Bitcoin has dropped below the 73,000 USD mark. The decline amounts to 3.4 percent within 24 hours and 6.3 percent on a weekly basis. At the same time, Bitcoin ETF outflows hit 527.84 million USD at BlackRock's IBIT. Specifically, this marks the second-largest daily outflow since the fund's January 2024 launch.

IBIT is an exchange-traded fund offered by asset manager BlackRock. The product gives institutional and retail investors direct exposure to Bitcoin without requiring their own wallet or custody solution. Moreover, with roughly 59 billion USD in assets under management, the fund ranks among the largest ETF offerings worldwide. IBIT originally launched in January 2024, when the SEC first approved US spot Bitcoin ETFs. Since then, the fund has channelled substantial institutional capital into the crypto market. Furthermore, it now holds approximately four percent of the total Bitcoin supply in circulation. Overall, all eleven US spot Bitcoin ETFs recorded combined net outflows of 733.43 million USD on Wednesday. This marks the largest single-day outflow since late January 2026. In addition, cumulative outflows since mid-May now exceed two billion USD.

New US airstrikes and macro pressure trigger risk-off wave

Two external factors drove the sell-off, in addition to broader market weakness. First, US Central Command conducted airstrikes on May 25 and 26 against an Iranian military facility near the Strait of Hormuz. During the operation, the command shot down four Iranian drones. At the same time, the US imposed fresh sanctions on the Iranian "Persian Gulf Strait Authority". Iran subsequently accused the US of violating the existing ceasefire. Observers have considered that ceasefire fragile for weeks. Specifically, a dispute over the wording on Iran's nuclear programme has so far blocked any long-term agreement. Moreover, the Strait of Hormuz is one of the most important transit routes for crude oil worldwide. As a result, military escalations in the region feed directly into global energy prices.

In addition, a difficult macroeconomic environment is weighing on risk appetite across global markets. Rising US Treasury yields and persistent inflation concerns are reducing the likelihood of near-term Federal Reserve rate cuts. Consequently, risk assets are coming under additional pressure. Asian equity markets lost 1.7 percent, while the MSCI All Country World Index slipped only 0.4 percent. Futures on the S&P 500 and Nasdaq 100 also traded in negative territory. Meanwhile, oil prices climbed as an immediate reaction to the geopolitical escalation. Bitcoin ultimately responded as a correlated risk asset. Specifically, the price fell 3.4 percent within 24 hours and 6.3 percent over the week.

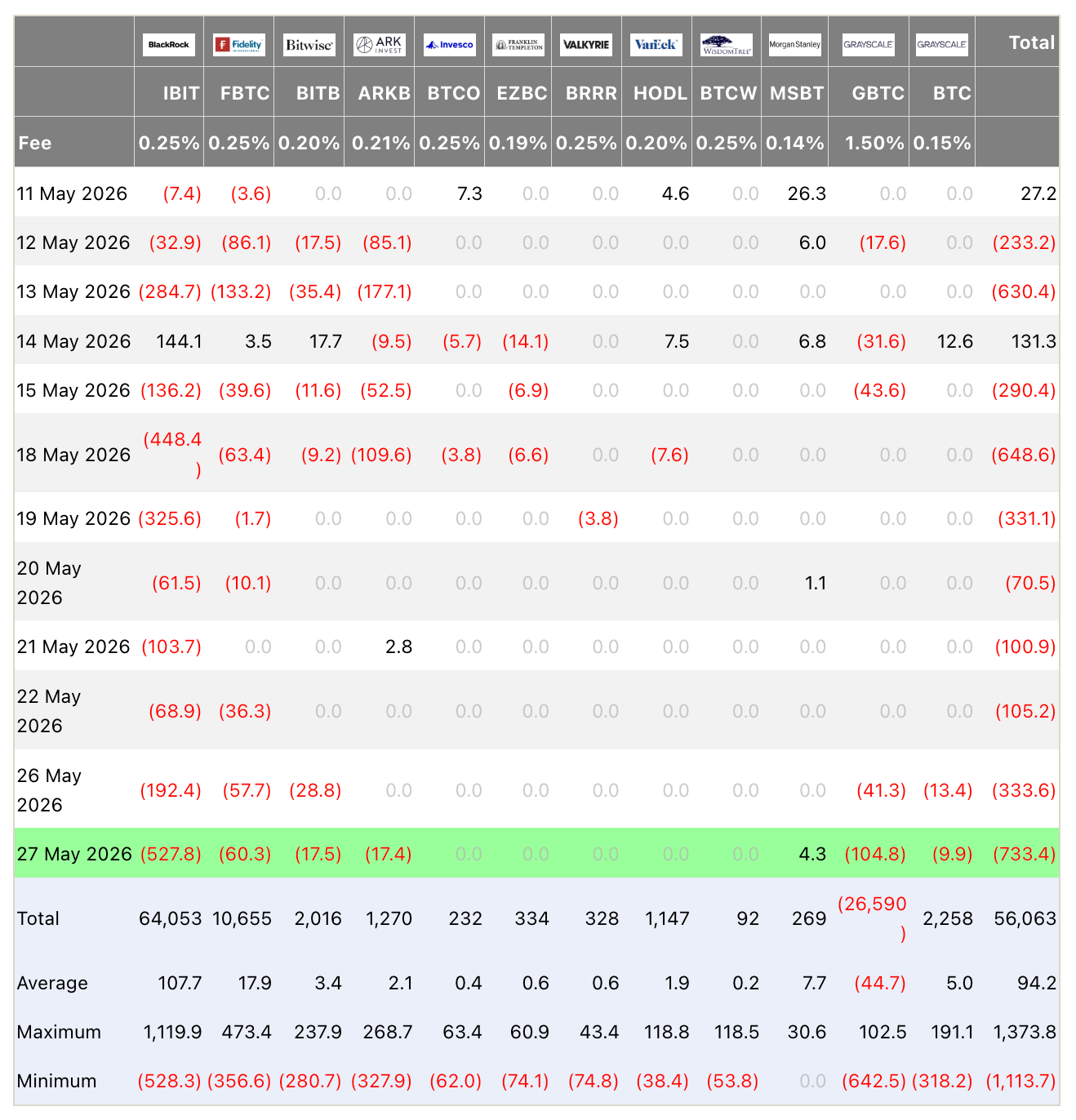

Bitcoin ETF outflows approach record territory

The net outflow at IBIT of 527.84 million USD marks the second-largest daily outflow since the fund's launch. The previous record dates from January 28, 2026, when outflows reached roughly 528.3 million USD. As a result, the current event fell short of the all-time high by only around 500,000 USD. This represents a difference of less than 0.1 percent. Notably, both peak readings coincided with pronounced correction phases in the Bitcoin spot market.

In addition to IBIT, other large products recorded significant outflows. Grayscale's GBTC lost 104.76 million USD, while Fidelity's FBTC shed another 60.30 million USD. In total, the eleven US spot Bitcoin ETFs registered a combined daily outflow of 733.43 million USD. Notably, this is the largest figure since late January 2026. Consequently, the products have collectively lost more than two billion USD in capital since mid-May.

The pattern points less to a loss of confidence in Bitcoin as an asset class. Instead, it points to institutional portfolio rotation in a risk-off environment. The concentration of outflows at IBIT, the product preferred by professional investors, supports this reading. Furthermore, the timing aligns with the geopolitical shock and rising Treasury yields. Consequently, the macro-driven dynamic stands out clearly. Therefore, this represents an asset allocation phenomenon rather than a product-specific issue.

Block trade the day before signalled institutional positioning

In fact, the institutional position reduction had already become visible the day before. On Tuesday, a single investor sold IBIT shares worth 1.29 billion USD via a dark pool block trade. Specifically, this refers to an off-exchange large order executed outside the regular order book. Such transactions allow institutional players to reshuffle large positions without moving the market price. Notably, the size of the trade had already signalled that at least one major professional investor was sharply reducing its exposure.

Nevertheless, the net daily outflow at IBIT on Tuesday came in at a relatively moderate 192.44 million USD. In parallel, capital continued to flow into the fund and offset part of the selling. Only on the following day did the situation escalate to 527.84 million USD in net outflows. Specifically, the offsetting buyers also stepped back at that point. Ultimately, the pattern suggests a coordinated institutional retreat. Furthermore, it spanned at least two trading days and coincided with the escalation in the Persian Gulf.

Nearly one billion USD in derivatives liquidations within 24 hours

The spot market pressure extended into a broad chain reaction across the derivatives market. Within 24 hours, exchanges liquidated positions worth a total of 958.8 million USD across 167,706 traders. Notably, long positions accounted for 897 million USD, or 93 percent of the total. Short positions, by contrast, lost only 61 million USD. For Bitcoin specifically, liquidations amounted to 386 million USD. The single largest liquidation hit a BTC position worth 15.34 million USD on the derivatives exchange Hyperliquid.

Ether lost 4.2 percent to 1,976 USD and 7.7 percent over the week, with liquidations of 246 million USD. Furthermore, the larger altcoins declined sharply. Solana fell 3.5 percent to 80.57 USD, XRP dropped 3.6 percent to 1.28 USD, and Dogecoin slipped 3.2 percent. Overall, the distribution reflects a broad-based capitulation of leveraged long positions. In addition, these positions had been aligned with a sustained uptrend. Consequently, the dominance of long liquidations at 93 percent shows how one-sided the speculative positioning had become just before the correction.