A summarizing review of what has been happening at the crypto markets of the past week. A look at trending sectors, liquidity, volatility, spreads and more. The weekly report in cooperation with market data provider Kaiko.

The last 7 days in cryptocurrency markets:

- Price Movements: All crypto sectors ended Q1 down, despite enjoying healthy gains in March.

- Volume Dynamics: Bitcoin trade volume is increasingly concentrated at the overlap between US and EU trading hours.

- Order Book Liquidity: Price slippage for BTC-USDT pairs is at all time lows.

- Derivatives: Bitcoin's put-call ratio fell to its lowest level since January.

- Macro Trends: Risk assets erased losses in March despite rising yields.

ETH ends the week up despite massive Ronin hack

Last week, the largest crypto hack ever hit the Ronin Network, an Ethereum sidechain powering the blockchain-based game Axie Infinity. It took 6 days for developers to notice the hack, which saw 173'600 ETH (about $600mn) and 25.2mn USDC siphoned from a bridge connecting the sidechain to Ethereum (ETH). Despite the news, ETH ended the week in the green, and Bitcoin (BTC) continued to trade between $45'000 and $48'000.

On the regulatory front, two European Parliament committees voted in favour of proposals that would require crypto companies to collect KYC information on unhosted wallets before approving transactions. Lawmakers stated that the proposals would bring the EU in compliance with the Financial Action Task Force’s travel rule , though they are likely to face challenges in the European Commission.

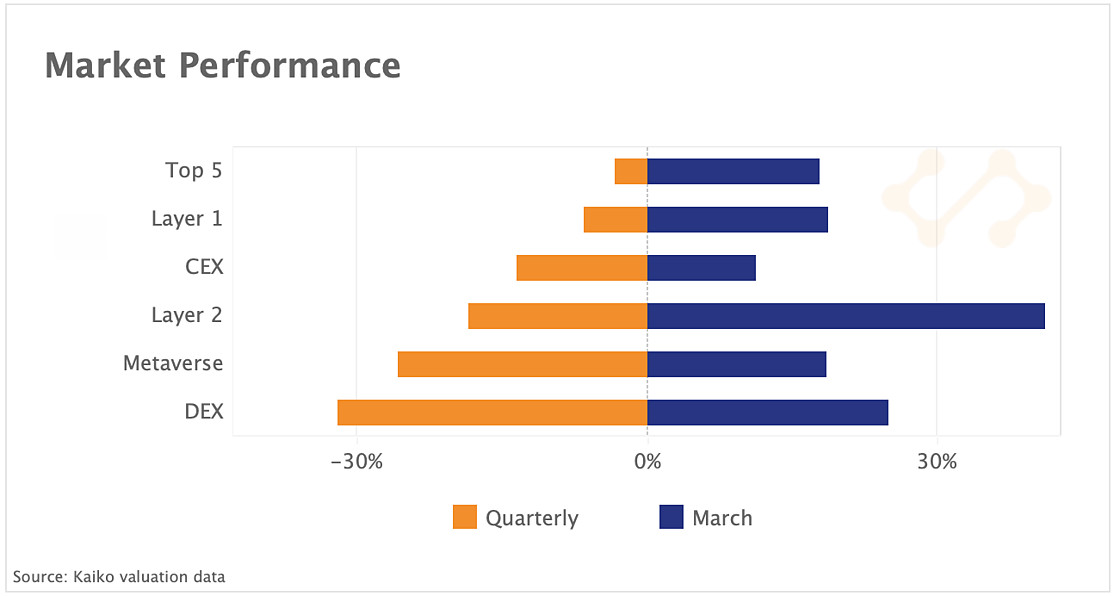

Dismal Q1 returns despite strong March recovery

Despite a strong recovery in March, all crypto sectors registered negative returns in the first quarter of the year, as macro and geopolitical headwinds took their toll on risk sentiment. We chart the returns of different market sectors in Q1 (orange) and March (blue) by compiling a portfolio of the five largest assets by market cap for each segment. We observe that the top 5 crypto assets overall were Q1's best (or least worst) performers while DEX tokens registered the worst returns, plummeting more than 30%. By contrast, in March, all market segments ended well in-the-green. Tokens affiliated with Layer 2 scaling solutions were the best performers, led by Loopring’s native LRC token and Skale network’s SKL, which jumped more than 50% over the past month.

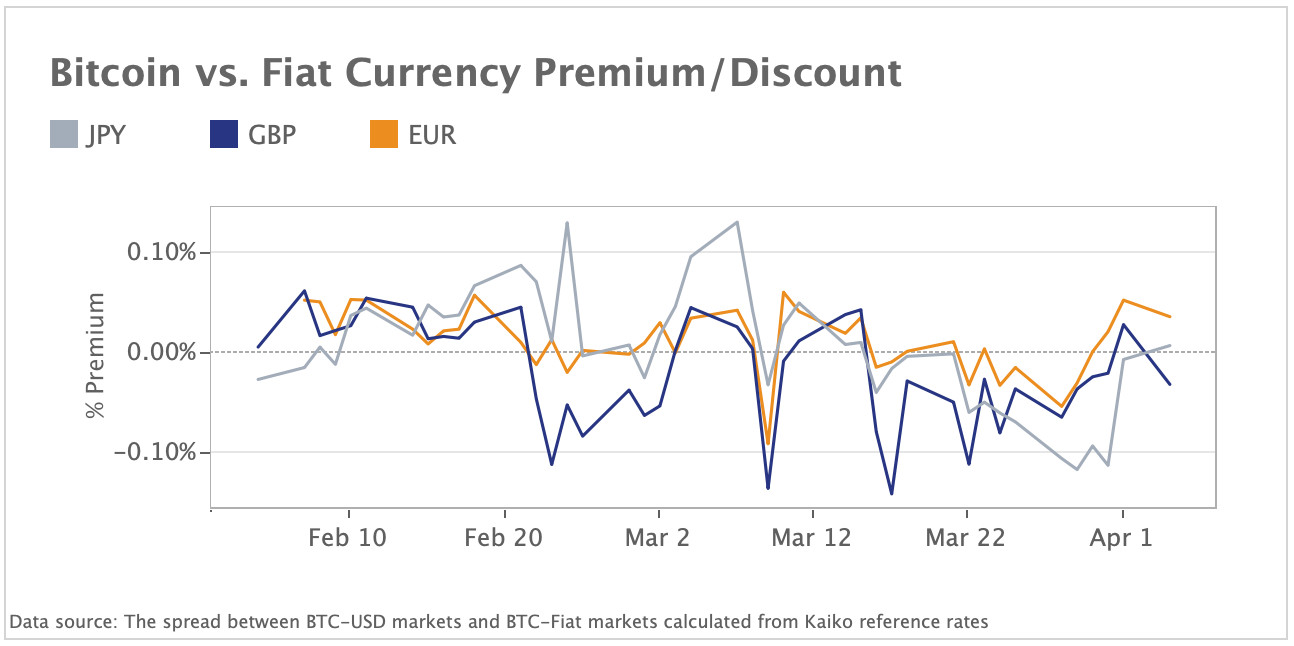

Bitcoin trades at a discount on fiat currency markets

Bitcoin traded at a discount on GBP, EUR, and JPY markets—in addition to KRW markets discussed last week— before a move back to neutral territory at the start of April. In Japan, Bitcoin traded at a discount on Japanese markets despite the Japanese yen (JPY) hitting a historic, 7-year low against the US Dollar last week. This has led to speculation within the crypto community that the outflows from the Yen could flow into Bitcoin and U.S. equities, although the discount does not reflect this sentiment.

The EUR/BTC premium was the least volatile of the group, despite regulatory concerns surrounding the EU’s Markets in Crypto-assets (MiCA) framework, which has been hotly debated in recent weeks.

Finally, the GBP/BTC premium was mostly negative through March, as the March 31st deadline for crypto firms to register with the Financial Conduct Authority loomed; the FCA on April 1 provided temporary registration for six firms, including Revolut, Copper Technologies, and CEX.io, to continue operating while the FCA assesses their applications.

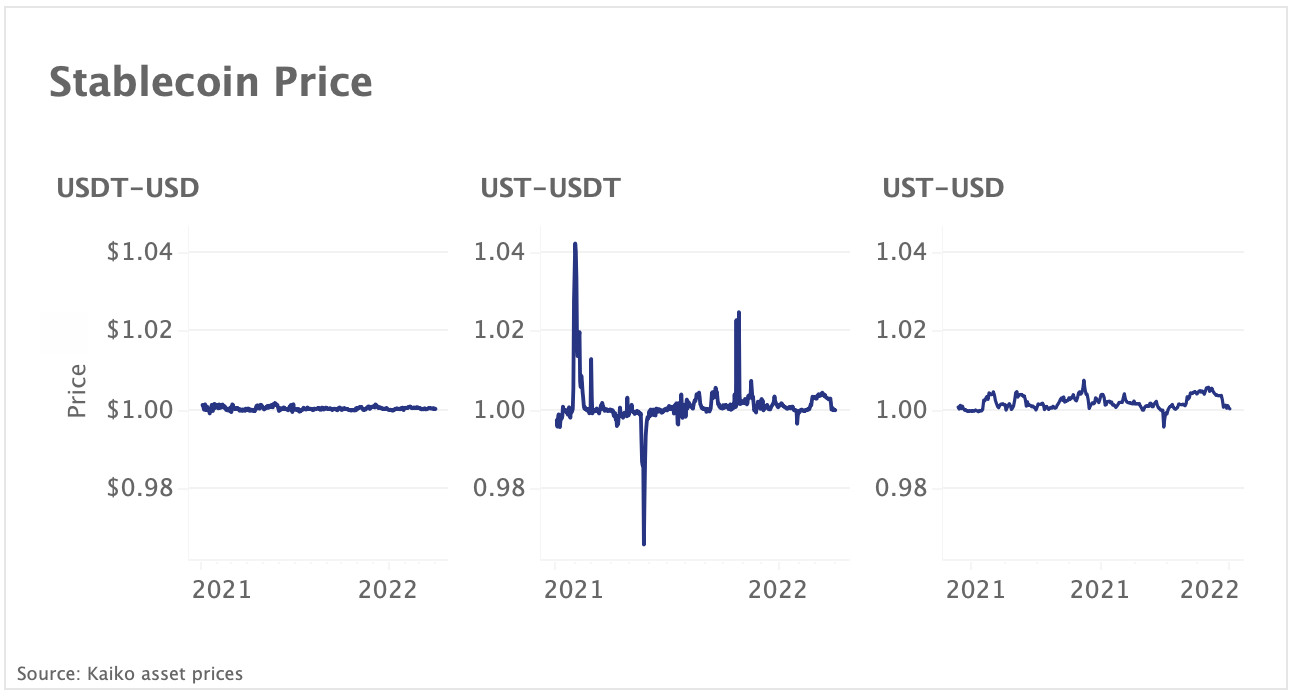

Decentralized stablecoin UST enters the spotlight

Decentralized stablecoin Terra USD (UST)—issued on the Terra blockchain— has received significant attention lately after the Luna Foundation Guard announced it would be purchasing up to $10bn of Bitcoin to create a “Forex Reserve” to minimize the risk of de-pegging. UST was first announced on September 21, 2020, and has since grown to over $16bn market capitalization, $11.9bn of which is deposited on Anchor protocol to earn over 19% APY. While the success of decentralized stablecoins like UST has been rapid, centralized stablecoins remain much larger and more liquid; USDT’s market cap is roughly five times larger than that of UST.

Smaller-cap stablecoins like UST tend to experience more frequent arbitrage opportunities when the price de-pegs from 1:1, making them popular among traders. Above, we chart the price of 3 stablecoin pairs, and can observe that UST remains more volatile than USDT, often coinciding with significant market or protocol events. For example, the large decrease in 2021 came during the May drawdown, when some speculated that UST would permanently lose its peg. Over the weekend,Terraform Labs CEO Do Kwon endorsed a proposal to create a 4pool on the decentralized exchange Curve containing UST, FRAX, USDC, and USDT with the goal of “bridging the gap between decentralized and centralized stables” and “starving the 3pool,” which contains DAI, USDC, and USDT.

On centralized exchanges, there are only 4 UST-USD trading pairs compared with 8 UST-USDT, which remains one the most popular means by which to exchange UST. This demonstrates the popularity of stablecoin-stablecoin pairs, which exhibit more volatile price profiles than direct USD pairs.

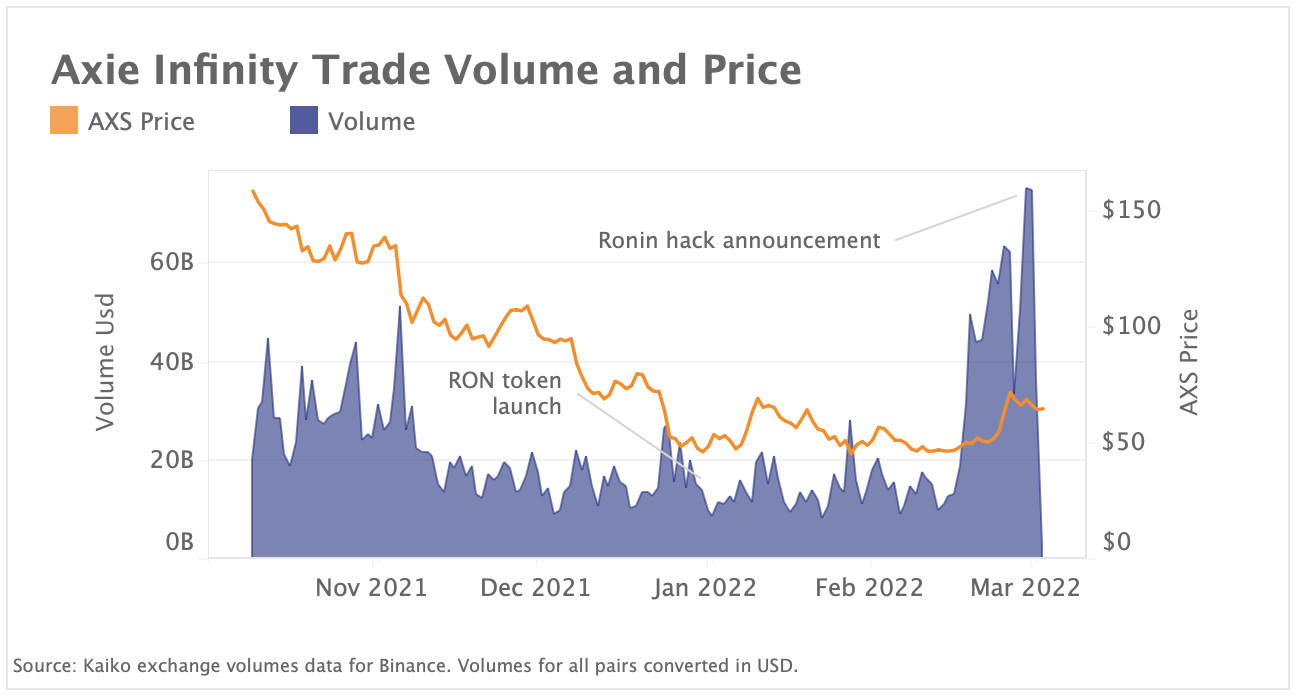

$600m Ronin hack causes AXS volume spike, with little price impact

On March 29, it was discovered that the Ronin Network, an Ethereum sidechain designed for the blockchain-based game Axie Infinity, had been compromised, with the attacker draining 173'600 Ethereum (about $600mn) and 25.5mn USDC from the Ronin bridge. Notably, while ETH and USDC deposits on Ronin were drained, the team announced that “[a]ll of the AXS, RON, and SLP on Ronin are safe.” The news of the hack generated significant volumes for Axie's token AXS but had only minor impacts on price. This may be due in part to a recent precedent set by the Wormhole bridge exploit of 120,000 ETH (about $325mn), after which Jump Crypto stepped in to replenish the stolen funds. Sky Mavis, the creator of Ronin and Axie, is backed by several large investors, including Andreessen Horowitz, FTX, and Paradigm.

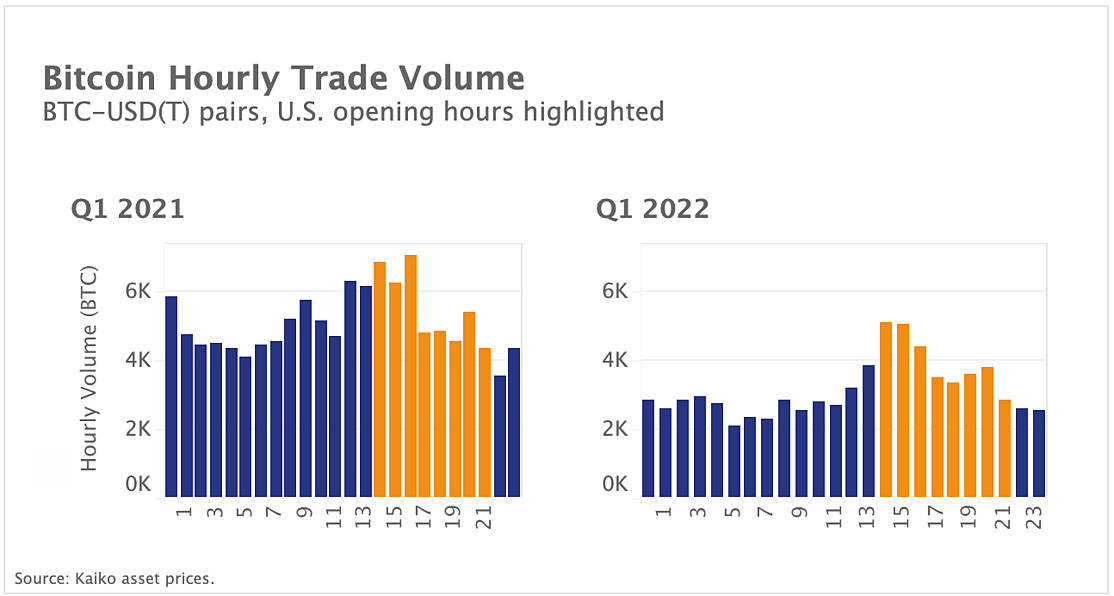

Bitcoin increasingly trades during US trading hours

Bitcoin’s trading activity is increasingly concentrated during U.S. trading hours, which is in line with the asset’s rising correlation with U.S. equities. We chart hourly average BTC-USD(T) trade volumes (aggregated across all exchanges) in Q1 2021 and 2022, and can observe that the variance in average hourly volume in 2021 was slightly lower than in 2022. Volume appears to be increasingly concentrated at the overlap between US and EU hours: volume between 8-10am EST is nearly double all other hours. We can also observe that average hourly volumes are around 50% lower compared to last year following a drop in risk appetite.

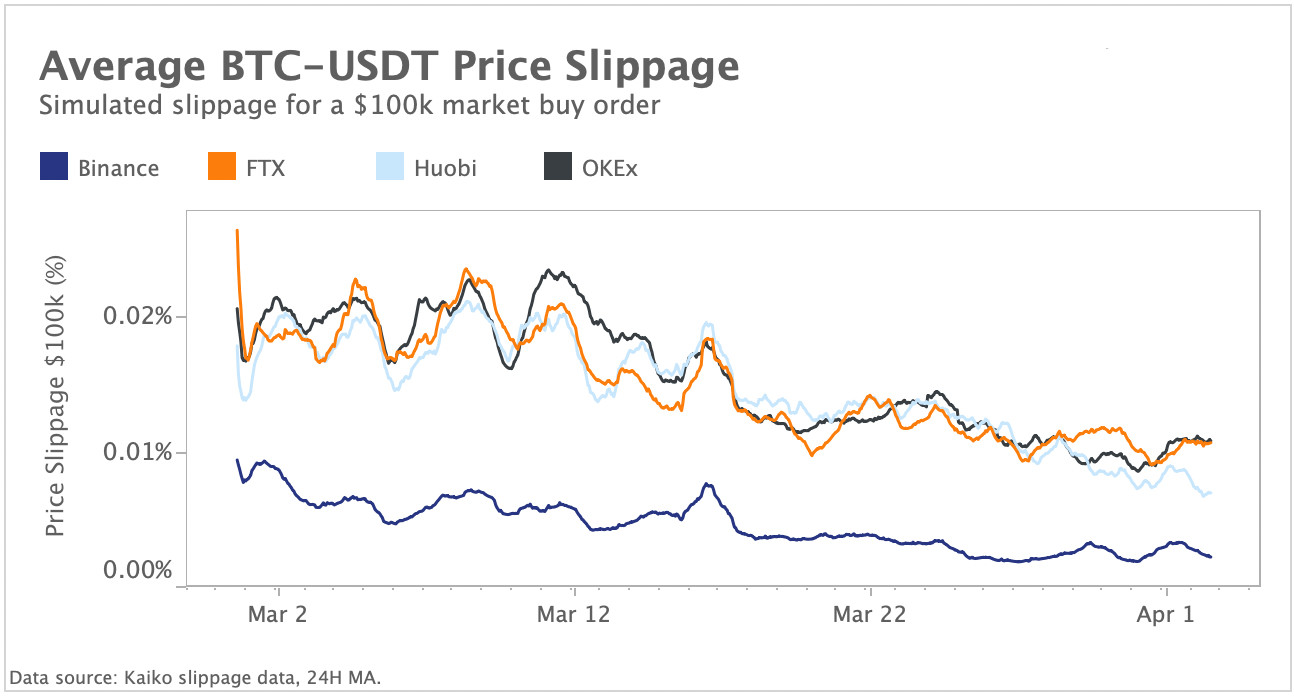

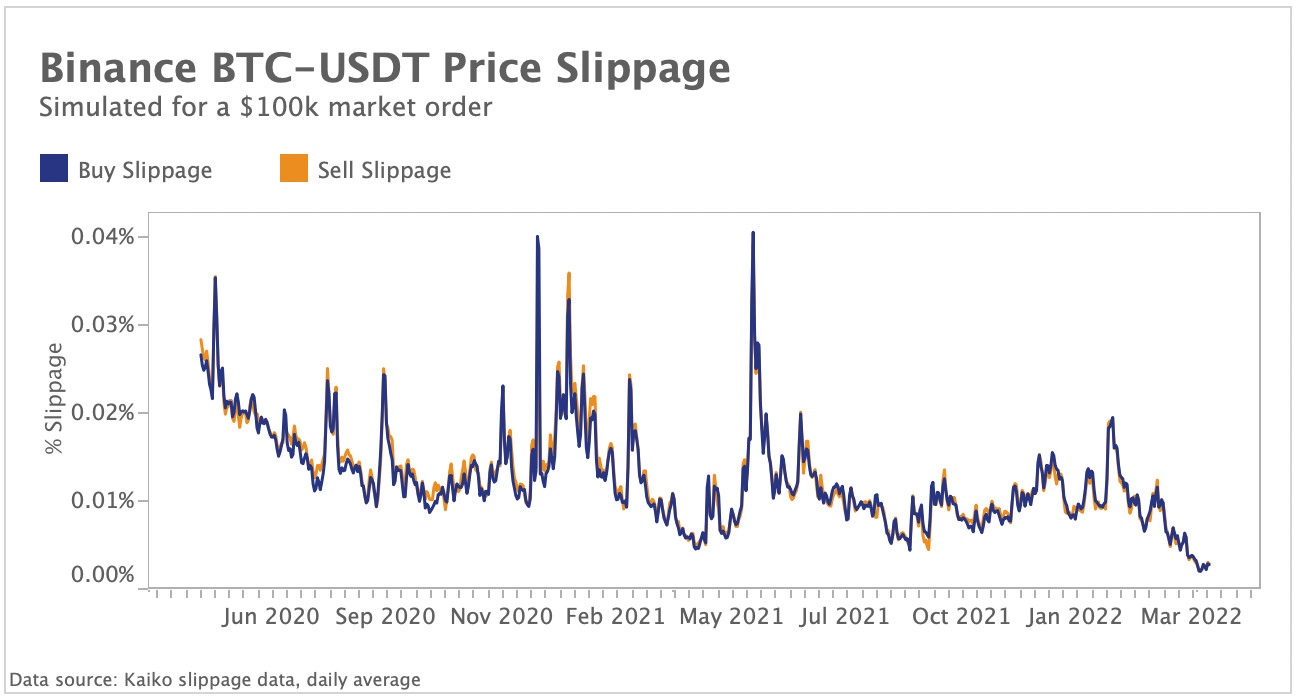

Bitcoin-Tether price slippage at all time lows

Price slippage for the most liquid BTC-USDT trading pairs has fallen to all time lows on the biggest global cryptocurrency exchanges. The same trend was not observed for the most liquid BTC-USD pairs. Price slippage is an indicator for liquidity and is calculated by taking the difference between the expected price of a trade and the price at which the trade is fully executed (in this case, a simulated $100k buy order). On all 4 exchanges, average slippage has fallen sharply throughout March, but Binance has experienced the best improvement in liquidity over time.

Since May 1st 2020, price slippage on Binance has fallen from an average of 0.02% for a $100k buy or sell order to ~0.002%, which shows how on both sides of the order book liquidity has strongly improved. Slippage is an important measure that large traders pay attention to in order to avoid moving the price of an asset. With news that the Luna Foundation is executing $125m in Bitcoin buy orders every day, it is highly likely that Tether trading pairs are playing a role in these transactions.

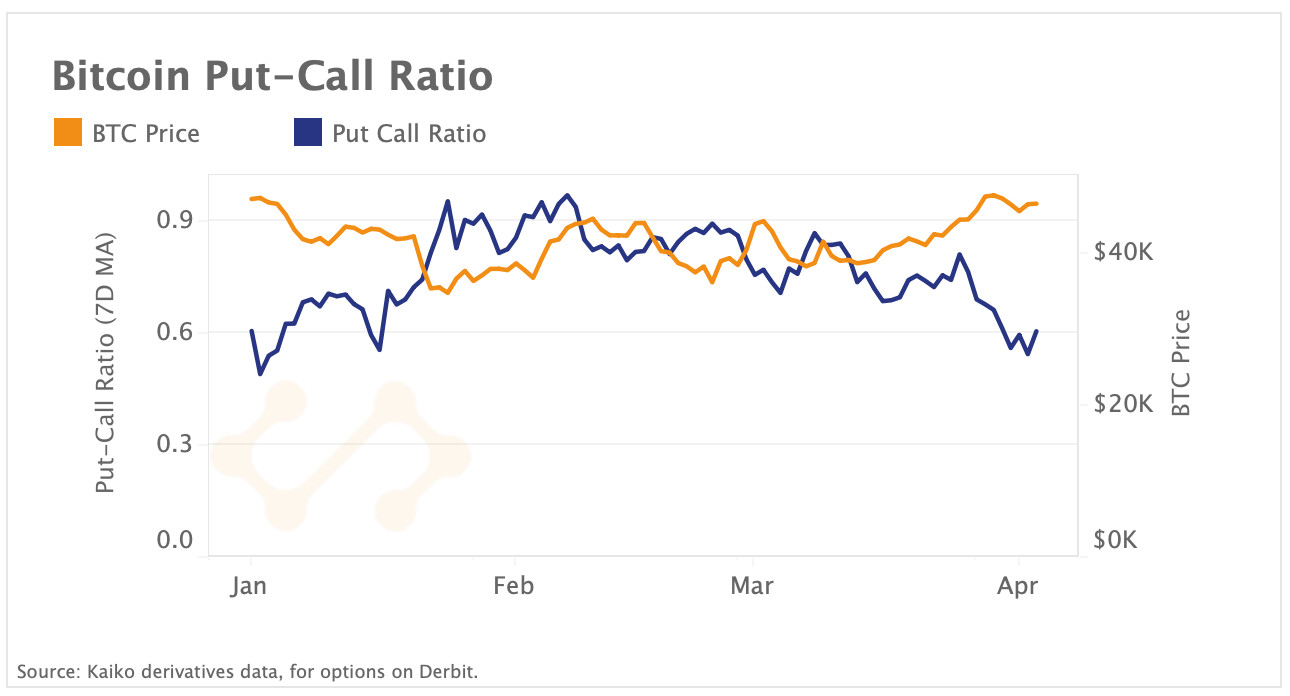

Put-call ratio hits lowest level since January

The ratio of Bitcoin put to call option trade volumes on the largest options exchange Deribit fell to its lowest level since early January last week. Typically, a decreasing put-call ratio is seen as a bullish sign as demand for puts (bearish bets) are declining relative to calls (bullish bets). The ratio has been on a downward trend after hitting a yearly high of .96 in February. Together with falling short-term volatility this suggests an easing of bearish sentiment on option markets.

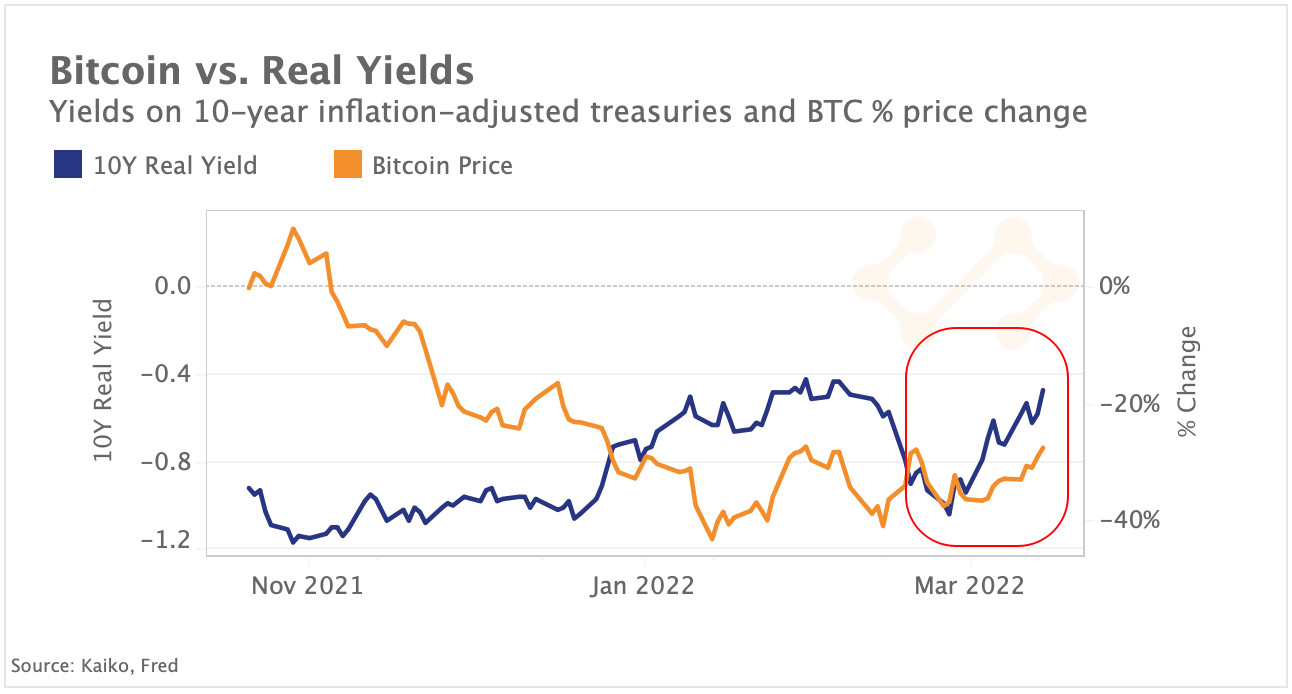

Risk assets surge in March despite rising real yields

Risk assets rallied in March despite growing recession fears and the kick off of tightening by the Fed. Above, we chart the real 10-year treasury yield - or the returns investors can expect after inflation is taken into account - along with Bitcoin price returns. Typically, rising borrowing costs hurt risk assets such as tech stocks and crypto, which appear less attractive to investors than safe-haven bonds. While remaining in negative territory, real yields have increased by over 40 bps in March as the U.S. Fed kicked off monetary policy tightening. However, both Bitcoin and the tech-focused Nasdaq 100 ended last month up 6%, erasing their losses from the sell-off sparked by Russia’s invasion of Ukraine.