The Bitcoin price fell to USD 59,023 and slid to its lowest level since October 2024, dropping below the USD 60,000 mark once more. The daily decline of 5.4% triggered around USD 800 million in long liquidations.

After Bitcoin had reached all-time highs in late 2024 and early 2025, the decline now amounts to 19.9% over 30 days and 30.6% since the start of the year. The US spot ETFs, approved since January 2024, were considered a reliable inflow pillar until the spring of 2026. However, all three buyer categories are now missing at the same time: retail is retreating, ETF buyers have produced net outflows for six consecutive weeks, and Strategy, the world's largest corporate Bitcoin holder, sold Bitcoin for the first time in years to fund dividends.

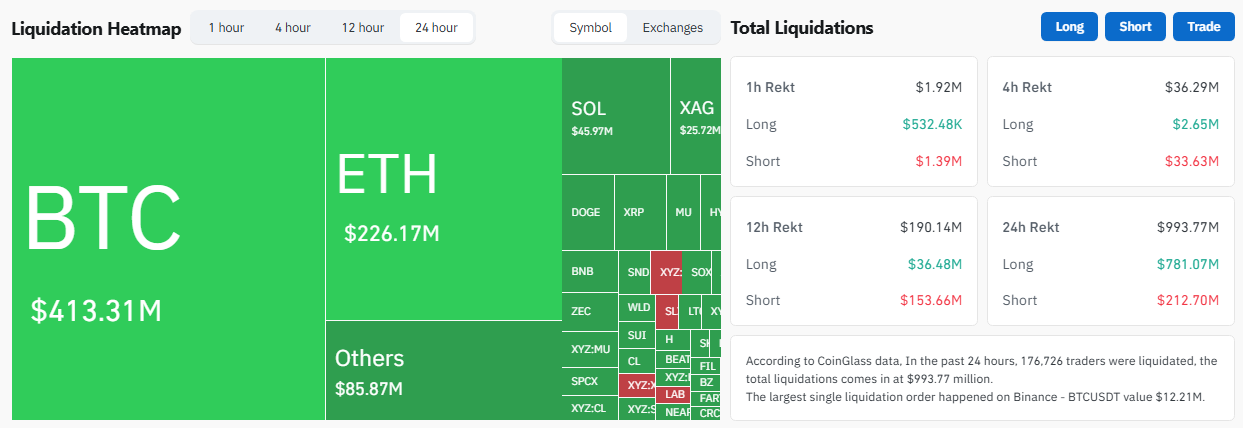

Options expiry and liquidation wave intensify the Bitcoin price slide

The decline on 24 June was not an ordinary sell-off. In the preceding 24 hours, around USD 800 million in long positions were liquidated, which intensified the downward pressure further. Moreover, it was already the second time the USD 60,000 mark had been breached within a month, after Bitcoin had briefly slipped below it in early June. As of today, the price recovered slightly to USD 61,500.

The next pressure valve is imminent. On 26 June, Bitcoin options with a notional value of around USD 10 billion expire on the derivatives exchange Deribit. The so-called max pain level, meaning the price at which the most options expire worthless, sits at roughly USD 74,000 and therefore well above the current level. At the same time, open interest is heavily concentrated on the USD 60,000 put and the USD 80,000 call. As a result, this constellation makes the USD 60,000 mark a technically sensitive threshold, where hedging trades can fuel volatility further just before expiry.

Strategy's flywheel turns in reverse

The slide hit Strategy's shares harder than Bitcoin itself. MSTR fell more than 10% on 24 June to USD 92 and thus reached its lowest level since February 2024, marking the sixth consecutive losing day. The day before, the company had already traded intraday below USD 100 for the first time since March 2024 and subsequently closed at USD 103.84. The firm holds 847,363 Bitcoin at an average purchase price of around USD 75,680 per coin; at prices between USD 59,000 and USD 61,000, the unrealised losses therefore add up to an estimated USD 11 billion.

The financing pressure becomes most visible in the preferred shares. STRC, the company's perpetual preferred share, fell to USD 79.85 on 24 June and thus trades well below its par value of USD 100, which drove the effective yield to around 14%. At the same time, the annual dividend obligations have risen from about USD 300 million to roughly USD 1.2 billion. Moreover, the at-the-market programme for the ongoing issuance of new common shares, long the central source of financing, was temporarily suspended.

This very pressure forced Strategy into a symbolically charged move. Between 26 and 31 May, the company sold 32 Bitcoin at an average of USD 77,135, selling Bitcoin on a net basis for the first time since 2022 to fund STRC dividends. The amount corresponded to merely 0.004% of its holdings, yet the signal value was considerable. During the upswing, the model functioned as a flywheel: a rising MSTR share enabled capital increases, the fresh money flowed into further Bitcoin purchases, and the additional demand supported the price. When prices fall, this mechanism runs in reverse.

US spot ETFs record six losing weeks in a row

The second institutional pillar is crumbling as well. Between 15 May and 3 June, the US spot Bitcoin ETFs recorded net outflows on 13 consecutive trading days, the longest outflow streak since their launch, totalling USD 4.33 billion. In early June, the largest weekly outflow since the approval in January 2024 followed at USD 3.4 billion. BlackRock's IBIT, the largest fund in the segment, lost around USD 980 million in that record week alone. Overall, the assets managed in the ETFs shrank during the streak from USD 104.29 billion to USD 80.40 billion.

A recovery failed to materialise afterwards. As of 24 June, six consecutive weeks of net outflows added up to a total of USD 5.94 billion. The spot ETFs were originally designed as a permanent institutional demand base and had supported the price for months through continuous inflows. Meanwhile, they instead act as a reliable outflow source and withdraw the very liquidity from the market that they had previously supplied.

Macro pressure and AI competition remove all three buyer pillars

The third pillar, retail trading, has also retreated. On June 24, the Fear & Greed Index stood at 24 and thus in the "Extreme Fear" range, which signals pronounced risk aversion among small investors. The changed interest rate environment is considered the main driver: expectations of imminent Fed rate cuts have shifted, and Bitcoin currently behaves more like a highly volatile risk asset than the often invoked inflation hedge.

In addition, there is structural competition for capital. Part of the funds that previously flowed into crypto are now migrating into AI infrastructure and semiconductor stocks as an alternative investment. Over a one-year horizon, Bitcoin has lost 30.6%, and the narrative of the reliable store of value comes under further pressure with each phase of stress.