Crypto lending is young, but a rapidly growing industry. A three-part series on the past, present and future of crypto-credit markets. In this article: The past and the evolution of credit markets in the cryptocurrency ecosystem.

The world loves leverage. Debt is the magic that has fueled economic growth since the dawn of time, and while we’ve come a long way from the days of the Iron Bank — throwback for you Game of Thrones fans — global debt is by far the largest asset class and investment category. Whether government debt, corporate debt, derivatives, consumer debt, or some permutation thereof, leverage is the lubricant that keeps the wheels of the global machine spinning.

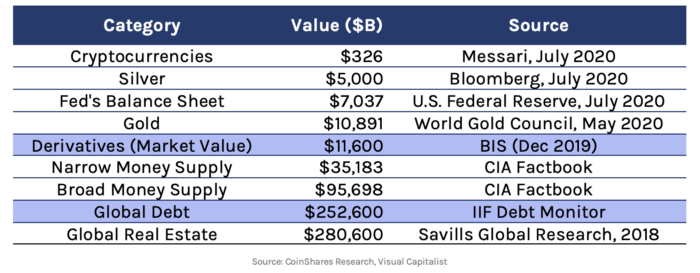

Figure 1: Global Asset Base (Ranked in Size)

Bitcoin is often touted as a hedge against the debasement of fiat currencies by governments and their Central Banks. Watching Chairman Powell at work with the money printer (brrr) certainly highlights the sharp contrast between bitcoin and fiat. Bitcoin is digitally scarce, and so in the above table of global assets, we expect it to behave more like gold and appreciate in price as demand for it rises, rather than to behave like fiat and some other cryptocurrencies, that inflate supply to meet demand.

However, investors who hold bitcoin are only rational human beings. Just as we’ve witnessed the financialization of bitcoin with the exponential growth of bitcoin derivatives markets — including both synthetic cash settled instruments as well as digitally settled instruments — the bitcoin lending space continues to grow exponentially quarter after quarter.

Please step into our magical time machine and allow us to transport you to 2017… (no seriously that was like… 2 crypto-eons ago)

Crypto Financing History Lessons

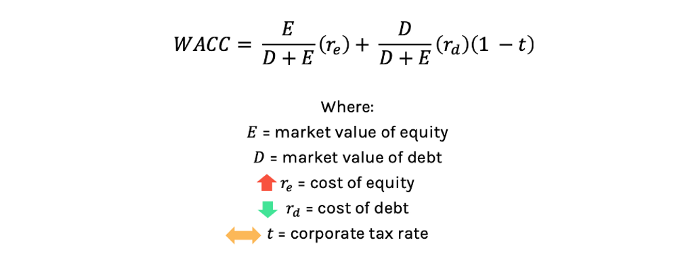

If you’re a fan of modern economics, you’ll be familiar with the capital asset pricing model, perhaps the phrase WACC is whack, and the work done by Miller and Modigliani. We only mention MM63 for the purposes of introducing the cost of debt, or r(d), which influences how firms make financing decisions.

Figure 2: Are Equity and Debt Equal? The Vagaries of CAPM

So why bring up WACC? Well, historically, companies in the crypto ecosystem have been financed purely by equity. As one of few crypto investors around in 2015, we can confidently say that the idea of debt financing didn’t really exist. The cost of equity was variable, but generally, quite high. Average dilution in a financing round ranges from 20–40%, depending on your business model, your jurisdiction, and your ability to sell the valuation to investors. So, for most companies, access to capital was basically limited to E, equity, and r(e) was expensive.

Given that bitcoin was trading in the range of $200 to $300 for an extended period of time, but had traded at $1,200 before, founders were not keen to sell their coins for cash to finance working capital. In fact, some of the companies which funds were investing in committed a big no-no, they used some of their financing to buy MORE bitcoin and would hold bitcoin on their balance sheet rather than liquidating it, believing bitcoin’s value would rise. In 2017 and 2018, many companies raised very large financing rounds on “revenue” metrics that were largely fueled by the rise in the price of the underlying assets, bitcoin and ether.

In 2017, investors started thinking about how to finance companies who had short term working capital needs. It didn’t make sense to raise highly dilutive, very expensive equity capital to finance a short-term need stemming from a cash flow timing mismatch. Some companies already had crypto on their balance sheets, so lending against that crypto collateral provided a low-risk way of extending credit at modest rates to finance growth opportunities. Trading desks with cash on their balance sheet were in a great position to begin providing short-term capital to these companies, especially if they were already investors via their venture strategy.

As bitcoin went from $700 to $1200 to $10,000 within the span of six months, the market for crypto collateralized debt grew dramatically. Early stage companies in an investment portfolio with limited cash on their balance sheets were able to finance working capital in a new way, effectively creating a market for debt. And so, a crypto debt market was born, and r(d) was created. And more importantly, because loans were collateralized with a highly liquid and readily saleable asset, bitcoin, the level of risk required was very low. It should not come as a surprise that today crypto collateralized lending rates are not that much higher than other types of corporate debt, and in some instances, crypto firms can actually access debt at better rates than other types of technology startups.

One final point here — the introduction of a robust asset-backed debt market is a game-changer for the crypto ecosystem and many of the companies in it.

Lowering the Cost of Capital

The average cost of capital has come down significantly, thanks in large part to this growing debt market. Rates to borrow dollars by posting bitcoin collateral are anywhere from 8 to 12%, which is much more attractive than 20–40% dilution via equity. And don’t forget the important tax advantages of financing with debt, which further sweeten the deal. The accessibility of capital in this industry has increased significantly, as more venues emerge to cater to this debt market.

On the risk side of the equation, today the vast majority of institutional crypto lending is fully collateralized, usually by a ratio of anywhere from 1.25–3x the loan amount, depending on the volatility of the underlying asset. If you have collateral that experiences wild swings in value, you don’t want to be posting margin calls 24/7.

Today, effectively riskless lending via crypto-collateralized loans is still earning 8–12% APY. Given lending in traditional markets is going for LIBOR + 1, or if you have access to the printer, zero, we expect crypto lending rates to come down as more capital hunts for yield.

In fact, this tees up the theme of “yield farming” perfectly.

In a world where capital is abundant, but yield is scarce, investors are willing to move further out on the risk curve to find returns. We’ll get to this in a bit!

Enter the Mooninites: Crypto Lending Goes Exponential

Let’s hop in the Delorean and jump to July 2019. At this point, crypto loans had been around for nearly two years. While crypto lending had started via brokers and existing desks, the crypto community quickly realized that you didn’t need a team of expensive traders to match buyers and sellers of risk. You could use the magic of the internet to match this market, and you could use the financial primitives being built on top of Ethereum to build new types of debt instruments. The first such product was the margin loan product provided by Maker.

Borrowing using an on-chain margin loan was easy; a borrower would lock up Ether as collateral and borrow dollars in the form of the stablecoin Dai (a synthetic dollar, if you will). As long as the value of the locked Ether stayed above 150% of the USD denominated loan balance, the borrower would not be margin called. If it dropped below this threshold, the locked Ether would be liquidated to repay the loan, ensuring that the lender suffered no credit loss, and any excess would be returned to the borrower’s ether wallet. The Maker system was a massive proof of concept for the open finance ecosystem, and demonstrated how financial incentives and programmable money built on top of the Ethereum network could facilitate an automated lending market that followed programmatic rules, rather than a manually matched marked.

By providing liquidity in the form of dollar-pegged stablecoins to borrowers willing to over-collateralize with their existing “unproductive” crypto holdings, on-chain lending opened up a new frontier — the ability to obtain leverage without liquidating a scarce and appreciating asset. On the flip side, for those with assets seeking yield, lending in these markets offered variable interest rates that far outweighed the abysmal overnight rates provided by traditional banks in exchange for bearing greater risk. These risks include protocol, smart contract, liquidity, and asset price volatility risk.

There have, of course, been numerous issues with different crypto-collateralized lending platforms stemming from different flaws in design — including technical errors in smart contracts as well as behavioral edge cases stemming from unseen arbitrage opportunities. However, the Maker experiment proved this system (a) worked and (b) drastically expanded capital availability and efficiency.

Over time, Maker evolved from single collateral, in the form of Ether, to multi-collateral, and today, there is an active rate market in the crypto market for borrowers and lenders of different assets in all sorts of exotic new ways…

Which brings us up to the present! In Part Two we outline new models for alternative credit being implemented in the world of “decentralized finance” or DeFi today.