A summarizing review of what has been happening at the crypto markets of the past week. A look at trending sectors, liquidity, volatility, spreads and more. The weekly report in cooperation with market data provider Kaiko.

The last 7 days in cryptocurrency markets:

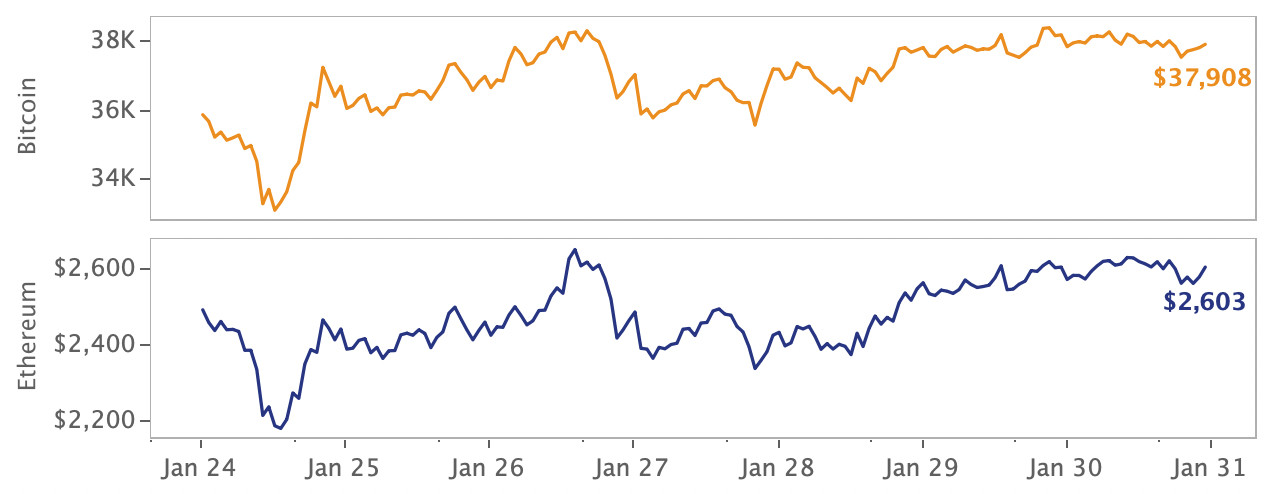

- Price Movements: Last week's hawkish Fed meeting spurred volatility in cryptocurrency markets, which remain on edge following three months of losses.

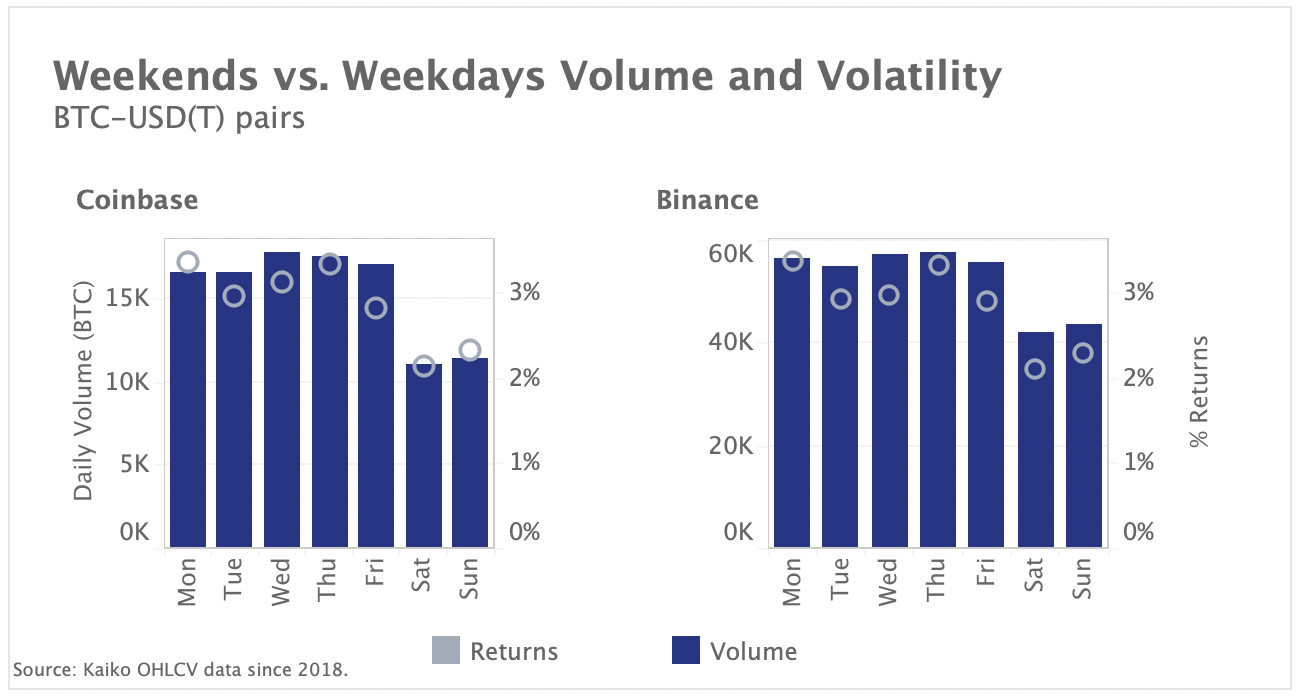

- Volume Dynamics: Weekend trade volume is significantly lower than weekday volume on Coinbase and Binance.

- Order Book Liquidity: The bid-ask spread for ETH-USD pairs has improved overall since 2020, but widened significantly this January amid high volatility.

- Derivatives: Average funding rates for both BTC and ETH entered bearish territory in January following a sharp drop in market sentiment.

- Macro Trends: 2-year treasury yields surged after the Fed indicated a likely March rate hike.

Investors remain risk adverse following Fed meeting

Both Bitcoin and Ethereum ended the week in the green despite last week’s hawkish Fed meeting in which Jerome Powell indicated a likely rate hike this March to combat inflation. The announcement triggered volatility in both crypto and equity markets, which have benefited heavily from loose pandemic-era monetary policy and now risk losses as investors take a more cautious approach. Persistently low funding rates and muted open interest suggest risk sentiment remains fragile in cryptocurrency markets. Despite an overall bearish January, NFT markets bucked the trend, recording all time high volumes and massive VC investments.

In industry news, Facebook announced it would sell its Diem stablecoin project, FTX.US attained an $8billion valuation (its parent company FTX is valued at $32B), and Binance reinstated payments from the European Union.

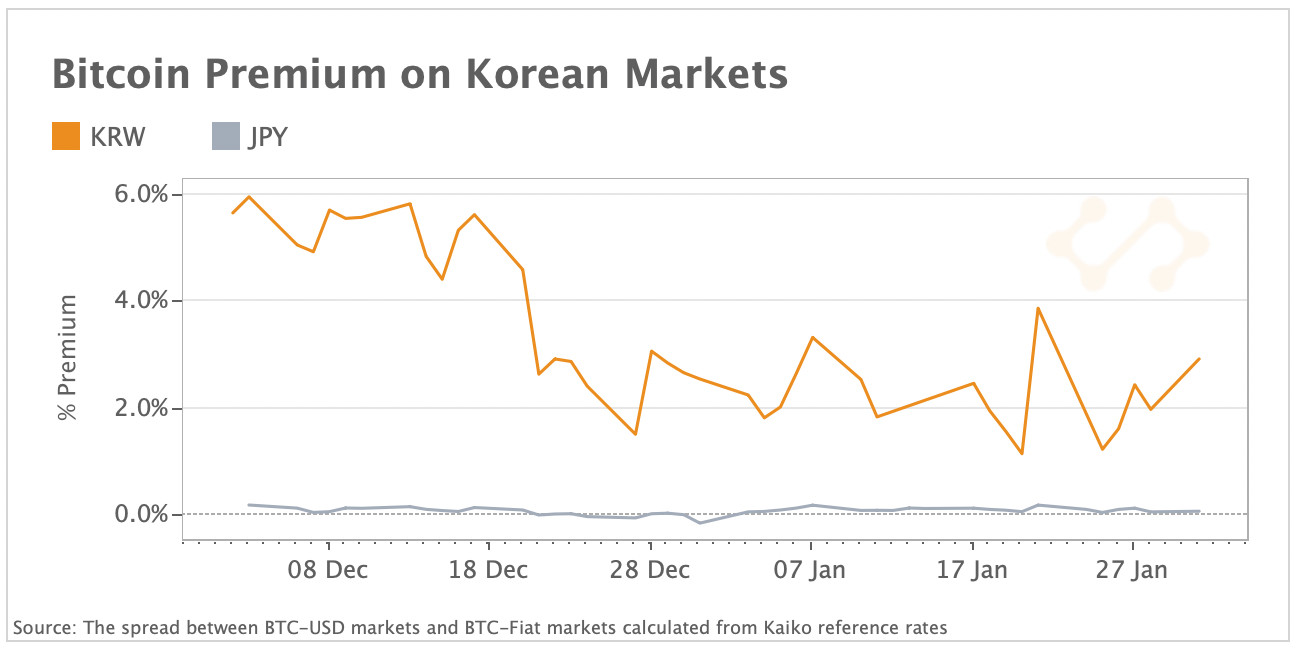

Kimchi premium drops amid tighter regulatory environment

Bitcoin’s premium on Korean markets - known as the “Kimchi premium” - has been on a steady downward trend over the past few weeks, falling from around 6% in early December to 1.4% as of end-January. The Kimchi premium is a crypto market phenomenon that has existed since 2017 and refers to a positive spread in the price of Bitcoin across USD and Korean markets. Demand for Bitcoin has weakened as major Korean exchanges moved to block withdrawals from unverified crypto wallets such as MetaMask and Ledger. South Korea has tightened its regulatory stance on digital assets over the past year. This has led to a consolidation of the market with several leading foreign exchanges such as Binance and Huobi discontinuing their operations in the country after failing to register with the country's anti-money laundering body.

Analyzing weekend volume vs. volatility over time

Despite 24/7 access to cryptocurrency markets, weekend liquidity has historically been lower than weekday liquidity, as measured by trade volume. Above, we chart average daily Bitcoin volume and average absolute price returns on Coinbase and Binance. On Coinbase, average daily volume on Saturday and Sunday is about 10k BTC, compared with weekday volumes of ~17k BTC. The difference between weekend and weekday volume is less pronounced on Binance, a more retail exchange with a global user base.

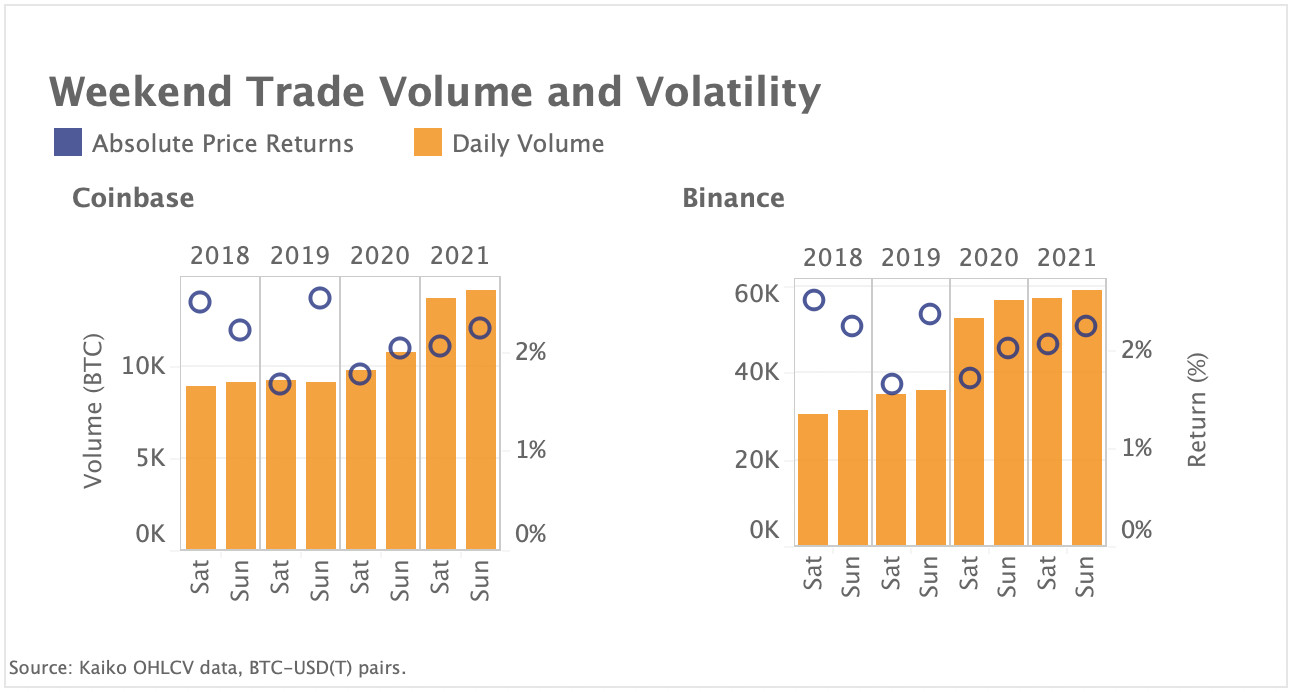

We can observe that despite lower liquidity, weekends have lower average absolute returns compared with weekdays. Average returns are between 2-2.5% on weekends, while returns are greater than 3% during the week, which suggests low liquidity doesn't strongly affect price movements. When looking at weekend liquidity over time, we can observe that volatility has fallen since 2018 while volumes have increased, suggesting that the ease of executing a trade on weekends has improved since 2018.

Above, we chart the average daily trade volume on weekends since 2018 alongside BTC’s absolute price returns. Weekend volatility increased slightly between 2020 and 2021, but has declined overall since 2018. Weekend trading volumes rose faster on Binance, almost doubling over the past two years, while volumes grew at a slower pace on Coinbase. This could be explained by the fact that Binance has a strong retail reputation while many institutional investors - which are trading during traditional market opening hours - prefer regulated fiat-to-crypto exchanges such as Coinbase.

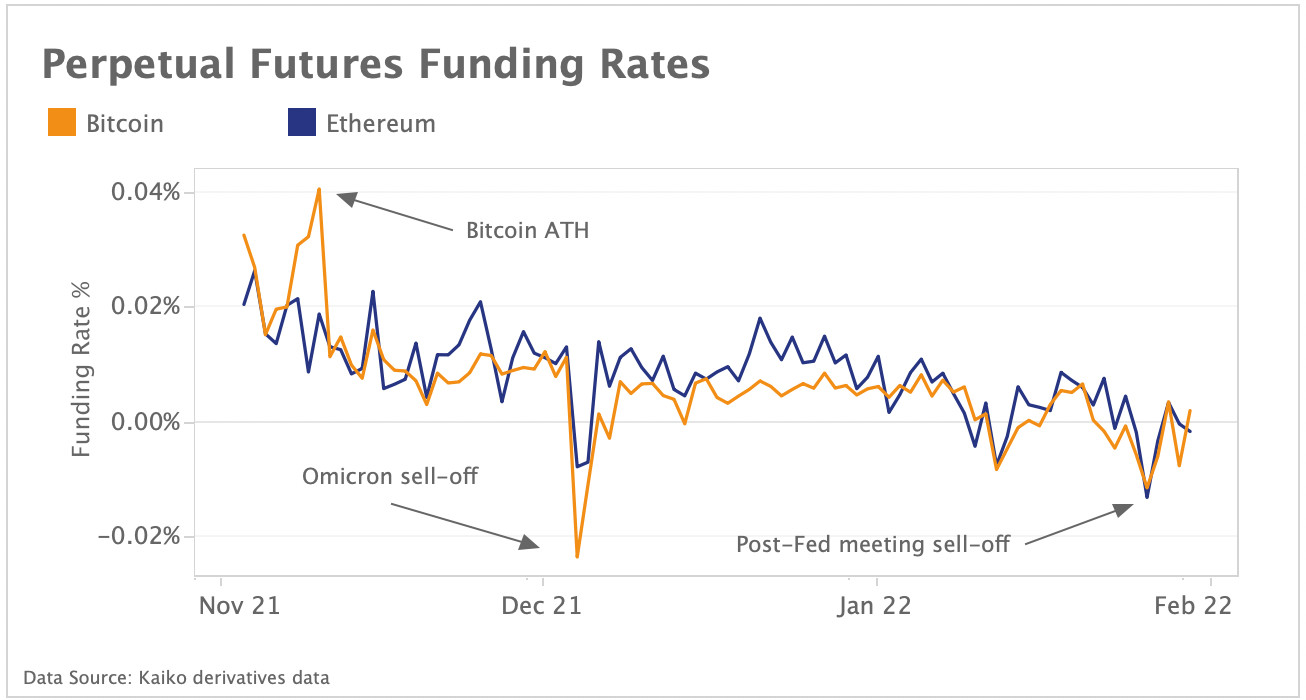

Funding rates drop sharply since November

Market sentiment remains firmly bearish with average funding rates for BTC and ETH perpetual futures dipping negative several times throughout January. The funding rate is the average cost of holding a long position and when negative, this means that perpetual futures prices are lower than the index price which suggests that more traders are entering short positions. Ethereum’s funding rates have been consistently higher than Bitcoin’s since end-November.

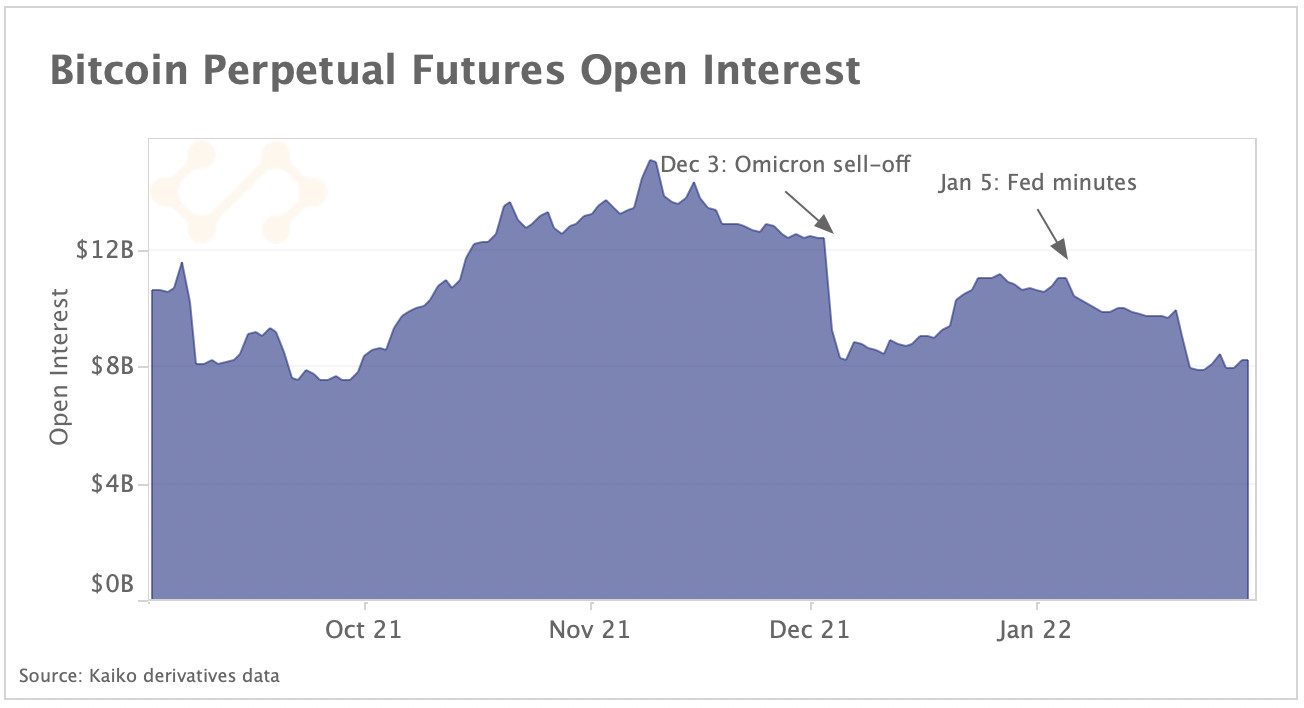

However, the two assets have been moving together closely in January following a sharp drop in bullish sentiment across all crypto assets. Open interest has also remained muted since reaching all time highs in November.

Following the latest bout of volatility, open interest for Bitcoin perpetual futures has fallen from $10B to $8B over the past month. Open interest is now at its lowest levels since September, which suggests low amounts of leverage in derivatives markets.

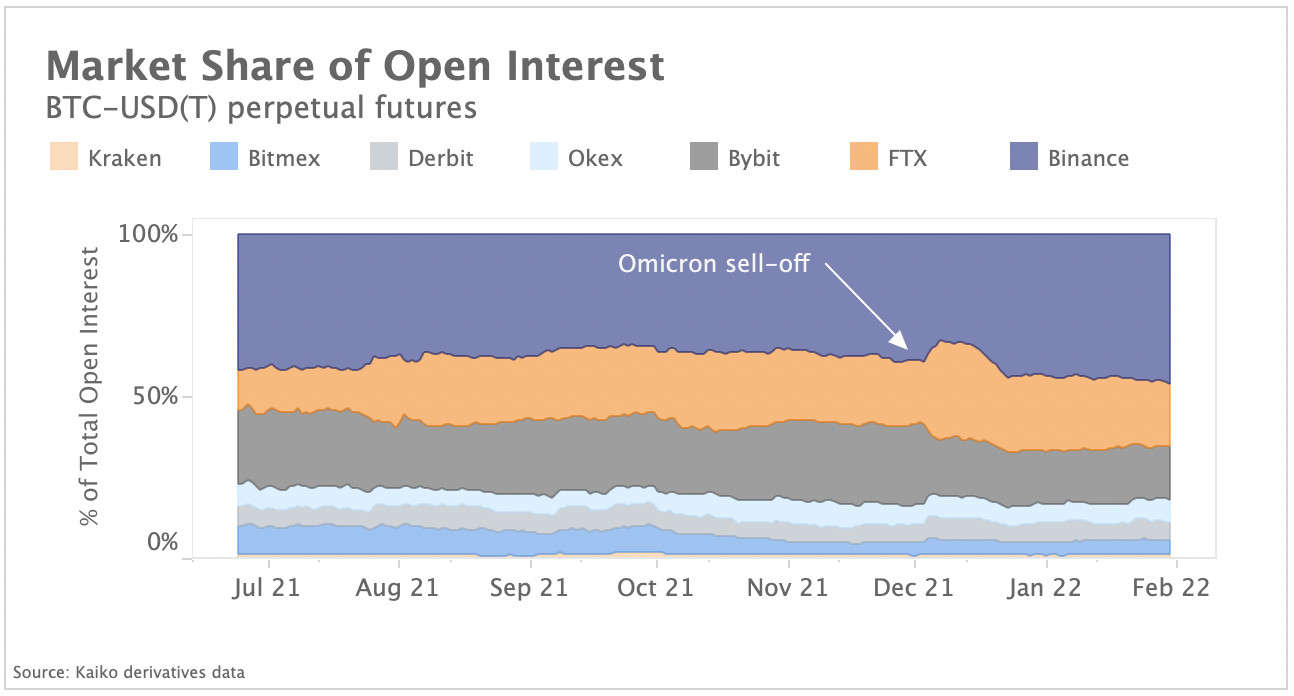

Binance and FTX dominate Open Interest

Despite recent bouts of volatility, Binance’s market share of open interest for perpetual futures recovered in January after hitting a multi-month low of 34% during the December sell-off. Retail-oriented exchanges have been hit hard by the wider market crash, with Binance and Bybit registering a sharp decline in their share of total open interest, after over $830mn of long positions got liquidated on both exchanges between Dec 3-4. While Binance has managed to recover, the amount of open contracts on Bybit has continued declining relative to its peers. Meanwhile, FTX’s market share of open interest has increased from 12% to 19% since July 2020.

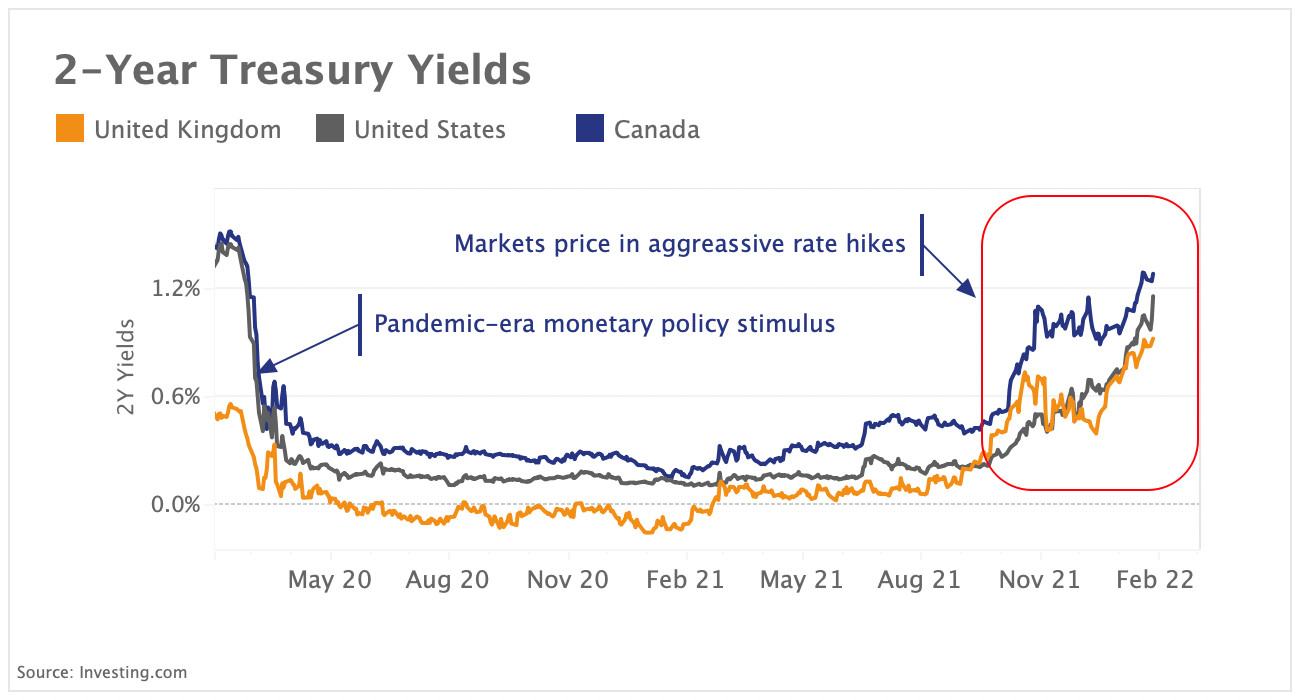

Treasury yields surge as Fed flags March rate hike

Last week, the U.S. Federal Reserve flagged its first rate hike for March, despite volatile equities and falling risk sentiment. The move caused short term U.S. treasury yields - a proxy for market expectations on the future direction of monetary policy - to register their biggest daily jump in nearly 2 years. The chart above shows that Canadian and UK 2-year treasury yields have also surged since September as markets price in a removal of the so-called “Fed put”, referring to the central bank’s support for equity markets in times of trouble. The tightening of financial conditions has been a major headwind for risk asset valuations over the past few months and is expected to to push stock prices lower, which could have investors seeking safe havens.

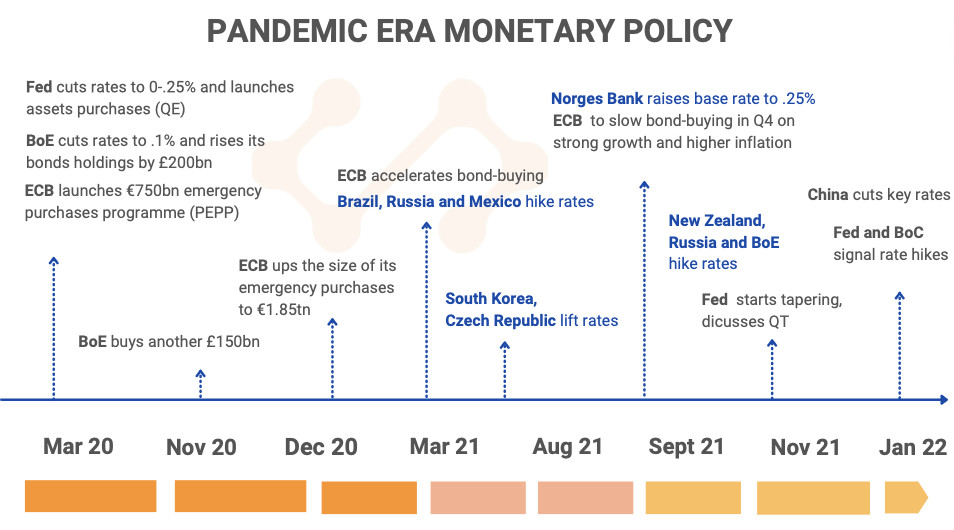

However, while many global central banks are gradually pivoting towards normalisation of their post-pandemic monetary policies, the pace varies across regions. In the infographic below, we outline some of the major monetary policy moves.

Tightening has been on the agenda of several Eastern European countries over the past few months. By contrast, rate moves have been muted in Asia where inflationary pressures were much more moderate in comparison to the U.S. due to slower increases in food and energy costs. China recently cut its key rates in order to boost its economy amid concerns around its property sector woes and slowing growth.

The divergence between the Fed and the European Central Bank (ECB) is also growing with the ECB reiterating its commitment not to raise rates in 2022. This is expected to partly offset some of the headwinds from tightening of financial conditions in the U.S. and other developed markets.

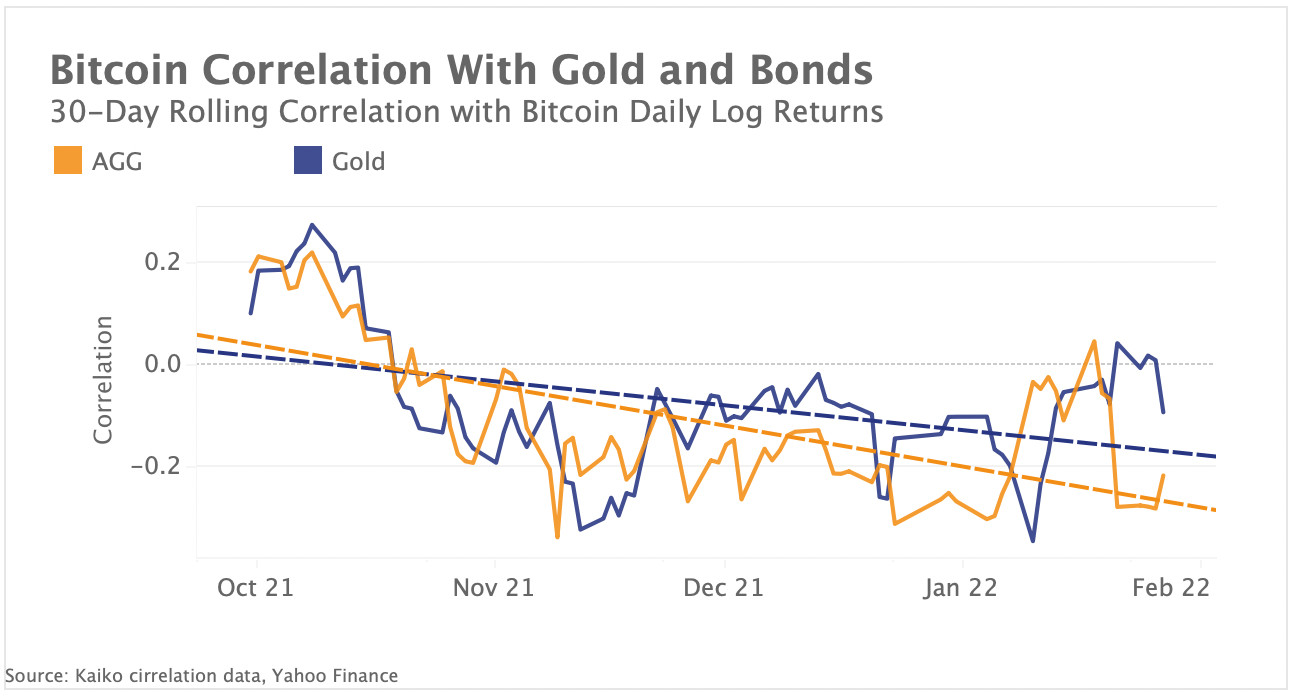

Bitcoin's correlation with gold and bonds remains negative

While Bitcoin’s correlation with tech stocks has surged over the past few months, its correlation with safe-haven gold and bonds has been mostly negative since October. Above we chart the 30-day rolling correlation between Bitcoin, gold and the aggregate bonds index (AGG). The aggregate bond index is a broad fixed-income index that tracks the U.S. investment-grade bond market. Typically, bonds provide a hedge for stock market investors and their prices often increase when stock prices fall. However, their correlation with equities has been shifting over the past two years, pushing asset managers to explore different asset classes such as commodities, real estate and crypto as tools for diversification.