Strategy, the Bitcoin accumulation firm led by Michael Saylor, has sold Bitcoin for the first time since December 2022: 32 BTC for roughly USD 2.5 million. The proceeds are earmarked for distributions on preferred stock.

Strategy, formerly MicroStrategy, is a publicly listed Bitcoin treasury company. Its core business model consists of raising capital through capital market instruments such as shares, convertible bonds and preferred shares to accumulate Bitcoin. The company currently holds 843,706 BTC, more than 4% of the fixed total supply of 21 million units. The accumulation originally began in August 2020 under founder Michael Saylor. Since then, there have been no realized sales with strategic intent. The only precedent came in December 2022, a tax-loss trade: Strategy sold 704 BTC and bought back 810 BTC within two days. Strategy's current Strategy sale is structural in nature, however, because it finances ongoing dividend obligations. The 32 BTC went for an average price of USD 77,135, roughly 1.9% above the company's internal cost basis of USD 75,699.

Preferred stock dividends as the trigger for the Strategy Bitcoin sale

The company's capital structure provides the reason for the liquidation. Strategy has issued several series of preferred stock that require regular distributions. On 30 June 2026, dividends fall due on all series: STRF at USD 2.50 per share, STRC at USD 0.958333 per share with an annual rate of 11.50%, STRK at USD 2.00, STRD at USD 2.50 and STRE at EUR 2.50 per share. These obligations arise independently of the Bitcoin price. Therefore, they create a permanent cash flow requirement.

An earmarked USD reserve serves as a buffer. As of the end of May 2026, it stood at USD 900 million and is reserved for dividends and bond interest. The STRC share came to market with a face value of USD 100 and a high yield promise. Precisely this structure creates an ongoing obligation volume, however, which is difficult to cover without continuous share issuance or Bitcoin liquidations. The 32-BTC sale is therefore not a strategic retreat but a forced cash flow act.

On the Q1 2026 earnings call, Saylor named the central threshold above which the model holds without common stock sales. Additionally, the company is reviewing a switch from monthly to semi-monthly distributions. Shareholders are due to vote on the change on 8 June 2026.

"At our current positions, Bitcoin must rise 2.3% annually for our existing holdings to cover the STRC dividend obligations indefinitely, without us selling common stock." - Michael Saylor, Executive Chairman, Strategy

Onchain signal and market reaction

The market had anticipated the transaction. Earlier, at the end of May 2026, Arkham Intelligence registered a movement of roughly 411.6 BTC from Strategy's Coinbase Prime custody to a cold wallet. As a result, the implied sale probability on prediction markets rose to 84% before year-end 2026. However, the company actually sold only 32 BTC, which suggests that the bulk of the moved coins were reshuffled internally.

The MSTR share reacted as well. It last traded at USD 159.09, a weekly loss of 3.1% against an annual return of 2.9%. Later, after publication of the SEC 8-K filing, the stock fell roughly 6% in pre-market trading. MSTR now sits roughly 65% below its all-time high from the summer of 2025.

The pressure on the model also shows up in the balance sheet. In the first quarter of 2026, the company reported a net loss of USD 12.54 billion, of which USD 14.46 billion were unrealized Bitcoin losses. At the time of the filing, this resulted in an implied book loss of roughly USD 2.9 billion. Meanwhile, the market NAV multiple stood at roughly 0.98, just below par.

Bitcoin sale in the context of debt reduction

The sale does not stand in isolation but fits into a broader balance sheet strategy. In the prior week, the company bought back USD 1.5 billion notional of its zero-coupon convertible bonds maturing in 2029 for roughly USD 1.38 billion, an 8% discount to face value. Strategy financed the buyback from the USD reserve, from USD 83.7 million in ATM proceeds and from an STRC issuance of USD 1.949 billion. The move makes economic sense, because the conversion price of these bonds stands at USD 672.40. As a result, a conversion at the current MSTR price of roughly USD 159 was unrealistic. Without the buyback, the notes would effectively have come due as debt for repayment. The outstanding convertible bond volume thereby fell from USD 8.2 billion to USD 6.7 billion.

At the same time, the company uses its at-the-market equity program as a liquidity source. Between 26 and 31 May, Strategy sold 801,994 MSTR shares for net proceeds of USD 128.3 million. Notably, none of these shares flowed into Bitcoin during the reporting period. The remaining ATM capacity moreover amounts to roughly USD 26.1 billion, and the company expanded its programs by USD 21 billion in MSTR, USD 21 billion in STRC and USD 2.1 billion in STRK. Saylor nevertheless positions the sale as a footnote within an accumulation logic. For every Bitcoin sold, Strategy will buy 10 to 20 more, he stated.

Strategy's position in the corporate Bitcoin market

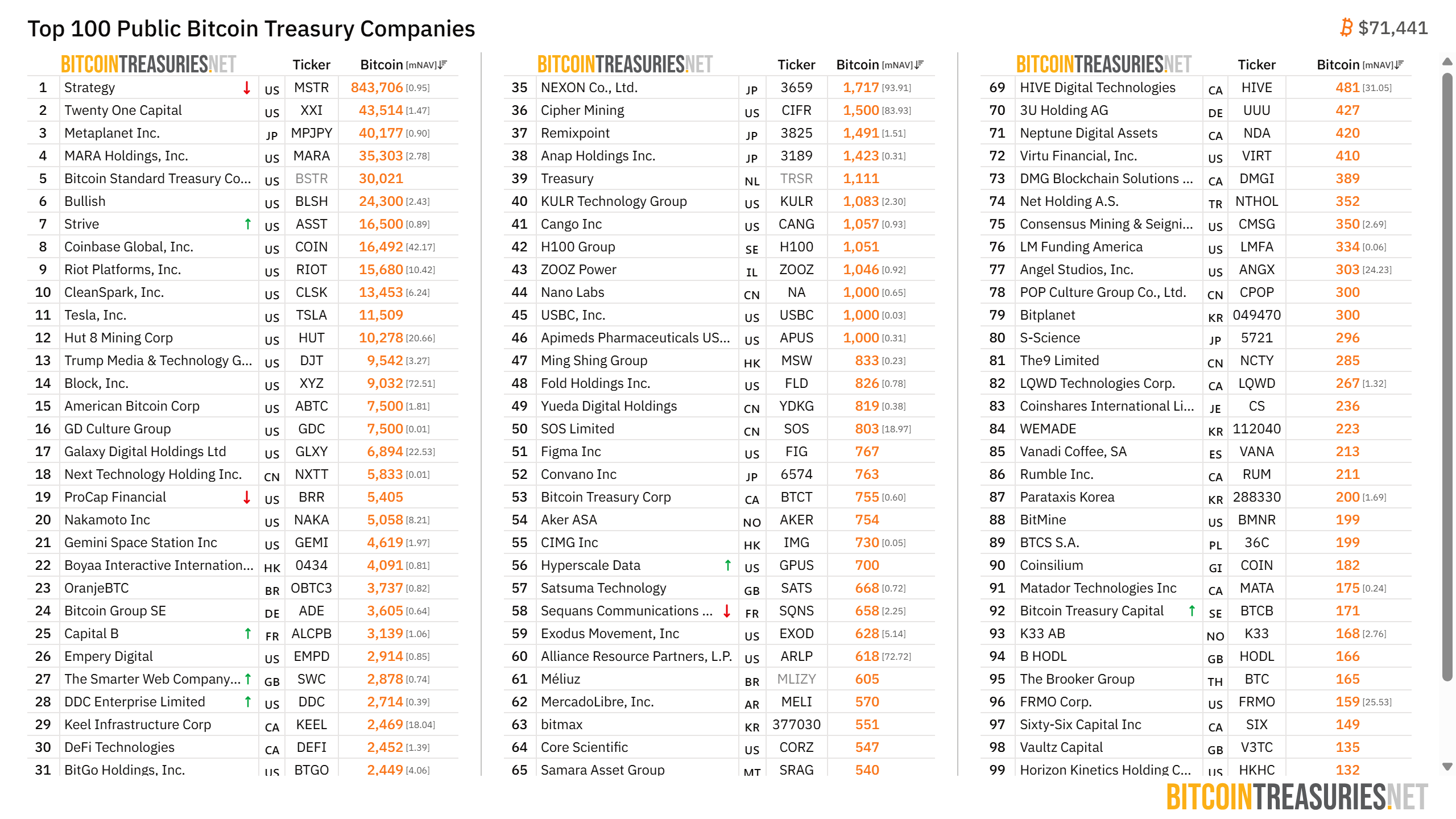

Despite the sale and book losses, Strategy remains dominant among publicly listed Bitcoin holders. In total, 198 publicly listed companies hold some form of Bitcoin position, and Strategy leads the field by a wide margin with 843,706 BTC. The nearest pursuers trail well behind: Twenty One Capital holds 43,514 BTC, Metaplanet 40,177 BTC, MARA 35,303 BTC and the Bitcoin Standard Treasury Company 30,021 BTC. Taken together, corporate holdings add up to roughly 1.15 million BTC, about 5.47% of total supply.

Strategy itself describes MSTR as a "BitVac" and points out that in 2026 it has so far bought 2.6 times the amount of Bitcoin mined over the same period. Measured against that scale, the 32-BTC sale remains marginal and does not shift the accumulation logic. Nevertheless, it marks a structural turning point, because it demonstrates that the company's dividend architecture creates a cash flow requirement that qualifies the "never sell" narrative.