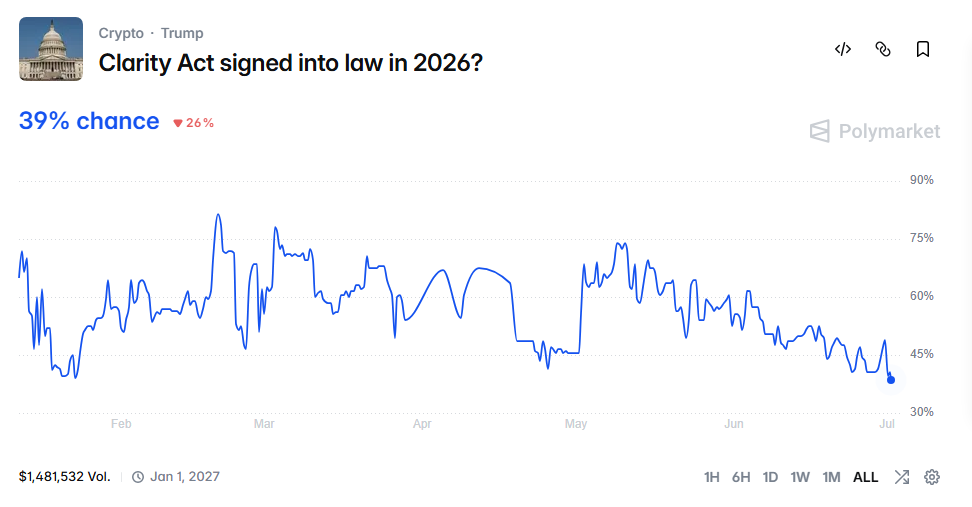

The delay of the Clarity Act in the US Senate is intensifying. In late June, Galaxy Research cut the probability of a 2026 signing to 50%. Meanwhile, the prediction market Polymarket most recently priced the odds at just 39%.

The Clarity Act would set the first federal rules for digital assets. It aims to define when an asset qualifies as a security under the SEC. It would also clarify when an asset instead counts as a commodity under the CFTC. Bitcoin, Ether and other assets with a functioning blockchain would fall under the CFTC. Classic capital-raising token sales, by contrast, would remain with the SEC. Payment stablecoins, however, would receive joint oversight, building on the already enacted GENIUS Act. The House of Representatives had already passed the bill (H.R. 3633) in July 2025. It cleared the chamber on a bipartisan basis, by 294 to 134 votes. In the Senate, however, the text took considerably longer. The Agriculture Committee held its markup first, in January 2026. The Banking Committee followed only in May 2026, by 15 to 9 votes. Since early June, the Clarity Act has additionally sat officially as Calendar No. 423 on the Senate Legislative Calendar. In theory, it could come to a vote without further committee work. So far, however, no source has named a concrete date for the floor vote.

Why the Clarity Act delay narrows the Senate window

The Clarity Act is not failing over substantive differences, but over a procedural bottleneck. For a floor vote in the full chamber, the text needs 60 votes. With around 53 Republican seats, roughly seven Democratic crossover votes are therefore required. So far, the central stablecoin compromise has been publicly backed above all by Senators Thom Tillis and Angela Alsobrooks. The remaining votes needed remain open. Committee members also stressed one point. A vote in committee is no guarantee of the 60 votes needed on the floor.

In addition, a procedural hurdle remains. First, the Banking version from May 2026 and the Agriculture version from January must be merged into a single text. More than 100 filed amendments had previously delayed the Banking markup originally planned for mid-January. The draft has been on the Senate calendar since 1 June 2026. However, a floor vote is thereby merely possible, not scheduled.

Several procedural steps still lie ahead. A merged text, a motion to open proceedings and a floor debate must all come first. An amendment process and renewed action in the House of Representatives would then follow. All of it would have to fit into a few weeks. The realistic timeframe therefore shrinks with every session week in which no vote is scheduled.

The ethics clause remains the final point of contention

Observers now consider the major substantive dispute largely resolved. The stablecoin compromise in Section 404 appeared on 1 May 2026. Three days later, Tillis and Alsobrooks confirmed the text as final. It prohibits interest or yield on dormant stablecoin balances, but permits activity-based rewards. As a result, one long-standing question finally fell away. It had blocked the law for months and formed the biggest front between the camps.

What remains open, however, is a single, politically sensitive passage: the ethics clause. It would bar officeholders from private crypto dealings. Democratic Senators Kirsten Gillibrand and Chris Van Hollen are making their support conditional on precisely this clause. Without these Democratic votes, the Clarity Act ultimately lacks the majority needed on the floor.

The White House accepts general rules, but rejects clauses that target individuals. Implicitly, this refers to the Trump family with its own crypto interests. This question therefore determines whether the remaining Democratic votes materialise at all. A bill that is substantively fully negotiated ultimately hangs on a primarily political conflict of interest.

Prediction markets lower the odds of success

Concrete figures reveal the waning optimism. The prediction market Polymarket, where users bet real money on political outcomes, augurs nothing good. The probability traded there peaked at 82% in February 2026. It then fell through 70% in mid-May to just 39% most recently. Both indicators are therefore moving below the threshold of a majority probability for the first time. The market consensus itself increasingly doubts a passage within the current year.

The investment bank Jefferies also warned in late June of the consequences. A failure before the August recess could push the bill to 2027 or later. This applies in particular if the Democrats retake the Senate in November. Consequently, the bank expects increased volatility for crypto tokens and blockchain stocks such as Circle, Coinbase and Bullish. Their valuations hinge directly on the question of whether the US creates a binding regulatory framework.

2027 becomes the last window before 2030

After the summer recess in August 2026, Congress moves into the midterm campaign. Complex, bipartisan financial legislation, experience shows, finds little floor time in such phases. If the vote falls through now, 2027 therefore counts as the earliest possible next window. The crypto industry has invested heavily in political spending during the current election cycle. Whether that translates into Senate votes, however, remains uncertain.

Senator Cynthia Lummis warns even more clearly. She chairs the Senate Banking Subcommittee on Digital Assets. That role also makes her the bill's most important advocate in the Senate. She is not standing for re-election and, in the worst case, sees the legislative window closed until at least 2030.

"This is our last chance to pass the Clarity Act before at least 2030. We cannot afford to give up on America's financial future." - Cynthia Lummis, Senator (R-WY)

Moreover, even a successful signing would not mean immediately enforceable rules. According to observers, the actual implementation is likely to take about a year or longer. It would involve regulatory texts, comment periods and compliance deadlines. Binding requirements would consequently take effect in 2027 or 2028 at the earliest. Until then, the fragmentation persists. The SEC continues to claim jurisdiction over many tokens as securities. The CFTC, meanwhile, remains essentially confined to combating fraud and manipulation in spot crypto markets.