Circle Internet Group has received final approval from the US banking regulator OCC to establish Circle National Trust. The nationally supervised trust bank will provide custody for digital assets. It operates formally as First National Digital Currency Bank, N.A.

The OCC (Office of the Comptroller of the Currency) is the US federal agency that supervises nationally active banks. It also issues bank charters. A national trust bank charter permits fiduciary custody services, but no classic deposit business. This excludes checking or savings accounts and access to FDIC deposit insurance. Circle filed the application in June 2025. In December 2025, a conditional approval followed alongside four other crypto firms. Final clearance came after Circle met the preconditions. As a result, the CRCL share rose roughly 10 percent in pre-market trading. Meanwhile, USDC ranks fifth among all cryptocurrencies with a market capitalization of USD 73.21 billion.

What Circle National Trust may do as a custodian

Circle National Trust starts with a narrowly defined mandate. For now, the bank offers fiduciary custody services exclusively to Circle and its affiliated companies. However, the business plan approved by the OCC provides for a gradual expansion. Depending on demand, the trust bank can later offer custody services directly to a limited number of institutional clients. These are primarily banks and regulated derivatives organizations.

Structurally, the charter reaches considerably further. It is designed so that management of the USDC reserve could also fall under the bank in the future. As a result, reserve management for a stablecoin worth over USD 73 billion would move under direct federal supervision. At present, however, this remains only a future capability, not an immediate function. Precisely this option gives the charter its strategic depth.

Nevertheless, the limits of the charter remain clearly defined. Such a charter permits no deposit business and no access to FDIC deposit insurance. Circle therefore operates within an established framework. Around 60 other nationally supervised trust banks already fall under the OCC. The difference thus lies less in the type of bank than in the business purpose. This new trust bank holds digital rather than traditional assets in custody.

From conditional to final OCC approval

The final approval was no formality but the conclusion of a process lasting more than a year. Circle filed the charter application with the OCC in June 2025. In December 2025, the agency then issued a conditional approval, alongside four other crypto firms. In addition to Circle, Ripple also received a completely new charter with the Ripple National Trust Bank. Furthermore, the OCC let BitGo, Fidelity Digital Assets and Paxos convert existing state trust companies into nationally supervised trust banks.

Between conditional and final approval stood the fulfillment of the preconditions. Only afterward could Circle actually open the bank. A precedent from 2021 shows that this step is not a given. Originally, the OCC granted conditional trust bank charters to Anchorage Digital Bank, Paxos National Trust and Protego Trust Company. Of that trio, however, only Anchorage met the conditions and actually began operations. For Circle, the clearance therefore marks the formal entry into the US federal banking system.

"Federal oversight of our trust bank sets a new standard for the transparency, governance and scaling of our infrastructure and opens a new phase of adoption in which leading financial institutions can build on public blockchains with clarity and confidence." - Jeremy Allaire, Co-founder, Chairman and CEO, Circle

Traditional banks push back against the charter

The wave of charters for crypto firms faces resistance from the established banking industry. The Bank Policy Institute, an interest group of traditional banks, is examining legal action against the OCC charter practice. Additionally, further banking associations demand a restriction or overhaul of the approach. They cite financial stability, consumer protection and the legal scope of national trust charters.

The OCC itself, however, frames the opening as a competitive gain. Comptroller Jonathan Gould described new market participants in the federal banking sector as a benefit. In his view, they help consumers, the banking industry and the economy. Because they provide access to new products, services and sources of credit, they also foster a dynamic, competitive banking system. The conflict is likely to persist, especially since further applications sit in the queue.

Coinbase, Crypto.com's Foris DAX National Trust Bank, Stripe's subsidiary Bridge and the Brazilian neobank Nubank still await OCC decisions. Each has its own charter application pending. Consequently, the number of federally supervised crypto custodians could rise. For the established institutions, the focus rests less on a single competitor than on the principle. Through the trust charter, crypto firms are moving into the regulated banking system.

USDC cements its position in the stablecoin market

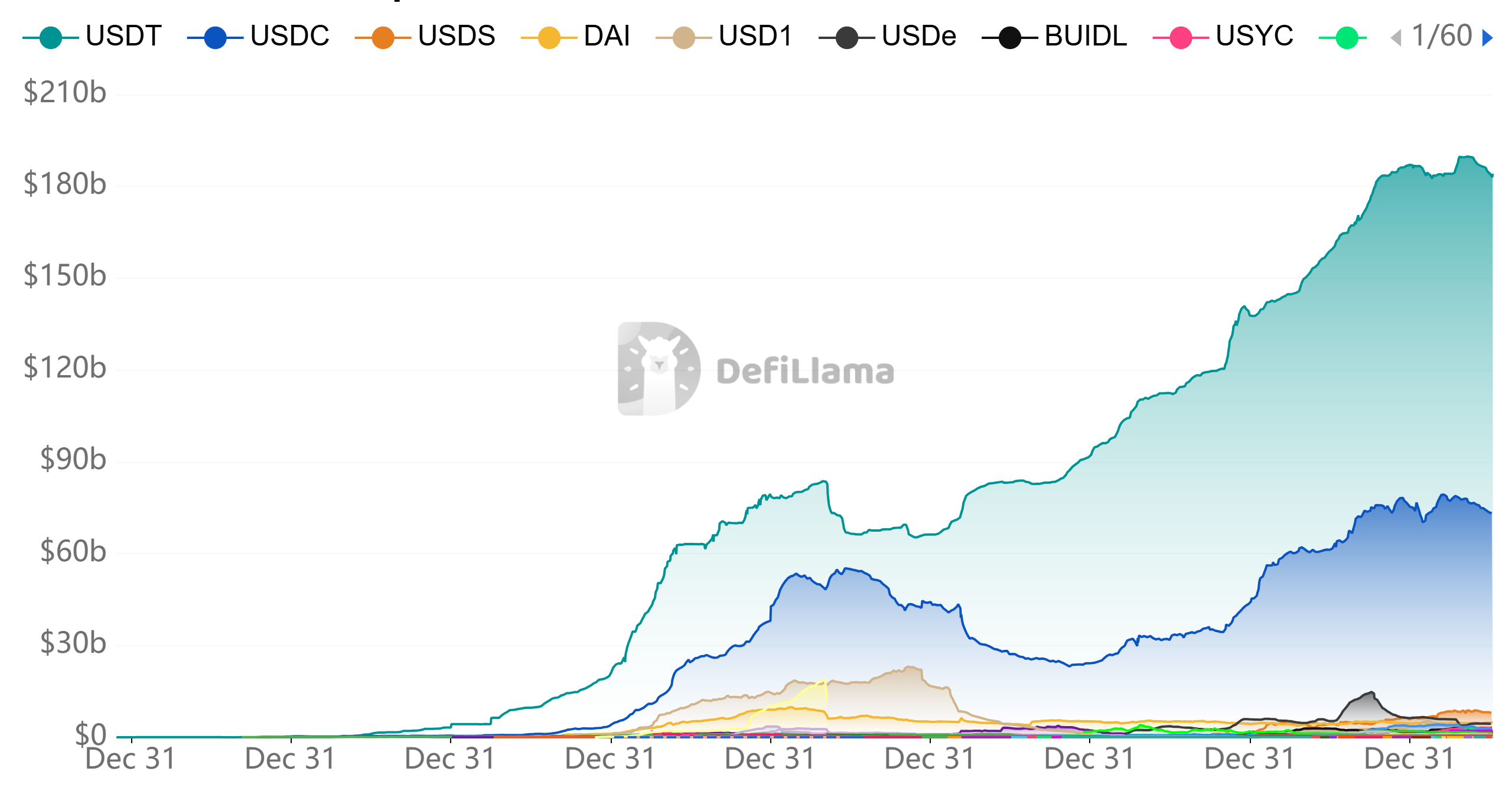

The regulatory news meets an already dominant market position. USDC reaches a market capitalization of USD 73.21 billion and ranks fifth among all cryptocurrencies. In June 2026, the stablecoin captured roughly USD 1.21 trillion of the adjusted transaction volume of USD 1.79 trillion. That corresponds to a market share of around 67 percent. In the first half of 2026, USDC's share stood at roughly 70 percent, compared with around 25 percent for Tether. By market capitalization, however, USDC still trails USDT by a wide margin.

The CRCL share reacted accordingly and gained roughly 10 percent pre-market. Structurally, two factors reinforce Circle's lead. On one hand, the GENIUS Act, the US federal law for payment stablecoins signed in July 2025, creates regulatory clarity. The OCC and FDIC are working on implementation in 2026. Its full effect takes hold by January 2027 at the latest. On the other hand, the trust bank charter underscores the issuer's regulatory profile.

At the same time, new competition arrives through a consortium of high-profile financial institutions. More than 100 companies, including Visa, Stripe, BNY, BlackRock and Mastercard, founded the Open Standard consortium two weeks ago. Together they announced the dollar stablecoin OpenUSD. The launch targets the second half of 2026, while Tether, Circle and PayPal deliberately remain on the sidelines.