A monthly review of what's happening in the crypto markets enriched with institutional research on the most important topics in the industry in cooperation with the Swiss digital asset specialist, 21Shares AG.

The price performance of the markets this month was progressive in comparison to February. The market cap of the whole crypto industry started hovering over $2T shortly before March came to an end. This month also witnessed crypto’s highest correlation with tech stocks, as seen in the chart below. There have been a lot of developments in the Ethereum network, riling up hype in its ecosystem. One of the biggest moves is the long-anticipated proof-of-stake migration (merge), which has shown a visible impact on Ethereum’s price performance.

Use of crypto during the war

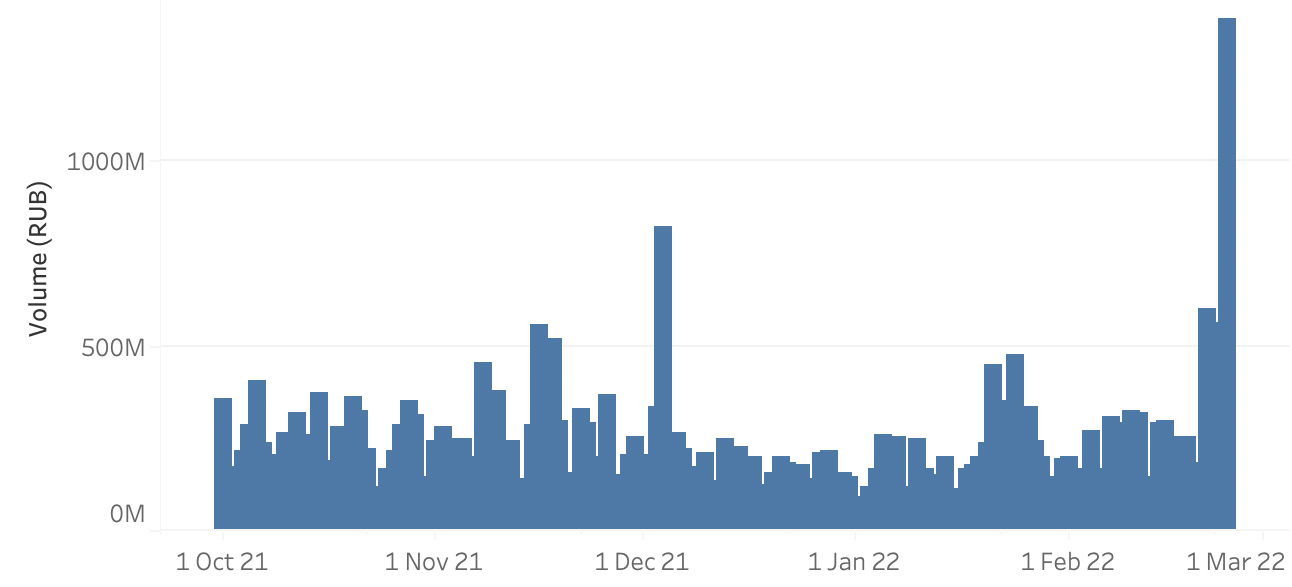

March started with the cancellation of what would have been the world’s first state-run airdrop. The Ukrainian government decided to withdraw from issuing fungible tokens, announcing it would drop some NFTs to support the Ukrainian army. Finally on March 30, the first sale of Ukraine’s “Museum of War'' was made. The Ukrainian government partnered with Fair.xyz, a one-stop shop for NFTs, to build a timeline of collages and images documenting the Russian invasion of Ukraine sold as tokens on the Ethereum blockchain.

Moreover, Ukraine’s deputy minister of digital transformation said that crypto is playing a significant role in Ukraine’s defense. Although the amount so far ($71.8M) of donations made in crypto is just a small fraction in comparison to those made in fiat, Ukrainian authorities highlighted that the speed and ease of use of crypto transactions are what really helped the war-ridden nation and even though the amount was not as high as fiat donations compared to how many people or organizations are already using cryptocurrencies, it showed the power enabled by blockchain technology.

Imposed sanctions on Russia

But the war not only played an important role in the country itselfe. It also had many influences on the rest of the world who stated a lot of sanctions against the war power Russia. On March 7, Coinbase announced that it had blocked more than 25,000 wallet addresses linked to Russian individuals or entities who are suspected of having engaged in illicit activity. Moreover, two fundamental pieces of the Ethereum ecosystem, Infura and MetaMask, are restricting access to users in certain geographical areas, shying away from giving any specific details.

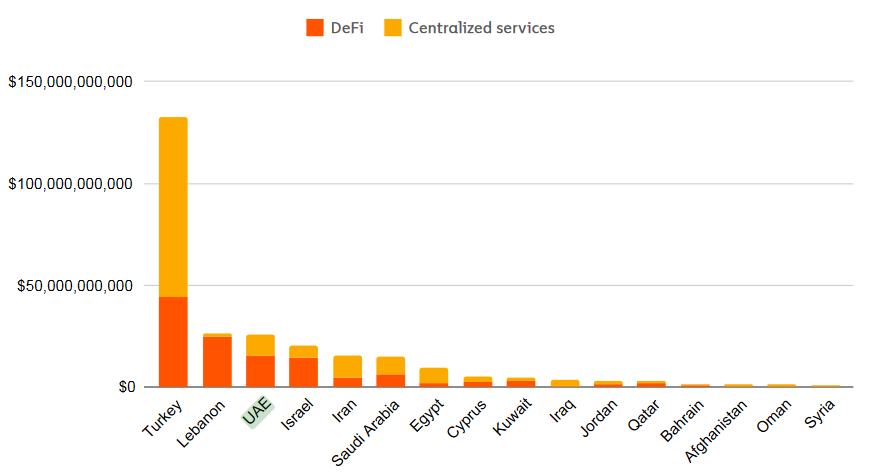

On March 11, as the invasion entered its fourth week, news came out that high-net-worth Russians attempted to liquidate billions of dollars of crypto last week through Dubai crypto companies. A week after, Michael Chobanian, founder of KUNA Exchange, told US senators in a hearing about the role crypto-assets play in the pursuit of illicit finance that there are a lot of Russians in and outside Russia who rely heavily on crypto. Chobanian denied that the Russian government could evade sanctions using crypto-assets, explaining that it’s virtually impossible to transfer large amounts of money from fiat to crypto-assets.

In a conference held on March 24, Russia’s Duma Committee on energy chair revealed the country’s intentions to be more lenient with its allies, selling its oil to Turkey and China for Lira, Yuan, and Bitcoin. Whereas, for countries imposing sanctions on Russia, that would be either gold or rubles. With the UK and the US already holding a ban on Russian oil, the EU is left in a pickle. Russian oil fields supply Europe with a quarter of its oil, which gives reason for its division on the fueled matter.

CBDC's getting more relevance

On March 15, it was reported that Saudi Arabia is considering accepting Yuan when selling oil to Chinese customers as oil surges amid the Russo-Ukrainian conflict. This foreshadows the scenario we have long anticipated at 21Shares, an effort to hedge against the dollar's hegemony with the rise of central bank digital currencies (CBDCs).

On March 16, former Bank of Japan executive Hiromi Yamaoka nodded to our thesis. He said that sanctions imposed on Russia could encourage more countries to look at CBDCs as a tool to counter the dollar's dominance in the global financial system. A month before Yamaoka’s statement, a week before the invasion, Russia had in fact begun piloting its digital ruble, following in China’s footsteps which had started piloting its digital yuan back in January.

Later in March the Bank of England (BoE) announced its partnership with the Massachusetts Institute of Technology Media Lab Digital Currency Initiative, or DCI, on a joint twelve-month research project on CBDCs. The new project is for research purposes only and is not intended to develop an operational CBDC, according to the BoE. The US on the other hand is taking big steps towards a digital dollar as part of President Joe Biden’s Executive Order (EO) published on March 9, which we’ll delve deeper into in the next section.

Regulations getting more serious

In the US, Biden signed an EO titled Ensuring Responsible Development of Digital Assets, assigning government agencies to a number of tasks:

- The Department of Commerce is asked to develop a framework for interagency international engagement with foreign counterparts to create an international forum to enhance the adoption of digital assets and standardized rules.

- National security agencies were asked to provide supplementary annexes on cyber security and make sure that US cryptocurrency laws align with those of the country’s allies to ensure international frameworks and partnerships are responsive to risks.

- The Treasury, Commodity Futures Trading Commission (CFTC), Securities and Exchange Commission (SEC), Consumer Financial Protection Bureau (CFPB) among others are assigned to gather recommendations to develop a policy for the digital asset sector.

- The Treasury Secretary is assigned to conduct a report on the future of money and payment systems. The report should delve into the impacts of digital assets on economic growth, financial growth and inclusion, national security, and the extent to which technological innovation may influence that future.

During the aforementioned hearing session on crypto’s role in illicit activities, Senator Elizabeth Warren introduced a bill targeting Russian crypto use. If Warren’s bill is passed, the presidential administration would be required to identify "any foreign person" operating a crypto exchange or facilitating digital asset transactions. Another provision would authorize the Financial Crimes Enforcement Network (FinCEN) to identify users transacting with more than $10,000 in crypto.

Middle East kickstarts regulation

In the UAE, Dubai rolled out its first legislation on cryptocurrencies, and is now in the amendments and approval phase. Non-fungible tokens (NFTs) and CBDCs are not covered in the Dubai Virtual Asset Regulation Law, which calls for the ban of “algorithmic tokens,” which interfere with supply and demand to control price and “privacy tokens,” designed to obscure token holders and trading patterns.

Whereas in Europe, the European Parliament Committee on Economic and Monetary Affairs and the Committee on Civil Liberties adopted on March 31, with 93 votes to 14 and 14 abstentions, their position on draft legislation strengthening EU rules against money laundering and terrorist financing. All transfers of crypto-assets will have to include information on the source of the asset and its beneficiary, information that is to be made available to the competent authorities. Patrick Hansen from blockchain firm Unstoppable DeFi warned that the regulation would require crypto service providers, such as crypto exchanges, to continue collecting personal data related to transfers made to and from unhosted wallets and to also verify the accuracy of the data gathered.

Britain has also been brewing some plans for its crypto industry. In the coming weeks, the British government is expected to reveal crypto regulation plans with a special focus on stablecoins. Although plans are still not made public, sources told CNBC that they are likely to be favorable to the industry, providing legal clarity for a sector that has so far been mostly lacking in regulation.

Further developments in crypto space

Ethereum saw its final public variation of its merge testnet preceding the final Proof-of-Stake (PoS) switch - dubbed Kiln - launch on March 24. In that view, the migration of the largest smart-contract network to a PoS network is soon to become a feasible reality by Q2 of 2022.

On the other hand, Avalanche had grounds for its rally rooted in the fact that Terra’s infamous anchor money-market protocol will now be deployed on top of the network through its wormhole integration. This should fend-off native users from having to take their funds off-chain and instead leave it within the premises of Avalanche.

We’ve seen many thought and market leaders, like David Heinemeier Hansson and Warren Buffet, change their minds about crypto; Stripe is one of them. In 2018, Stripe decided to stop supporting Bitcoin in payments, as they were “less useful” as such. On March 10, they updated the 2018 announcement with a disclaimer announcing their change of heart and their partnership with FTX. They would re-enter the crypto industry with a bundle of use cases that would give customers access to tools and APIs that facilitate buying and storing crypto tokens, cashing out, and even trading NFTs.

At 21Shares, we’ve always reiterated the thesis that increased institutional adoption is one of the effective ways for mass adoption, but in the case of Stripe, the roles were somehow reversed. With the size of Stripe’s scope, this may come as bad news for smaller crypto projects that worked to appeal to L1s and dApps to streamline their payments infrastructure as well as their KYC and KYB workflows. While in fact, Stripe is only raising the bar, rejuvenating the competition, which only means that the ecosystem’s skin is about to get a lot thicker.