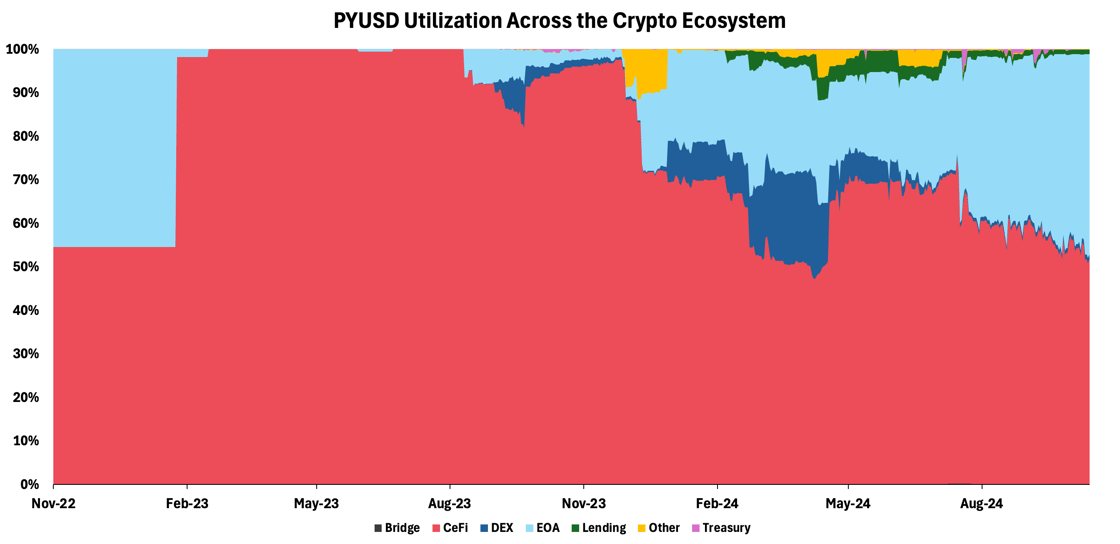

Fiat-collateralized stablecoins, like those from Circle and Tether, often have a limited presence in DeFi compared to decentralized alternatives such as Aave's GHO or Maker's DAI. This difference stems from the latter's incentive strategies, which typically involve distributing native protocol tokens (e.g., AAVE or MKR) to boost adoption. PayPal's PYUSD, however, stands out as an exception among centralized stablecoins.

In its push into the Solana ecosystem, PayPal partnered with Kamino Finance, offering yields of up to 17% annually on PYUSD deposits—significantly higher than competitors like USDC's 9% on Solana. This approach initially proved successful, driving PYUSD's market cap to nearly $1B, with almost 20% of its value distributed across decentralized exchanges (DEXs) as users leveraged it to generate yield by providing liquidity. Yet, when these incentives scaled back, the stablecoin’s market cap declined by almost 40% from the peak in August, highlighting the critical role of yield-driven strategies in shaping the adoption of stablecoin beyond the incumbents.

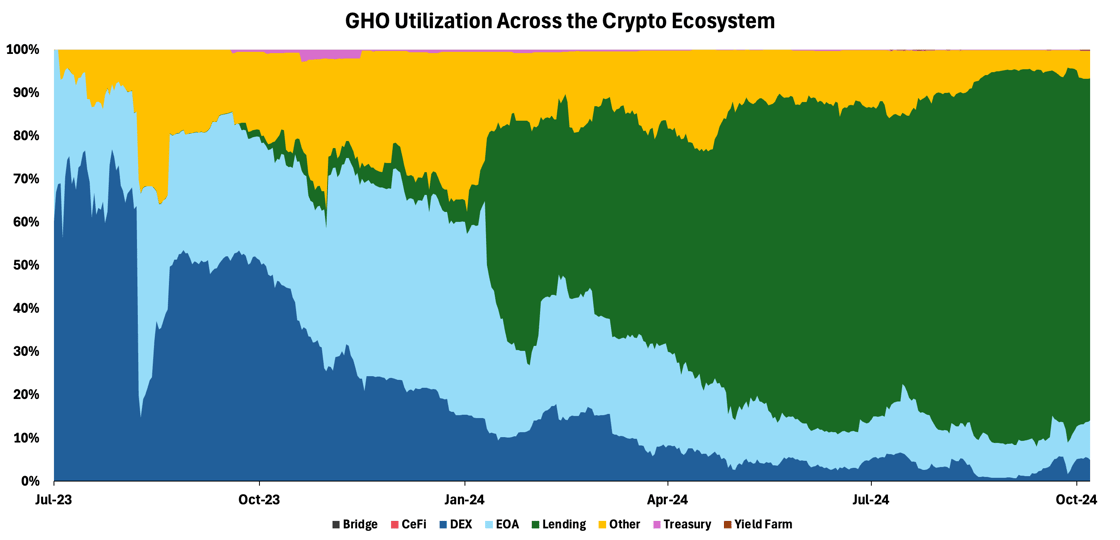

Similarly, GHO, Aave's over-collateralized stablecoin, gained significant traction in DeFi, largely due to Aave's strategic incentive structure. Notably, about 80% of GHO's supply is utilized in lending, with another 5% distributed across DEXs. This distribution aligns with Aave's strategy to position GHO at the core of its lending market, reinforcing the stablecoin's role in the broader DeFi ecosystem and driving its adoption.

To recap, stablecoins' general utilization makes up about 25% of DeFi, including DEXs, lending, and other types of financial engagement activities, as shown in Figure 7 below.

Remittance and payments

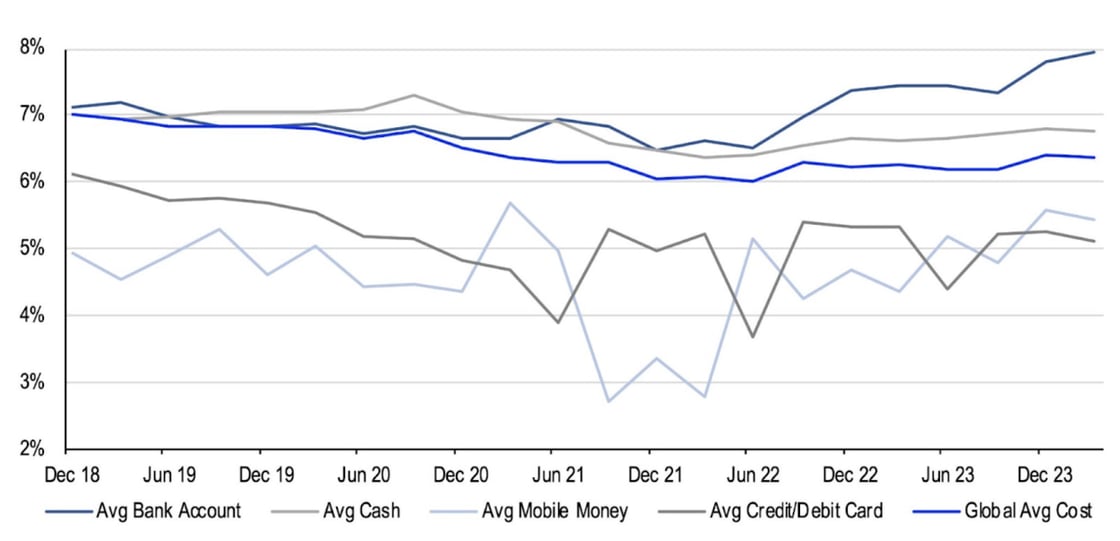

As seen below, stablecoins offer a compelling cost advantage for cross-border payments compared to traditional international money transfer services, which charge an average of 6% per transaction.

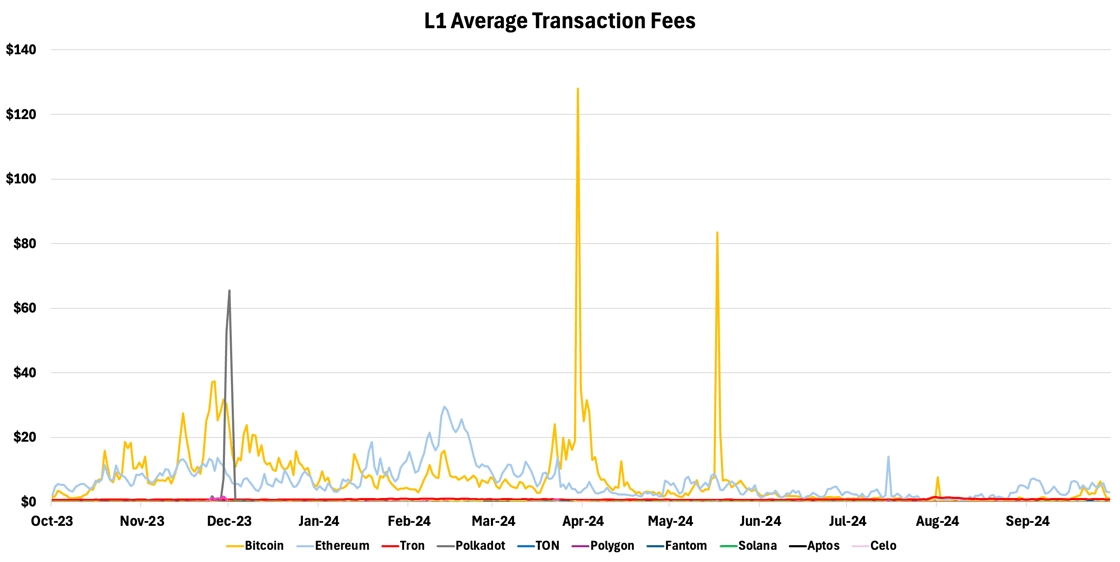

Transaction fees across blockchain networks vary significantly, ranging from fractions of a cent to several dollars—scalable blockchains like Solana, Fantom, Polygon, and TON offer average fees below one cent. In contrast, older-generation networks such as BNB, Tron, and Ethereum can incur fees from 10 cents to three dollars, as shown in Figure 9. However, Ethereum's ecosystem has evolved with the introduction of Layer 2 solutions. Platforms like Base, Arbitrum, and Optimism, operating atop Ethereum, have now drastically reduced transaction costs to less than a cent, especially after the Dencun upgrade. This development has significantly enhanced Ethereum's user cost efficiency.

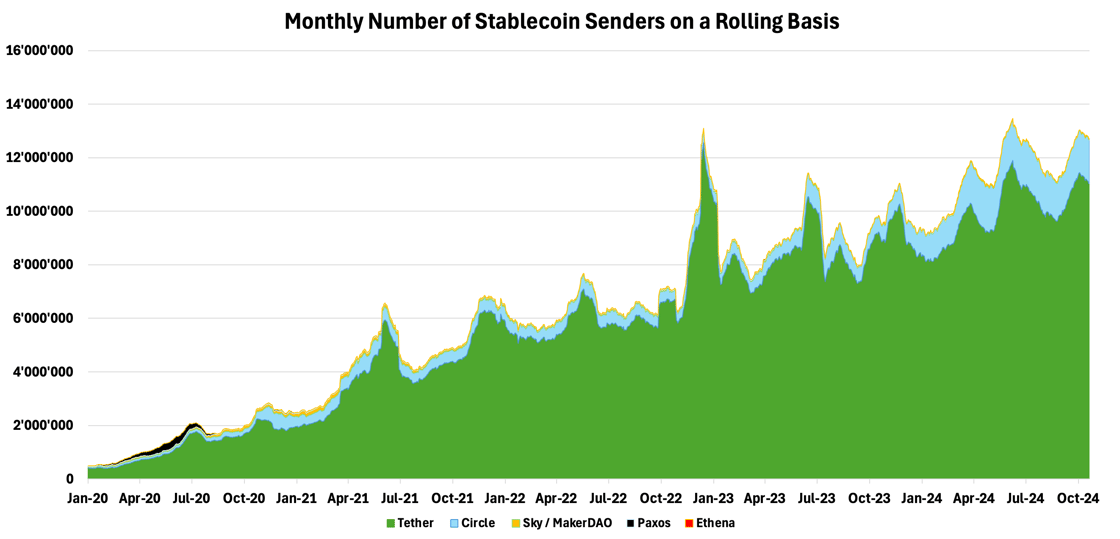

As seen, even with higher costs on networks like Ethereum, crypto transactions remain significantly cheaper than traditional payment systems. This cost-effectiveness is reflected in the unfazed growth of stablecoin usage, which has persisted through crypto's cyclical nature over the past four years. Despite experiencing a bull market from Q3 2020 to late 2021, followed by a bear market from 2022 to Q3 2023, the number of stablecoin senders has continued to rise unabated. Remarkably, monthly stablecoin senders have surged by nearly 600%, as shown below, from approximately 2.3M in October 2020 to 12M today, underscoring the enduring appeal and utility of stablecoins beyond the confines of the crypto ecosystem.

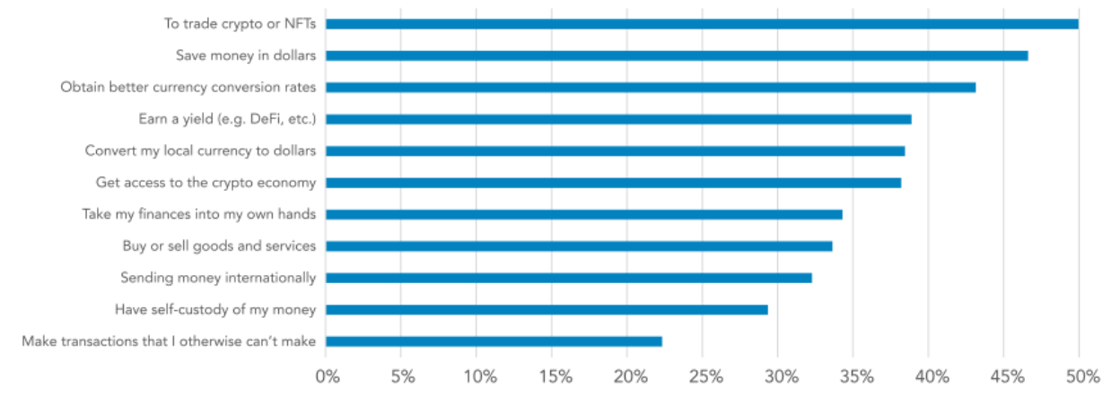

The evolving use of stablecoins is also evident in developing economies. A survey of 2,541 adults across Brazil, India, Indonesia, Nigeria, and Turkey, shows that 47% use stablecoins for better savings rates, 43% for improved currency conversion, and 37% to access dollars. Though limited in scope, this data suggests stablecoins are becoming versatile financial tools in emerging markets, addressing a range of economic needs beyond traditional crypto applications.