price lagging behind Bitcoin (BTC)?")

Ethereum has long stood as a beacon of innovation, second only to Bitcoin. With a valuation of $282 billion, Ethereum has earned its stripes as "a world computer," "ultrasound money," and the "cornerstone of decentralized finance (DeFi)". Yet despite all these achievements, why is ETH lagging behind BTC?

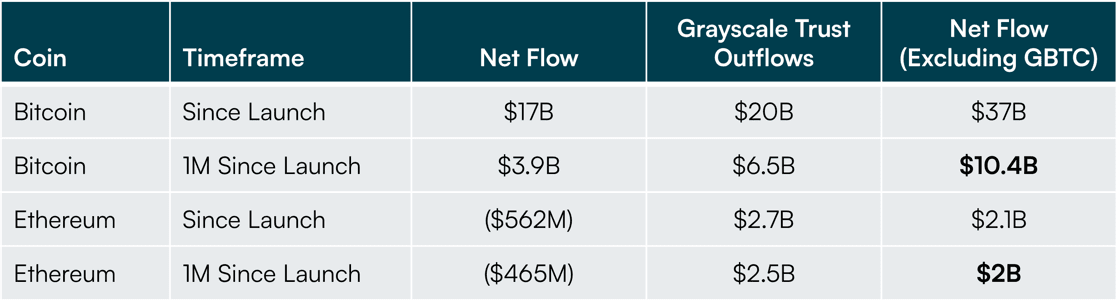

The answer, at first glance, seems deceptively simple. Bitcoin's meteoric rise can be largely attributed to the watershed moment of spot Bitcoin ETF approvals in the United States. This development has opened the floodgates for institutional capital, propelling Bitcoin to new heights while leaving altcoins, including Ethereum, in its wake. Lets take a look at ETF flows thus far.

Market dynamics

Interestingly, Ethereum's share of global ETP Assets Under Management (AUM) stands at a respectable 15.4% compared to Bitcoin. This figure aligns closely with Ethereum ETF inflows relative to Bitcoin ETF inflows (ex-Grayscale) over the first month, which sits at 19%. These statistics suggest that Ethereum maintains its proportional appeal among institutional investors, despite its apparent underperformance in the broader market.

While ETH has underperformed (YTD +4%) relative to BTC's impressive 35% year-to-date increase, it's important to note that not all altcoins have shared this fate. Several cryptocurrencies within the top 70 by market cap have outshone even Bitcoin's stellar performance:

- BNB: 66% (31% above BTC)

- TON: 124% (89% above BTC)

- FET: 87% (52% above BTC)

- PEPE: 478% (443% above BTC)

- WIF: 1018% (983% above BTC)

This divergence in performance highlights the current market's preference for emerging L1 blockchains (like TON), AI projects (FET), and memecoins (PEPE and WIF). It also underscores the current narrative and interests of users.

The Layer 2 roadmap: A double-edged sword

Coming back to Ethereum, its journey towards scalability has led to the rise of Layer 2 (L2) networks such as Arbitrum, Optimism, Base, Blast, and zkSync. This shift has dramatically reduced gas fees for users and improved transaction speeds, addressing long-standing criticisms of the Ethereum network. However, this solution has introduced new complexities to Ethereum's value proposition.

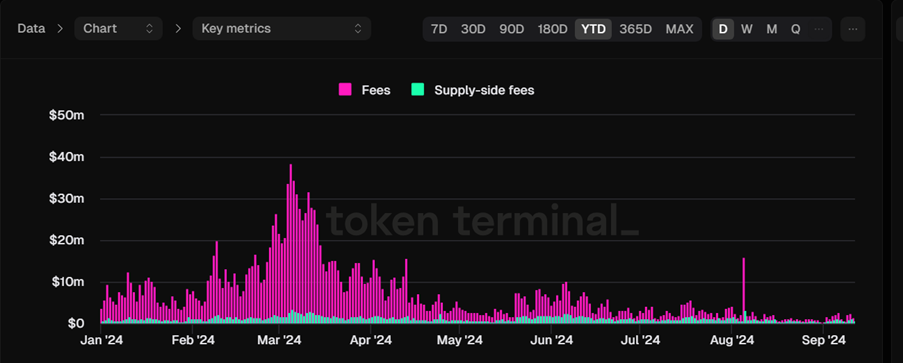

The numbers tell a compelling story. The top 12 L2 solutions now process a staggering five times more daily active addresses and transactions than Ethereum's mainnet. This migration of activity off the base layer has had profound implications for Ethereum's economic model. The recent Cancun/Deneb upgrade, implemented on March 13, 2024, has further amplified this effect. By reducing fees for rollup operators by a factor of 1000, the upgrade has significantly diminished Ethereum's fee-derived protocol revenue in the short term.

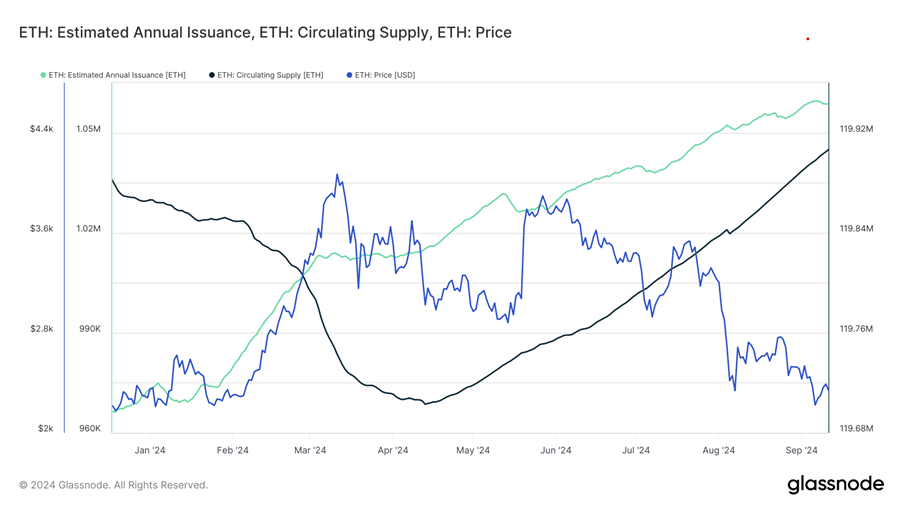

While this move enhances Ethereum's scalability, it has also contributed to ETH's underperformance, especially as L2 solutions become increasingly interoperable with other high-performance, low-cost settlement and data availability chains like Celestia. Reduced fees for Ethereum have also led to supply-side factors affecting ETH’s performance. After the Cancun upgrade in March, fees on Ethereum reached an all-time low. This has resulted in a net issuance in ETH supply, and the total circulating supply is now net positive. The increase in supply is an evident factor in ETH's dismal performance as well.

The Shifting Sands of DeFi and NFTs

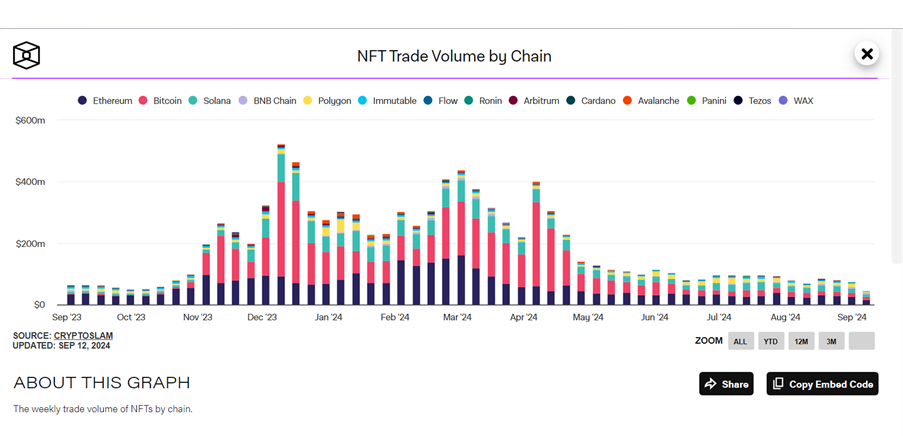

The DeFi landscape has shifted significantly, with investor focus moving towards emerging narratives like ETFs, memecoins, and artificial intelligence projects. This change has potentially slowed the influx of fresh capital into ETH. While Ethereum still hosts more than half of all DeFi investments, the challenge lies not in the absolute value locked in these protocols, but in the waning engagement levels and the diversion of attention to newer opportunities in other ecosystems. Even NFT markets, another significant driver of Ethereum activity, have seen a sharp decline in activity and volume.

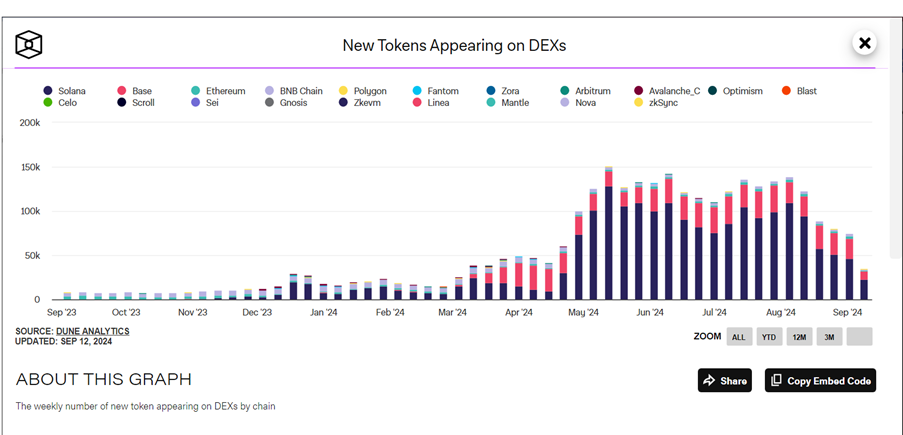

The landscape of token launches has also evolved; while most new tokens were launched on BNB and Ethereum a year ago, the trend has now shifted towards platforms like Solana and Base. Consequently, the demand for ETH as a trading pair for these new tokens has diminished, further impacting its utility and potentially its value proposition.

Utility and demand

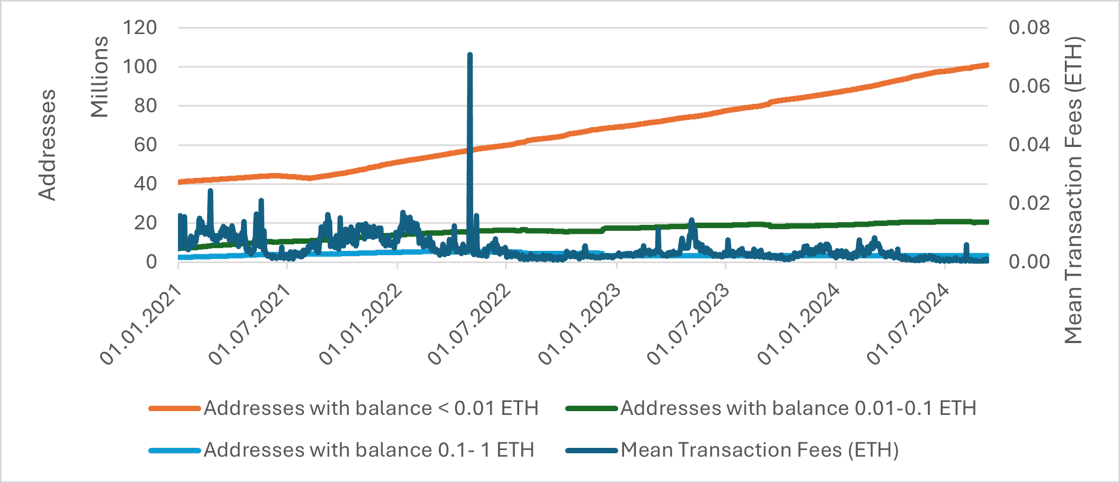

The reduced gas fees resulting from L2 adoption have decreased the need for users to hold large amounts of ETH for transaction purposes. This change in user behavior may have contributed to a reduction in buying pressure on ETH. An analysis of address cohorts and mean transaction fees supports this theory, showing a decrease in both the average transaction fee on Ethereum and the patterns of ETH holders. There is a significant increase in accounts holding less than 0.01 ETH and a flat line in accounts holding 0.1-1 ETH, which earlier could be accounted for tokens meant for gas usage.

However, the demand for staking and restaking continues to grow. With more than 50 billion USD worth of ETH staked in staking contract and 10 billion in restaking protocols, the demand to earn yield on Ethereum stays. Lido, one of the biggest liquid staking providers on Ethereum consistently posts highest revenues among defi projects. But does demand for staking equate to price appreciation? It does in the sense of increased demand to earn yields, but it has a more gradual and slow effect on price rather than a sudden one, which is also evident from the graph below.

The long game: Ethereum's evolving value proposition

As we look beyond immediate market movements, Ethereum's value proposition continues to evolve. The blockchain modularity thesis posits that Layer 2 rollup service providers, rather than end-users, will become the primary drivers of network fees for Layer 1 blockchains like Ethereum. This shift, coupled with the growing adoption of account abstraction on L2s, suggests that rollup operators may become the primary holders of ETH for block space payments. While this change may impact ETH's traditional utility, it opens up new avenues for value accrual within the Ethereum ecosystem.

Moreover, the emergence of liquid staking solutions and the maturation of re-staking protocols present new opportunities for ETH holders. These developments could lead to a scenario where end-users and DeFi protocols primarily hold token representations of staked ETH and its accumulating yield, rather than the native ETH token itself.

Conclusion

The numbers don't lie, and the common perception that Layer 2 solutions have driven value away from Ethereum is playing out before our eyes. Transaction activity on L2s has surpassed Ethereum's mainnet, and reduced fees on L2s have diminished Ethereum's revenue streams. This shift has undeniably impacted ETH's performance relative to other cryptocurrencies, particularly Bitcoin.

Yet, Ethereum continues to capture its share of institutional interest, evidenced by its proportional representation in global ETPs and ETF inflows. Ethereum's established network effects and robust developer ecosystem remain significant advantages. While L2s have currently dimmed Ethereum's spotlight, the network's fundamental strengths and its pivotal role in the broader blockchain ecosystem position it for future growth.