A summarizing review of what has been happening at the crypto markets of the past week. A look at trending sectors, liquidity, volatility, spreads and more. The weekly report in cooperation with market data provider Kaiko.

The last 7 days in cryptocurrency markets:

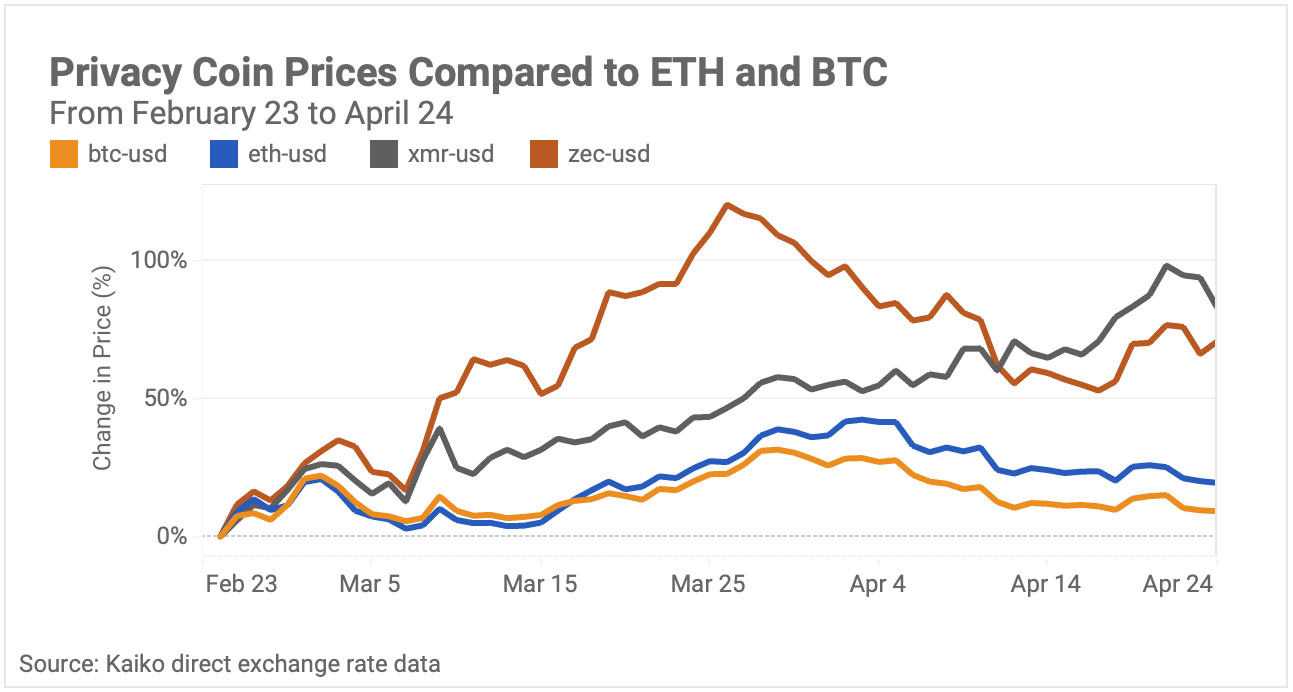

- Price Movements: Privacy tokens have outperformed ETH and BTC since late February.

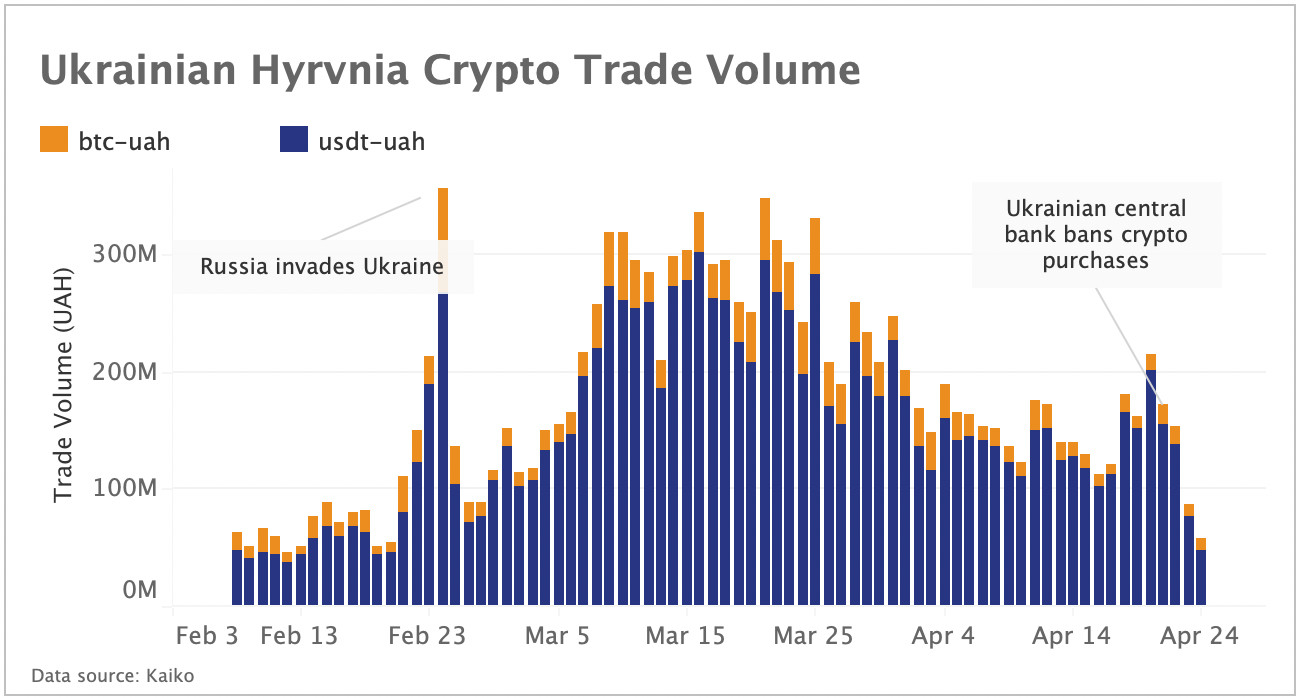

- Trade Volume: Ukrainian crypto trade volume dropped to pre-invasion levels after the central bank banned crypto purchases.

- Order Book Liquidity: Despite the lowest number of ETH on exchanges since 2018, market depth has remained steady.

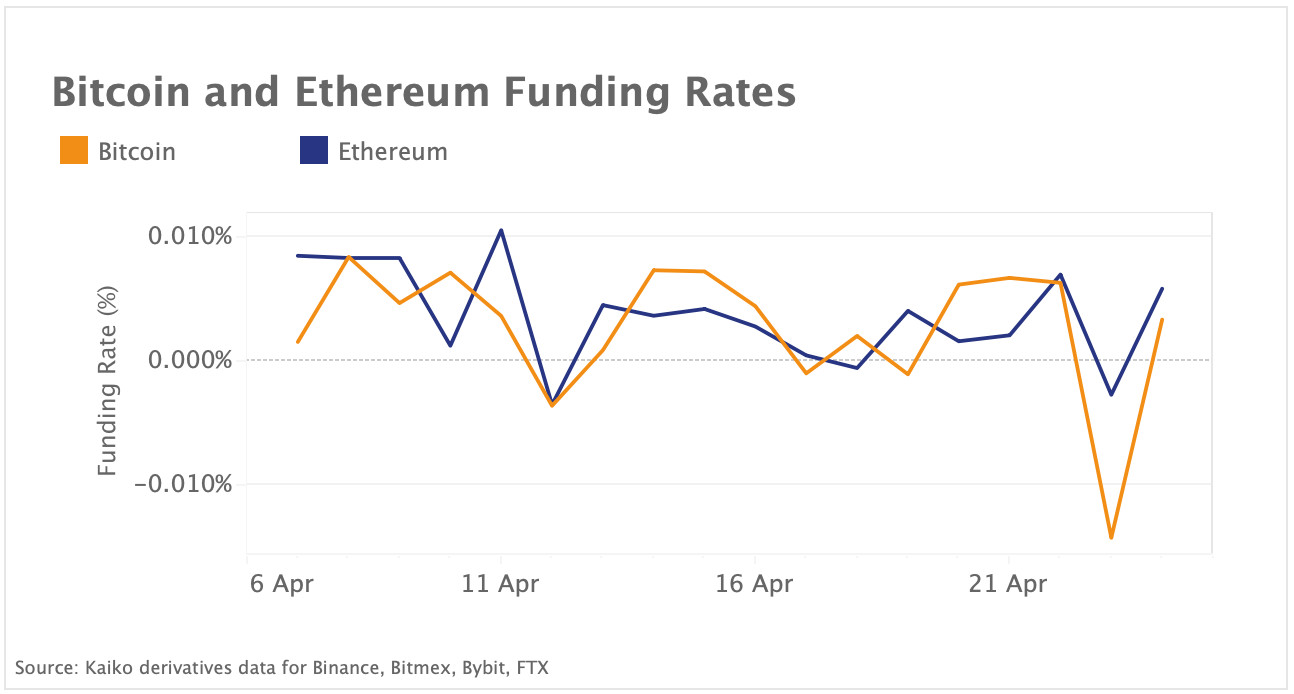

- Derivatives: Funding rates dipped negative during bearish pullback.

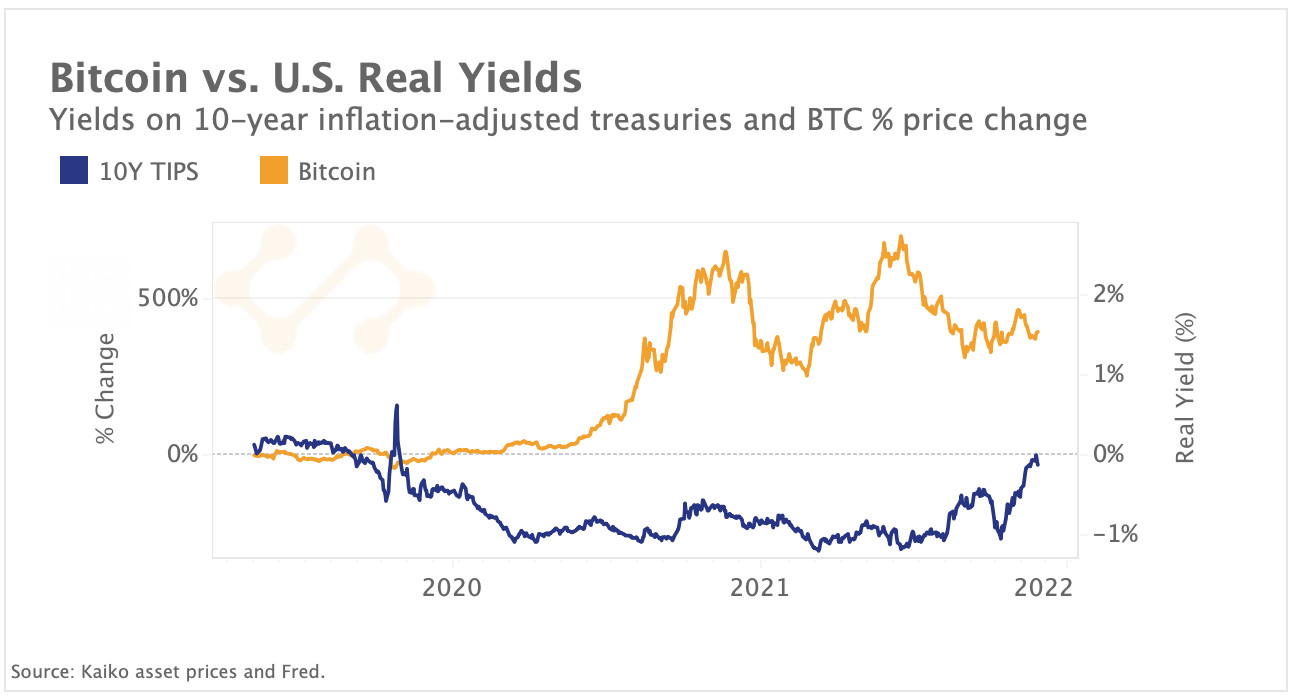

- Macro Trends: Real yields turned positive for the first time since March 2020.

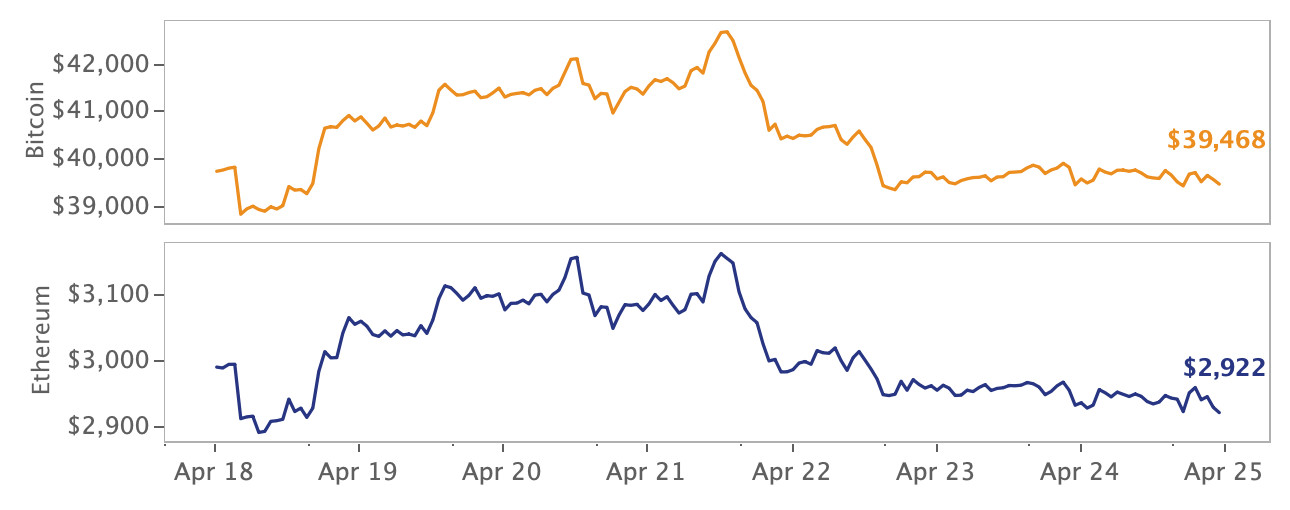

Crypto trends down as equities experience sell-off

Bitcoin (BTC) and Ethereum (ETH) finished last week in the red while equities suffered their biggest single day drop since 2020 following hawkish comments by U.S. Federal Reserve Chair Jerome Powell. Last week, the stablecoin wars heated up after Justin Sun, founder of TRON, announced the creation of an algorithmic stablecoin for the network called Decentralized USD (USDD), which mimics Terra’s UST mechanism and will offer a 30% interest rate designed to rival Anchor's 19.5%. NEAR Protocol is also expected to launch an algorithmic stablecoin with a 20% interest rate, highlighting the increasing popularity of using decentralized stablecoins to drive network usage. Finally, Coinbase released a beta version of its NFT marketplace, which emphasizes social features and will allow users to make purchases using a credit card.

Privacy coins outperform since February

The top two privacy coins by market cap – Monero and Zcash – have rebounded faster than Bitcoin and Ethereum following Russia’s invasion of Ukraine in late February. Russia has faced severe sanctions as a result of the invasion, with many specifically targeting crypto. Most recently, the U.S. Treasury sanctioned Bitriver, a Russia-based Bitcoin miner; earlier this month, the U.S. and Germany took down Hydra, a notorious black market exchange.

Russian citizens have increasingly been cut off from traditional financial services, and major exchanges like Binance have taken actions to limit their access. This has created a perfect storm of narratives to boost privacy coins, though it is unclear whether they are actually being used to evade sanctions. Monero and Zcash are still 50% and 95% down from their all time highs, respectively.

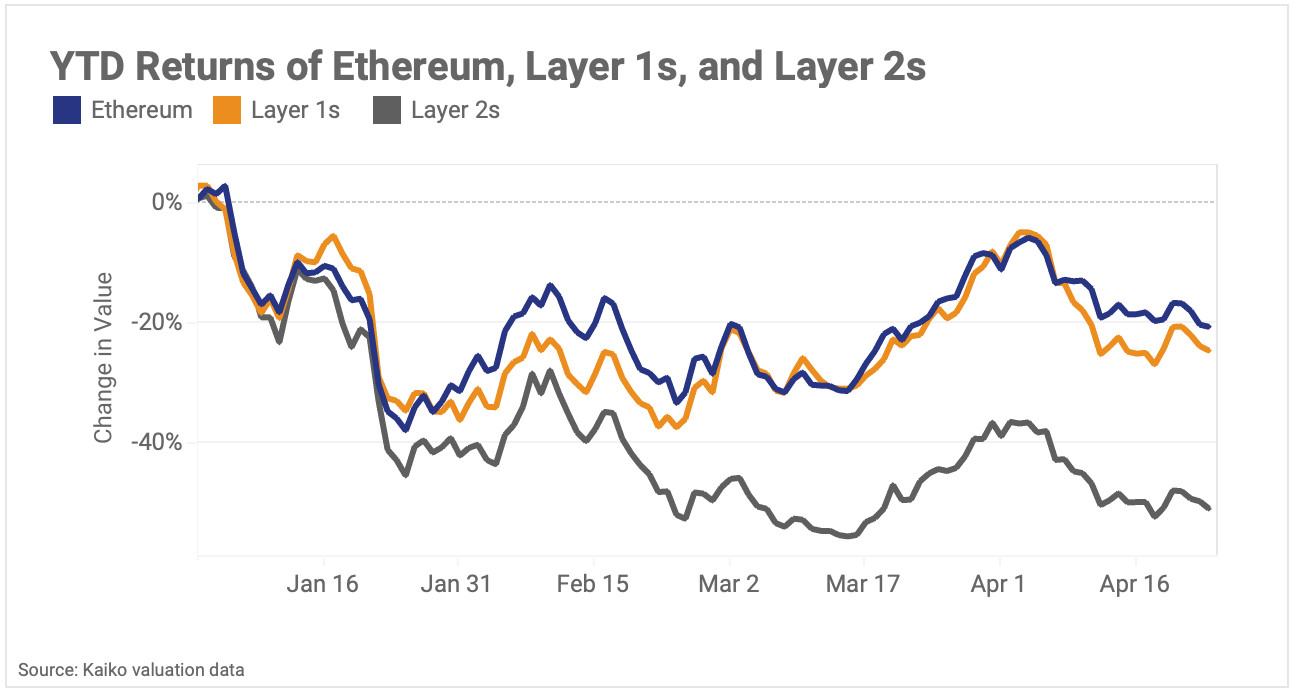

Layer 2 tokens struggle, while Layer 1s keep pace with ETH

Layer 2 tokens have struggled since the start of 2022, underperforming both Ethereum and Layer 1s. We built simulated baskets of top Layer 1 tokens (SOL, LUNA, ADA, AVAX, and BNB) and Layer 2 tokens (DYDX, LRC, METIS, BOBA, and MATIC) since the beginning of the year. Layer 2 tokens have struggled and are down over 40% after a particularly difficult February and March. With hints from the team that Optimism (4th largest L2 by TVL) will be releasing a token, it is possible that there will be a resurgence of interest in L2s. There have also been cryptic messages from the Arbitrum (2nd largest L2 by TVL) team that it will be releasing a token.

Major Layer 1 tokens have moved in line with ETH over the year, though Ethereum has continued to lose total value locked market share. NEAR Protocol, the 7th largest Layer 1 by market cap, has outperformed the others and is about even with where it began the year.

Ukrainian crypto trade volume drops to lowest level since pre-invasion following central bank ban

Last Thursday, the Ukrainian central bank banned the purchase of crypto using local currency to "prevent unproductive outflow of capital from the country." The effect on Hyrvnia-denominated trade volume was nearly instantaneous. BTC and USDT trade volume on Binance dropped to their lowest levels since before Russia's invasion, falling from the equivalent of ~$5 million daily to about $2 million as of this weekend. Despite the ban, Ukraine has embraced crypto throughout the war, formerly legalizing its use last month and receiving more than $50 million in BTC and ETH donations.

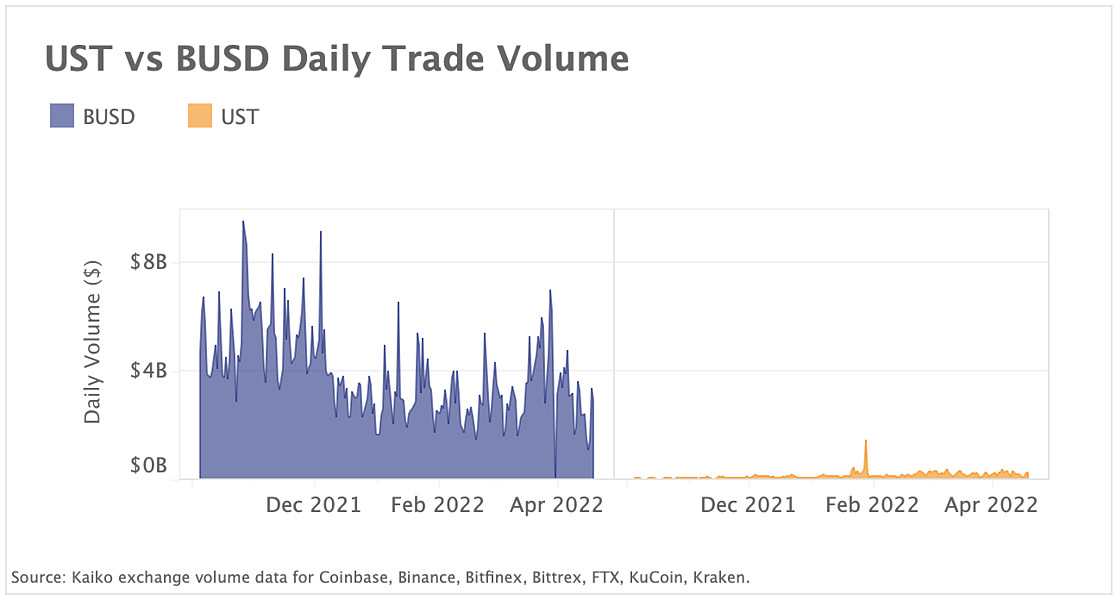

US Terra trade volume reveals niche use of the decentralized stablecoin

Last week, US Terra became the third largest stablecoin by market cap at around $18bn, flipping Binance’s BUSD (for reference, the largest stablecoins USDT and USDC have market caps of $83bn and $50bn, respectively). Despite its higher market cap, UST’s daily trade volume on centralized exchanges is significantly lower than BUSD’s, which is around $4bn daily compared with ~$140m.

This difference speaks to the different intentions and designs of the growing stablecoin space: BUSD was created by the world’s largest exchange, Binance, which has promoted the stablecoin by offering lower trading fees when users transact with it. UST was designed to serve as a decentralized, DeFi-native stablecoin on the Terra protocol.

Yet, when taking a closer look at the breakdown in UST usage, nearly 67% of supply is deposited in the lending and borrowing protocol Anchor, where users can earn more than 19% APY. Questions have been swirling over the sustainability of this model, which requires capital infusions to maintain the high yields. While UST may now be the 3rd largest stablecoin, its recent growth has been mostly driven by high yields offered by Anchor.

BTC and ETH funding rates dip negative

Bitcoin and Ethereum funding rates re-set to neutral over the weekend after turning negative last week on renewed monetary policy tightening jitters and worries around China’s growth outlook. We chart the average BTC and ETH funding rates on four exchanges - Binance, Bitmex, Bybit and FTX. Funding rates are seen as a gauge of market sentiment with positive funding rates suggesting that more traders are entering long positions and bullish demand is strong (and vice versa). Despite recovering over the past few days, Bitcoin perpetual futures funding rates fell more than Ethereum’s last week touching a monthly low. Overall funding rates for both assets have been on a steady downward trend since December.

Real yields are positive for first time since March 2020

The 10-year Treasury Inflation Protected Securities (TIPS) yield is seen as the real, inflation-adjusted risk free alternative to owning risky assets. When real yields are rising the opportunity cost of holding riskier assets increases, making riskier investment tougher to justify. The real yield has now turned positive for the first time since 2020, meaning the environment for risky assets has become the least attractive for a couple of years.

However, if we are to use the four-decade high CPI reading of 8.5% as our adjustment for real yields, rather than the TIPS yield, the real yield still stands significantly negative at -5.5%. The case could be made that this suggests there is still plenty of real-world incentive to invest in risky assets, or that this simply means the Fed still has more room to raise rates. Real yields look to only be rising in the near term however, as the Fed seems to have prioritized curbing inflation over accommodating growth.