A joint study by McKinsey and Artemis Analytics provides the first differentiated view of the stablecoin payments market. The central finding is surprising: Of the USD 35 trillion that flowed through stablecoin networks in 2025, only around USD 390 billion went to actual payments.

The rest consists of crypto trading, internal transfers, and protocol-related transactions. MKinsey's analysis is the first to systematically distinguish between transaction volume and real payment flows. The frequently cited comparisons with Visa or Mastercard are misleading: While stablecoins appear to process similar volumes at first glance, actual payments reach only 0.02 percent of global payment traffic of over USD 2 quadrillion annually.

Methodological distinction between volume and payments

For the study, McKinsey combined bottom-up and top-down approaches. First, analysts tagged custody providers. Then they examined transaction patterns and filtered out trading activities and high-frequency operations. Excluded activities include: exchange liquidity pools, automated smart contract interactions, liquidity management, arbitrage, and protocol-related mechanisms.

This distinction is relevant for companies and regulators. On one hand, it shows where stablecoins actually function as a means of payment. On the other hand, it reveals where they primarily serve crypto infrastructure. The methodology also makes clear that headlines about stablecoin volumes exceeding traditional payment networks miss the point.

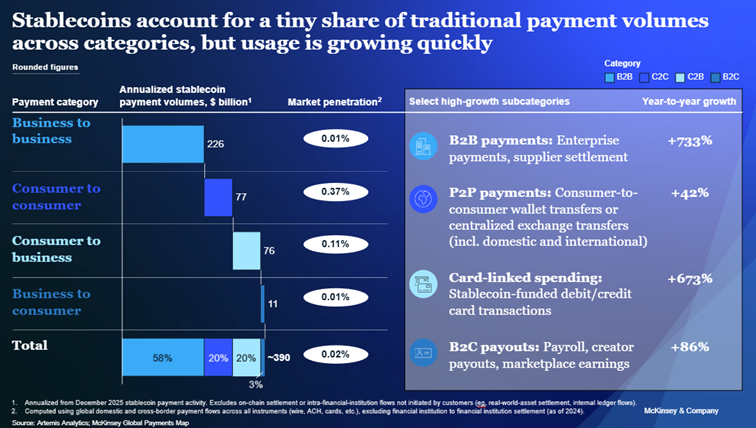

B2B payments dominate with 733 percent growth

The breakdown by use case shows a clear hierarchy. B2B payments stand out in particular: They reached USD 226 billion, accounting for 58 percent of total stablecoin payment volume. Year-over-year growth of 733 percent underscores the momentum in this segment. Companies are increasingly using stablecoins for cross-border supplier payments and international settlements.

Global payroll and remittances totaled USD 90 billion. This corresponds to approximately one percent of the USD 1.2 trillion remittance segment. Capital market settlements reached USD 8 billion, while stablecoin card payments stood at USD 4.5 billion. The latter also recorded strong growth of 673 percent year-over-year.

"The fact that real stablecoin payments are much lower than routine estimates does not diminish the long-term potential of stablecoins as payment infrastructure. Instead, it creates a clearer baseline for assessing where the market stands." - McKinsey and Artemis Analytics

Asia leads with 60 percent market share

The geographic distribution shows clear concentration in the Asia-Pacific region. Singapore, Hong Kong, and Japan dominate with a combined stablecoin payment volume of USD 245 billion. North America follows with USD 95 billion, Europe with USD 50 billion. In contrast, Latin America and Africa remain marginal at under one billion USD each.

This distribution reflects different regulatory frameworks and market structures. In Asia, established fintech ecosystems and high remittance volumes drive adoption. Still, the GENIUS Act passed in the US in July 2025 is likely to influence North American figures going forward. The law creates a comprehensive regulatory framework for stablecoin issuers for the first time and requires 100 percent reserve backing.

Market capitalization and competition among issuers

The circulating stablecoin supply exceeded USD 300 billion at the end of 2025. Shortly after, market capitalization reached an all-time high of over USD 311 billion in January 2026. Tether's USDT dominates with around USD 187 billion and a 60 percent market share. Circle's USDC follows with approximately USD 74 billion.

Yet growth rates show a shift. USDC grew 73 percent in 2025, while USDT gained only 36 percent. For regulated B2B applications, companies increasingly prefer USDC. In contrast, USDT remains dominant in emerging markets on networks like Tron and Solana, particularly for peer-to-peer transfers.

Outlook: Infrastructure on the verge of breakthrough

The McKinsey analysis forecasts stablecoin market capitalization of USD 2 to 4 trillion by 2030. Integration by traditional payment providers like Visa and Stripe is accelerating. At the same time, crypto companies like Circle and Tether are positioning themselves as alternatives to slow and costly international wire transfers.

The study establishes a sober baseline for future assessments. Stablecoins as a payment method are at the beginning, not the finish line. Actual adoption will be measured by real payment flows, not transaction volumes.