The SEC has delayed its planned innovation exemption for tokenized stocks indefinitely. The framework, originally expected during the week of May 18, 2026, is now on hold after exchanges and market participants raised formal concerns.

An innovation exemption is a regulatory instrument. It allows market participants to operate under simplified requirements during an experimental phase. In concrete terms, it would have let crypto platforms offer tokenized stocks without fully registering as broker-dealers. SEC Chair Paul Atkins first announced the measure on April 21, 2026, at the Economic Club of Washington. It formed part of his ACT strategy of Advance, Clarify and Transform, which aims to make the United States the world's crypto hub. The SEC staff had previously completed and reviewed the draft. Tokenized stocks currently account for roughly USD 1.55 billion of the USD 34 billion tokenization market. As a result, this remains an early segment with a regulatory framework that is still unresolved.

Third-party tokens as the sticking point of the tokenized stocks SEC exemption

At the heart of the delay sits a single clause, not broad resistance to tokenization. The draft would have permitted trading in so-called third-party tokens. These are digital representations of company shares that issuers never consented to. This is precisely where the structural problem lies. Several share tokens of the same company could circulate in parallel on different blockchains. Therefore, managing dividends and voting rights would become more difficult for listed companies. For an issuer, it would consequently be hard to trace which tokens even represent its shares.

Exchanges and market participants therefore raised formal concerns before the framework could take effect. In addition, Citadel Securities and SIFMA warned against broad exemptions for tokenized stocks, particularly with weakened KYC and AML requirements. In their view, however, a parallel market threatened to emerge that would escape the control mechanisms of regulated securities trading. The agency continues to review the industry feedback, though no new date has been set. Consequently, it remains open whether the contested third-party clause will survive at all in a revised version.

Atkins' crypto agenda and the steps leading to the delay

Paul Atkins presented the innovation exemption on April 21, 2026, as a central building block of his tokenization agenda. The SEC Chair described it as a temporary bridge until the commission has worked out long-term rules. The announcement fit into his broader ACT strategy, with which he wants to open the US capital market step by step to crypto applications. At the Economic Club of Washington, he stated the ambition directly.

"We are on the verge of releasing what I call an 'innovation exemption', a clearly defined framework intended to allow market participants to begin trading tokenized securities on-chain in a compliant manner, while the commission works on long-term rules." - Paul Atkins, SEC Chair

Nevertheless, the delay marks no retreat from the agenda. It is more of a pause within an already well-advanced process. Initially, the agency had clarified in January 2026 that tokenizing a security does not change its regulatory classification. In March 2026, it approved the Nasdaq rules for tokenized stock trading, and the NYSE followed in April. Both rely on a tokenization pilot from the DTCC, which aims to test the settlement of digital securities within the existing market structure. The regulatory direction has thus long been set, only the latest sub-step is being delayed.

Meanwhile, market momentum continues. In early May 2026, Jump Trading and Securitize announced a partnership for trading tokenized stocks. Jump contributes the liquidity, while Securitize provides the infrastructure for issuing and managing the tokens. Such alliances show that the industry views the delay as a tactical interim step and is pushing ahead with its preparations undiminished.

What the exemption would have enabled and what is missing now

With the innovation exemption, crypto platforms could have offered tokenized stocks without going through full broker-dealer registration. Moreover, such tokens offer substantial advantages: faster settlement, fractional ownership, lower transaction costs and round-the-clock trading. Fractional denomination and continuous trading in particular address needs that conventional exchange operations, with their fixed trading hours, do not serve.

Commissioner Hester Peirce publicly defended the framework on May 21, 2026. She called it "limited in scope", because it covers only digital representations of existing securities and no synthetic tokens. Her statement came the day before the delay became known and therefore underscores the internal differences over the scope of the measure. Without a fixed date, however, the affected platforms continue to wait in limbo.

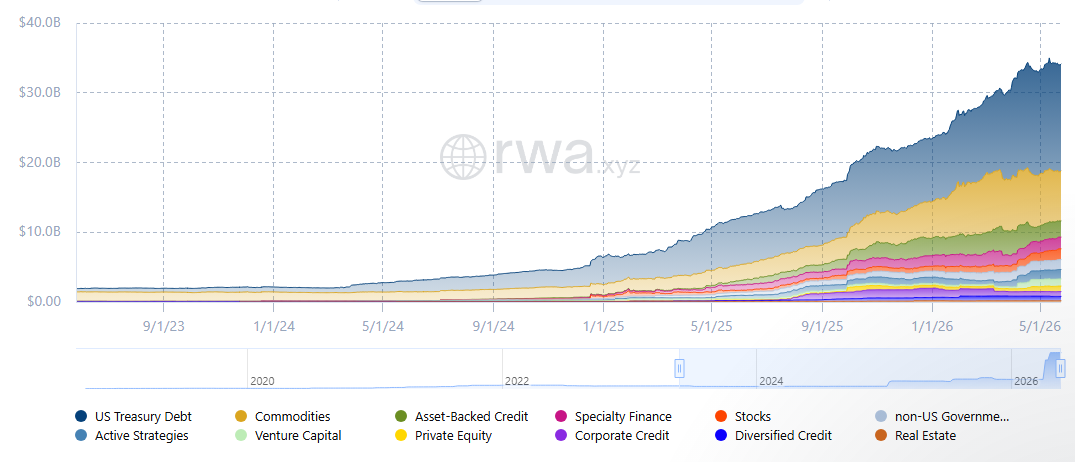

Tokenization market without regulatory safeguards

The market for tokenized real-world assets currently reaches around USD 34 billion. Tokenized stocks make up comparatively little of this, only about USD 1.55 billion, a small but growing share. Measured against established segments such as tokenized treasury products, the equity area therefore remains at an early stage. The regulatory standstill now slows its development even further. The missing exemption thus hits precisely the segment that has yet to make the leap from the pilot phase into broad trading.

Longer-term expectations nevertheless run high. Citibank originally projected in 2022, and McKinsey in 2024, that the tokenization market could reach a volume in the trillions by 2030. At the same time, the SEC had clarified in January 2026 that federal securities laws apply according to the economic substance of an instrument, regardless of its technical tokenization. The platforms operate exactly within this field of tension: the market potential is considerable, yet the binding framework for tokenized stocks is still missing at the SEC. Until a new date is set, the bridge between an ambitious agenda and compliant trading remains unfinished.